The Summer Slide Part 3: The Tax Code We Already Had

Why the Simulation Derived the New Deal — And What That Means

Last week, in Part 2, we diagnosed the disease. Today we test the cure. This piece continues to refer back to the code provided in this post. As many paying readers have requested, I’m placing the paywall at the bottom of the entire piece. It’s a quirk of Substack that excluding the paywall limits distribution. I thank all of my paying readers for subsidizing these notes. Your generosity is appreciated. I promise to send out a separate note later today that is entirely market focused. But markets will wait; this will not.

Let’s recap where we are.

In Part 1, we showed that in a world of geometric growth and volatility, talent doesn’t win — buffers do. The Gifted Poor went extinct at 25x the rate of the Normie Rich. The Ferrari broke an axle on the dirt road.

In Part 2, we added the costs of actual life — eating, children, and retirement — and watched the model reproduce the American economy with eerie precision. The average wealth skyrocketed while the median flatlined. The bottom 80% were pinned to the subsistence floor. The top quintile retirees became Capital itself — compounding, extracting, and never resetting. We called it the Gerontocracy, and it wasn’t a metaphor. It was the physics.

We ended with a question: Can you tax your way out of this?

You might expect the answer to be simple. Tax the rich. Redistribute. Done. It wasn’t simple at all. In fact, the first two “obvious” reforms made things worse. But the third — the one that most policy experts would dismiss as politically impossible — produced something I did not expect.

The simulation independently derived the tax code of the 1950s.

The Three Prescriptions

We tested three distinct tax philosophies against our baseline model (the untaxed Gerontocracy from Part 2). Same economy. Same agents. Same unemployment shocks. Same random seed. The only thing that changed was the tax structure.

Prescription 1: The “Orthodox” Reform

This is the tax code that both libertarians and mainstream economists call “optimal.” The logic: capital is sacred. Don’t tax it. Instead, shift the burden to consumption. Cut labor taxes (from 10% to 5%), eliminate capital gains taxes entirely, eliminate estate taxes, and introduce a 15% consumption tax. The idea is that by making capital “free,” you accelerate growth, and the rising tide lifts all boats.

Prescription 2: The “Naive Progressive” Reform

This is the populist left’s instinct. Tax capital gains aggressively — 30% annually on all gains — and redistribute the proceeds as a universal dividend. No estate tax. The logic: take from the rich every year and give to the poor.

Prescription 3: The “Deferred” Reform

Let capital compound freely during life. Zero annual capital gains tax. But at the point of intergenerational transfer — death — impose a 50% estate tax. Redistribute the proceeds as a universal dividend. This is, in essence, the structural logic of the New Deal tax code.

Let’s see what happens.

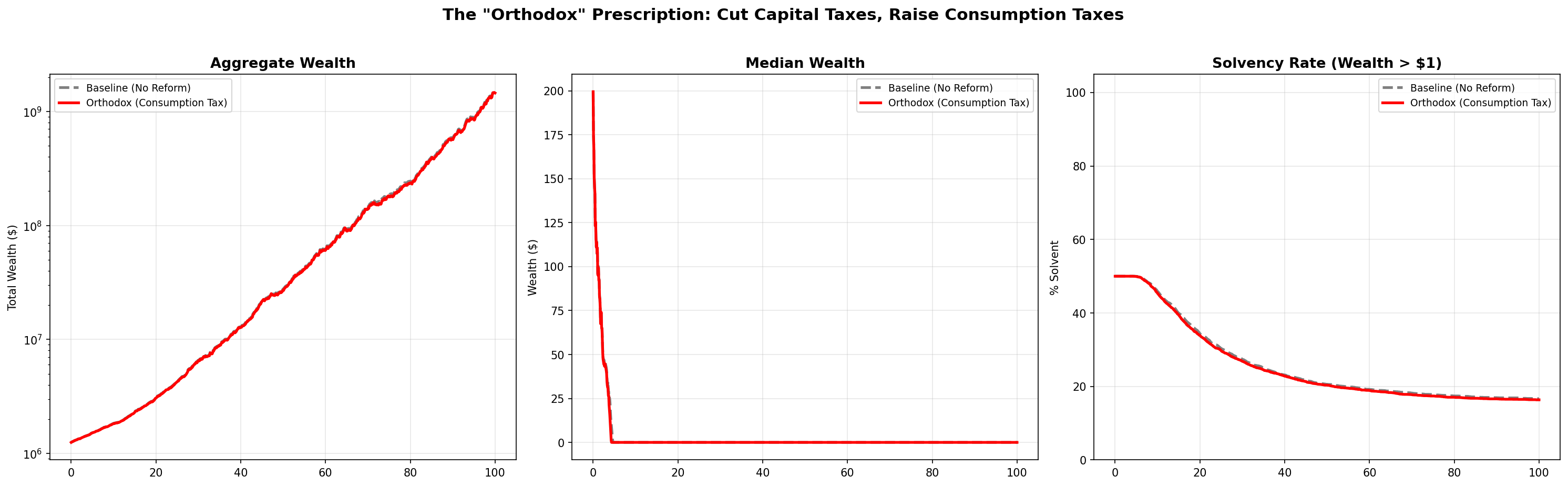

Prescription 1: The Orthodox Failure

The consumption tax is the darling of think tanks. It is “efficient.” It is “neutral.” It does not “distort” capital allocation.

It is also a torpedo aimed at the hull of every low-SES (low socioeconomic status, i.e. “poor”) household in the economy.

Here’s why. A consumption tax is functionally a tax on survival. In our model, every agent must “eat” — $50/year in non-negotiable cost-of-living. A 15% consumption tax raises that floor from $50 to $57.50. That’s $7.50 per year taken directly from the ability to form a buffer.

For the High SES agent sitting on $500 in savings, this is a rounding error. For the Low SES agent entering the workforce with $0 and trying to save $5/year (the gap between their $55 salary and their $50 cost of living), it is catastrophic. Their already razor-thin surplus — the only dollar that could compound — gets taxed before it can be saved.

The consumption tax doesn’t tax consumption. It taxes the attempt to build a buffer.

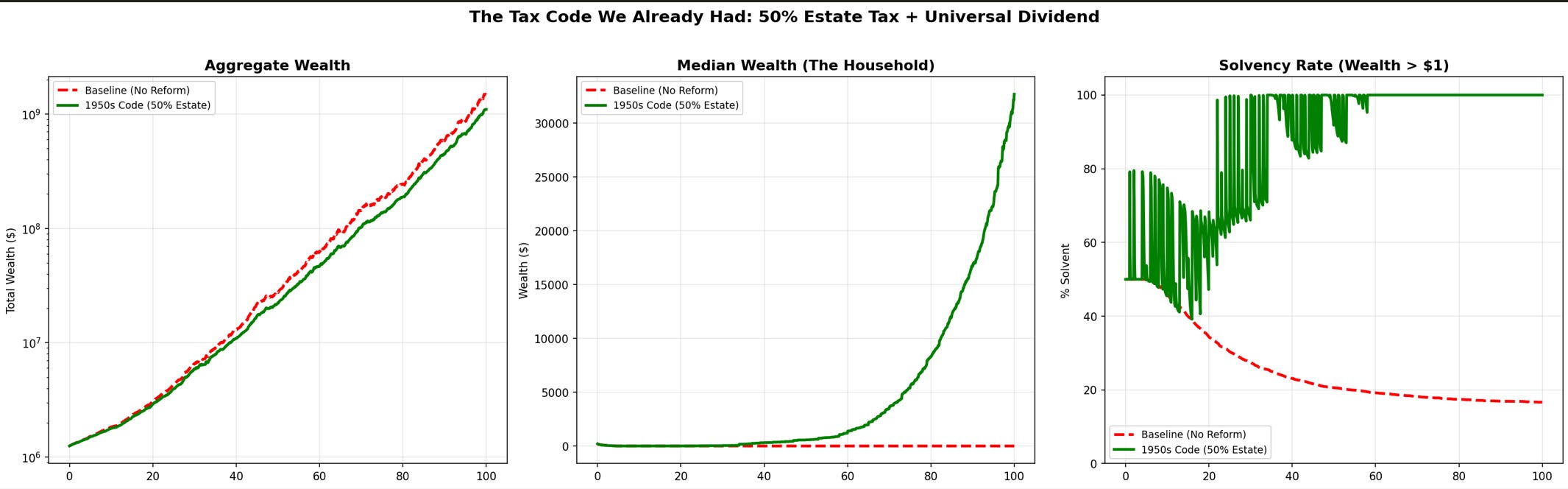

The results confirm the mechanism:

Read that again. The “optimal” reform made every metric worse. Aggregate wealth fell slightly (less capital formation from buffer-depleted agents). The median didn’t move — it was already zero. And the solvency rate — the percentage of the population with more than a dollar to their name — declined.

The “rising tide” argument requires that you already have a boat.

I want to be precise about the mechanism, because it maps perfectly to the empirical data. The consumption tax is regressive, not because of some abstract distributional concern, but because of the physics of geometric growth. A dollar taxed from the consumption floor of a low-SES agent destroys more future wealth than a dollar taxed from the surplus of a high-SES agent — because the low-SES agent’s dollar was the marginal dollar that determined whether they could compound at all.

This is not a political argument. It is a mathematical one.

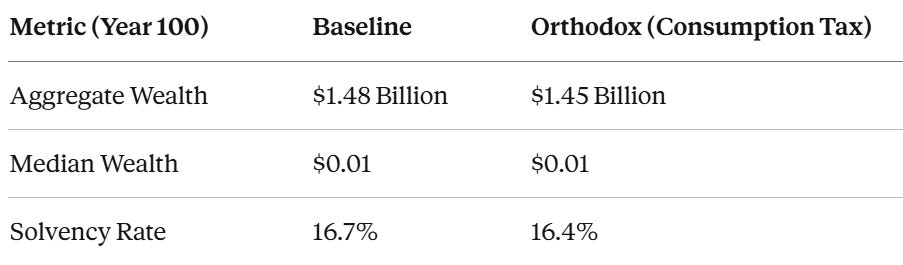

Prescription 2: The Naive Progressive Disaster

If the right’s instinct (free capital, tax consumption) fails because it depletes buffers, surely the left’s instinct (tax capital, redistribute) succeeds?

No. It is worse. Much worse.

A 30% annual tax on capital gains doesn’t just redistribute wealth. It destroys the compounding mechanism itself. Every year, the tax skims 30% of any positive return. This is equivalent to reducing the effective return on capital from 8% to approximately 5.6% — but with a critical asymmetry: the tax takes on the upside, but the agent bears the full downside.

This converts an already volatile growth engine into a systematically sub-critical one. The agents can no longer outgrow their costs. The buffer — the very thing that drives survival — can never form:

The aggregate wealth didn’t just decline. It collapsed. From $1.48 billion to $32,555. That is not a typo. That is a 99.998% destruction of total wealth. The solvency rate fell from 16.7% to 8.1%. You made more people destitute, not fewer.

This is the trap that the simulation reveals with brutal clarity: annual capital taxation and consumption taxation fail for the same reason. They both attack the buffer during the accumulation phase — the precise moment when the low-SES agent is most vulnerable to the Volatility Tax and the high-SES agent is on the border of compounding wealth that ultimately benefits society. One taxes the input (consumption). The other taxes the output (returns). Both destroy the same thing: the ability to compound.

The simulation doesn’t care about your ideology. It cares about where you interrupt the compounding process.

The Insight: When You Tax Matters More Than How Much

Let’s pause on this, because it’s the key to everything that follows.

The first two prescriptions share a fatal design flaw: they are synchronous taxes. They extract revenue in real-time — every month, every year — while the agent is still trying to build the buffer that determines their survival.

Imagine a farmer planting a field. You can tax the harvest (which arrives once, at the end of the season). Or you can tax the seeds, the water, and the fertilizer — every day, as they’re applied. Oh, and lop the tops of the plants as they grow as well.

The first approach lets the crop grow. The second prevents it from ever forming.

The question is not how much to tax. The question is when.

Prescription 3: The Tax Code We Already Had

The third scenario is structurally different. It lets capital compound freely during life with zero annual capital gains tax. But at the moment of intergenerational transfer, it imposes a 50% estate tax. The revenue is redistributed as a universal dividend.

This is a deferred, asynchronous tax. It does not interrupt buffer formation. It does not destroy the compounding mechanism. It waits. It lets every agent — High SES and Low SES alike — participate in the growth engine for their entire working life and retirement. And then, at the point of dynastic transfer, it reclaims half of the accumulated surplus and recycles it into the system as new buffers.

The results are not incremental. They are transformative:

Read that table slowly.

The aggregate wealth is lower — about 26% less than the baseline. The “pie” is smaller. Every economist trained in the last fifty years will tell you this is a failure. The system is less “efficient.”

But the median — the household in the middle, the one that votes, the one that sends kids to public school — went from functionally zero to $32,703. And the solvency rate — the percentage of the population with meaningful wealth — went from 16.7% to 100%. Every single agent in the simulation is solvent.

The pie is smaller, but everyone gets a slice.

The Quintile Transformation

This is where the simulation stopped being a model and started being a before-and-after photograph of the American middle class.

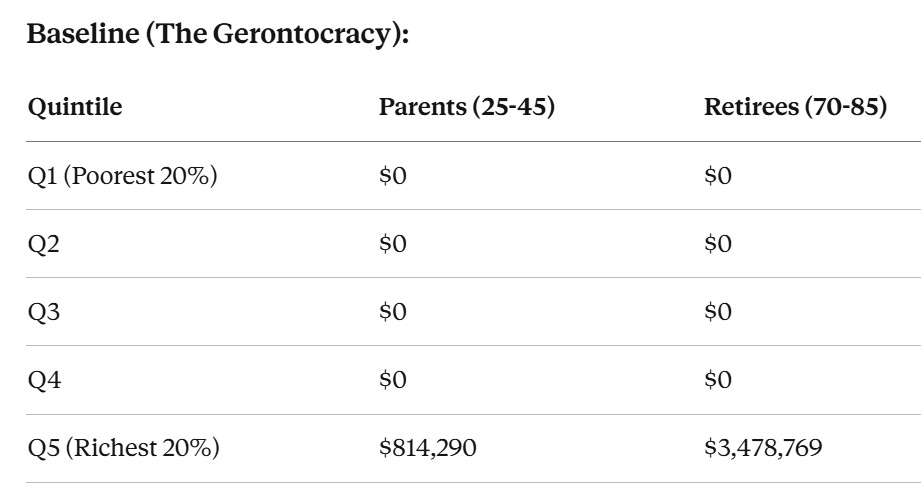

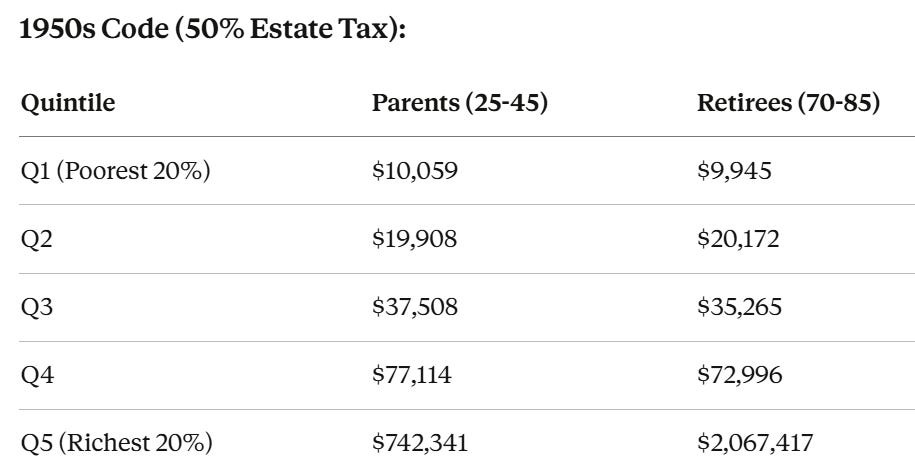

Look at those two tables, because they tell the entire story of the last seventy years of American economic history.

In the baseline, Q1 through Q4 have nothing. The bottom 80%, parents and retirees alike, are pinned to zero. All the wealth sits in Q5, and within Q5, the retirees hold 4x more than the parents. This is the Gerontocracy. This is the buffer-ocracy. This is America in 2026.

Under the 1950s code, every quintile has meaningful wealth. Q1 parents hold $10,059. That’s not luxury. But it’s a buffer — two years of breathing room. Q3 parents hold $37,508. That’s a down payment on a house. Q4 parents hold $77,114. That’s a college fund for their kids.

And look at the retirees. Under the baseline, Q5 retirees held $3.5 million, while every other retiree cohort held zero. Under the 1950s code, Q5 retirees still hold $2.1 million; they are still wealthy, but Q3 retirees hold $35,265, and Q1 retirees hold nearly $10,000. They can eat. They can live. They can care for grandchildren. They have dignity.

The 1950s code didn’t abolish wealth. It didn’t punish success. The Q5 agents are still rich. What it did was break the dynastic lock that prevented the bottom 80% from ever entering the compounding regime.

The Gini Tells the Story

For the economists in the audience, here is the same transformation expressed in the language you were trained in.

The Gini coefficient measures inequality on a scale from 0 (everyone has the same wealth) to 1 (one person has everything). The current U.S. wealth Gini is approximately 0.85 — already one of the highest in the developed world. The income Gini sits around 0.41.

In our simulation, the Gini tracks the trajectory of the system’s inequality over 100 years:

Look at the trajectories, not just the endpoints.

The baseline and orthodox scenarios march steadily toward a Gini of 0.98 — a system in which one agent holds essentially all the wealth. This is not an aberration. It is the mathematical inevitability of geometric compounding without a reset mechanism. The consumption tax doesn’t slow it down. It doesn’t even register.

The annual capital gains tax is a fascinating failure. It starts lower — a Gini of 0.50 at Year 10 because the tax successfully suppresses capital accumulation. But by Year 100, it converges to 0.97 anyway. Why? Because it destroyed the compounding engine for everyone. When nobody can build wealth, the Gini rises not because the rich got richer, but because everyone got poorer. The economy collapsed into a shared destitution that is, paradoxically, almost as unequal as the baseline — because even at the floor, the tiny differences between agents get amplified when there’s nothing left to distribute.

And then there’s the 1950s code. It is the only scenario where the Gini stabilizes. It rises to 0.87 around Year 50, then declines slightly to 0.85 by Year 100. The system finds an equilibrium. Inequality exists — it must, because agents have different ages, different compounding histories, different luck — but it is bounded. The estate tax creates a ceiling on dynastic accumulation while the universal dividend creates a floor on destitution. The system breathes.

A Gini of 0.85 is still high. But it is approximately where the U.S. wealth Gini sits today. The question is not whether we can achieve perfect equality. The question is whether we can prevent the system from converging on 0.98, where democracy itself becomes a formality.

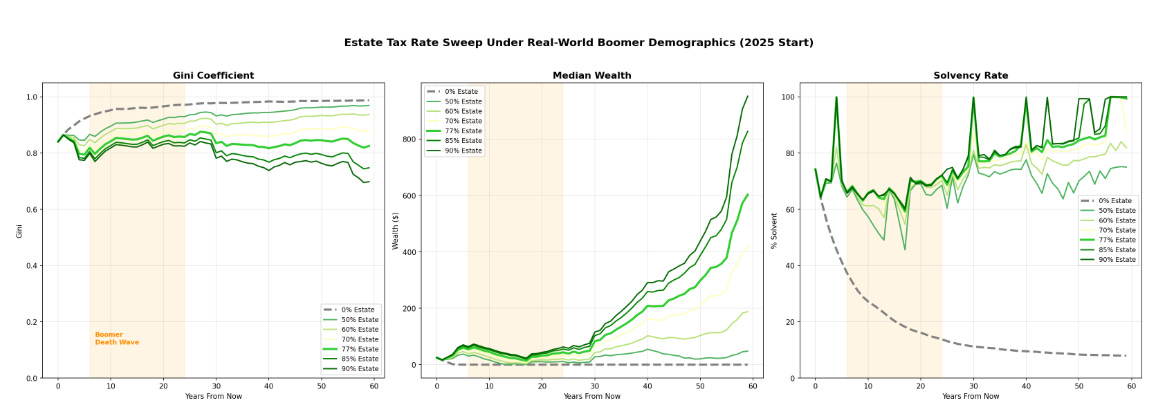

A careful reader will object: the simulation above uses a uniform age distribution. Real America in 2025 does not have a uniform age distribution. Real America has the Baby Boomers — the largest, wealthiest generation in human history — sitting on approximately $78 trillion in household wealth, aged 61 to 79, and about to die.

So we reran the simulation. Same four tax scenarios. But instead of a uniform age-wealth distribution, we initialized the population to match 2025 America: a Boomer bulge aged 61-79 holding the majority of wealth in a Pareto distribution (a few with enormous wealth, many with moderate), Gen X with moderate accumulation, Millennials with little, Gen Z with nearly nothing. The starting Gini: approximately 0.85 — exactly where the U.S. sits today.

The results are not merely different. They are alarming.

Under the baseline — no estate tax — the Boomer wealth concentration drives the Gini from 0.85 to 0.995 by Year 100. That last digit matters. At 0.98 in the uniform model, the system was already approaching feudalism. At 0.995, it has arrived. The Boomer bulge doesn’t just reproduce the inequality problem — it accelerates it, because the wealth is concentrated in agents who are still alive, still compounding, and approaching the generational boundary all at once.

And here is what alarms me: the 50% estate tax — the rate that produced 100% solvency in the uniform model — does not work under real-world demographics. The Gini under the 50% rate keeps rising straight through the Boomer death wave. It reaches 0.94 at Year 25, 0.94 at Year 40, and 0.97 by Year 60. Solvency reaches only 75%. The dividend generated by a 50% rate, spread across the entire population, is simply too thin to push agents above escape velocity when wealth is this concentrated.

The uniform model was a proof of concept. It showed that the estate tax mechanism works — deferred, asynchronous taxation at the generational boundary. But it understated the required dose. When you initialize the simulation with actual American wealth concentration, 50% is not enough.

This is why the window is now.

The Boomers hold approximately $78 trillion. They are between 61 and 79 years old. The actuarial peak of the death wave begins around 2030 and crests around 2045. Every year that passes without an effective estate tax is a year in which Boomer wealth flows into the perpetual trust architecture we described earlier — into the vampires, into South Dakota, into legal structures specifically designed to ensure that this wealth never triggers a generational transfer event.

The concentration of wealth in a single generation is not just a problem — it is an opportunity. It is the largest potential buffer-recycling event in American history. But it is a one-time event. Once the wealth has passed into perpetual trusts, the generational boundary ceases to exist, and the mechanism never fires.

We are not arguing for a policy that would be nice to have someday. We are arguing for a policy with a window of approximately fifteen years before the opportunity closes permanently.

So the question becomes: if 50% is not enough, what is?

50% Is Not Enough

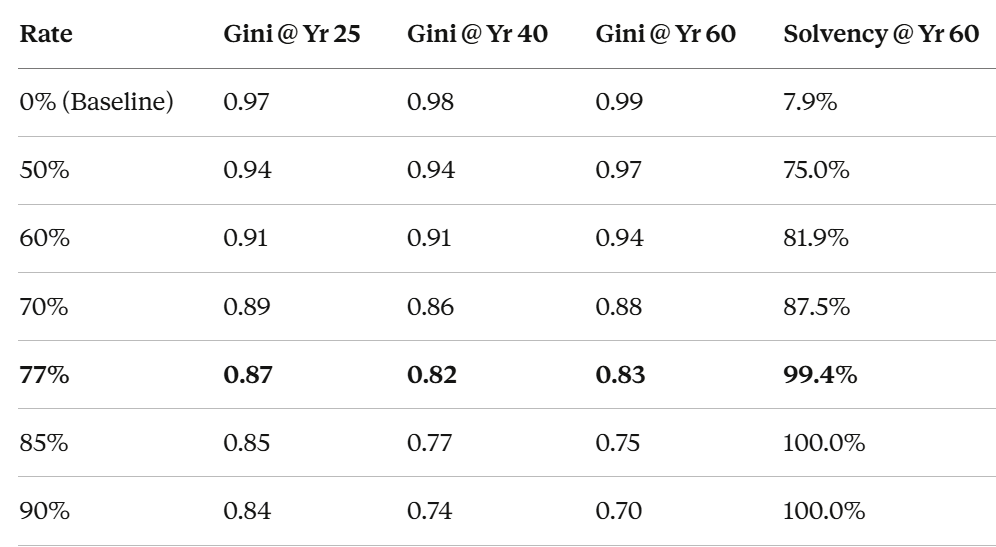

The Gini Coefficient still rises during the first 25 years of the Boomer death wave, even with a 50% estate tax. The dividend generated at a 50% rate is insufficient to push agents above escape velocity when wealth is concentrated in a single generational cohort rather than distributed uniformly across age groups.

So we swept the rate. Same Boomer demographics. Same simulation. Seven estate tax rates from 0% to 90%.

At 50%, the Gini never inflects. It keeps climbing straight through the death wave. Solvency reaches only 75% — better than the baseline, but a system that still condemns a quarter of the population to financial death.

At 70%, the Gini finally peaks and reverses — the inflection occurs around Year 25, precisely during the death wave. Solvency reaches 87.5%.

At 77% — the actual top marginal estate tax rate from 1941 to 1976 — the system achieves 99.4% solvency. The Gini peaks at 0.87, then falls to 0.82 during the death wave and stabilizes at 0.83. This is the rate at which the dividend just barely exceeds the threshold needed to push agents above escape velocity under real-world wealth concentration.

The number 77% is not arbitrary. It is the critical rate — the point at which the estate tax dividend, distributed across the population, generates enough buffer to overcome the compounding advantage of the surviving wealthy. Below it, the system improves but does not heal. Above it, the system heals, but at the cost of unnecessary compression. At 77%, it finds equilibrium.

They Knew

Here is the part of this story that stops me cold.

The top marginal estate tax rate in the United States was 77% from 1941 to 1976. Not 50%. Not 60%. Not “somewhere in the 70s.” Exactly 77%. The rate was reached through a series of legislative increases: 10% at inception in 1916, 25% in 1917, 40% in 1924, 70% in 1935, and finally 77% in 1941, where it stayed for thirty-five years.

Did the policymakers who set that rate understand the mechanism revealed by our simulation? Did they know about absorbing barriers, escape velocity thresholds, and the minimum dividend required to overcome geometric compounding under concentrated wealth?

No. Not in those terms. But they understood something arguably deeper.

In 1889, Andrew Carnegie argued that wealth did not belong to the wealthy — it was merely entrusted to them temporarily by the society that made its accumulation possible. He advocated heavy inheritance taxes and declared that a man who dies rich dies disgraced.

Theodore Roosevelt, in his 1906 address to Congress, called for an inheritance tax “increasing rapidly in amount with the size of the estate” — to prevent what he called “swollen fortunes” from perpetuating. His language anticipated our simulation’s findings almost precisely: the tax should be small on moderate estates — don’t interrupt buffer formation — and heavy on the largest — clip the dynastic tail.

Franklin Roosevelt warned in 1936 that “economic royalists” had “carved new dynasties” and that “new kingdoms were built upon concentration of control over material things.” He wanted a 100% tax on incomes above $25,000. Congress negotiated him down. The Revenue Act of 1935, called the “Soak the Rich Act” at the time, pushed the estate tax to 70%. By 1941, it reached 77%.

Keynes, writing in 1936, argued that there is “social and psychological justification for significant inequalities of incomes and wealth, but not for such large disparities as exist today.” He called for the “euthanasia of the rentier” — the functionless investor who lives off capital scarcity rather than productive effort. He explicitly advocated “a scheme of direct taxation which allows the intelligence and determination and executive skill of the financier... to be harnessed to the service of the community on reasonable terms of reward.” This is almost verbatim our distinction between taxing passive returns from luck and infrastructure while exempting active returns from skill.

Even Eisenhower — the Republican who maintained the 77% rate — warned that any society tolerating a “fabulously wealthy” class is asking for trouble.

They did not have agent-based simulations. They did not have ergodicity economics or stochastic process theory. What they had was thirty years of iterative calibration. They kept turning the dial up — 10%, 25%, 40%, 70%, 77% — because each lower setting proved insufficient to prevent dynasty formation. They were empirically converging on the same number that our simulation derives from first principles.

And before them, the Torah commanded Jubilee. The Babylonians decreed misharum. The Romans limited the concentration of ager publicus. Every durable civilization, through experience, arrived at the same structural insight: geometric accumulation requires a periodic reset at a natural boundary, and the reset must be large enough to actually recycle the buffer.

Five thousand years of civilizational experience. Three decades of American legislative calibration. And now a simulation with 5,000 agents and 1,200 monthly time steps. Three entirely independent methodologies. The same answer: approximately 77%.

Policymakers in the 1950s didn’t have our simulation. But they had something better: experience refined through iteration. And they got the number right. And then the business lobby, fronted by Reagan and Friedman, undid it.

And here is the final perversity. The ultra-wealthy already know this.

In 2010, Warren Buffett and Bill Gates launched the Giving Pledge — a commitment by billionaires to donate at least 50% of their wealth to charity during their lifetimes or at death. The remaining 50% is then, in theory, subject to the current 40% estate tax. Do the math: 50% donated, plus 40% of the remaining 50% = a 70% effective transfer rate. The billionaires are voluntarily self-prescribing an estate disposition almost identical to the rate our simulation identifies as the minimum threshold for systemic healing.

They know the wealth needs to be recycled. They just insist on choosing the recipient. The Giving Pledge routes the transfer through private philanthropy — where the donor names the building, selects the cause, retains reputational control, and employs their progeny in perpetuity — rather than through a public dividend, where the democratic process allocates the buffer. The effective rate is nearly identical. The difference is who decides.

This is not generosity. It is the last-ditch defense of allocation authority by a class that understands, intuitively if not mathematically, that the wealth must flow back. They would rather give 70% on their own terms than have 77% recycled on society’s terms.

The rich have already conceded the principle. They have merely reserved the right to administer it privately. The simulation says that’s not good enough.

Why It Works: The Buffer Recycling Mechanism

The estate tax is not a punishment. It is a buffer recycler.

Here’s the mechanism. When a wealthy individual dies, up to 77% of their accumulated capital above the exemption threshold is returned to the system as a universal dividend. That dividend does something specific and measurable: it raises the wealth of every low-SES agent above the critical threshold where compounding can begin.

Think of it in terms of our simulation’s physics. Below a certain wealth level, the Volatility Tax — unemployment shocks, restart costs, the cost of eating — consumes every dollar of surplus before it can compound. The agent is stuck in the Capital Decay Regime. No amount of talent or effort can escape it, because the math prevents escape.

The estate tax dividend pushes agents above the escape velocity. It provides the buffer that allows the compounding engine to finally engage. Once above the threshold, the agent’s own returns do the rest. The system becomes self-sustaining.

But there is a design problem that the simulation glosses over: timing risk. In the model, deaths are distributed uniformly, so the dividend flows smoothly. In reality, estate tax revenue is lumpy. A billionaire dies in 2027; the fund swells. No billionaire dies in 2028; the fund starves. A child born in 2028 receives a smaller buffer than a child born in 2027 — not because of anything about them, but because of the accident of when a stranger died. We have replaced one form of birth lottery with another.

The solution is, ironically, to use the vampire’s own weapon: a trust. Not a perpetual dynastic trust designed to hoard wealth across generations, but a public buffer trust — a sovereign fund that receives estate tax revenue, invests it in U.S. government debt, and distributes the dividend on a smoothed, predictable schedule. The trust absorbs the volatility of revenue timing and converts it into a steady stream. The same way a pension fund smooths contributions over decades to deliver predictable benefits, the buffer trust smooths the generational harvest to deliver predictable buffers.

This is not a new idea. Norway’s sovereign wealth fund, Alaska’s Permanent Fund, and Singapore’s Temasek all operate on variants of this principle — public capital pools that convert volatile revenue streams into stable citizen dividends. The mechanism is well understood. The engineering is solved. What’s missing is the revenue source, and the estate tax provides it.

This is why the solvency rate nears 100%. It’s not that the government is supporting everyone indefinitely. It’s that the buffer recycling mechanism gives everyone enough runway to support themselves. The tax code isn’t redistributing income. It is redistributing the ability to compound.

And here I need to address something directly, because it is the first objection that any fiscal conservative will raise: “You want to grow government.”

No. Emphatically, no. And this is why the universal dividend is the critical design choice, not a detail.

The federal government already spends roughly $6 trillion per year. The vast majority of that spending on social programs operates through a pass-through architecture: federal dollars flow to states, states administer benefits through local bureaucracies, and at every layer of the chain, the dollar is diminished. Administrative overhead. Compliance costs. Eligibility determinations. Case workers. Appeals processes. The bureaucratic friction that exists between a federal tax dollar and a low-SES family’s bank account is enormous — and it is a feature, not a bug, of the current system. It sustains an entire class of administrators, consultants, and state-level political operators whose livelihoods depend on the complexity of the redistribution apparatus.

We monitor charities for efficiency. A charity that spends 60 cents of every dollar on overhead and delivers 40 cents to its mission gets an F rating and donors flee. Yet the federal-to-state-to-local benefit pipeline routinely operates at comparable or worse ratios, and we call it “government spending.”

The universal dividend bypasses this entirely. It is a direct transfer. No state administration. No eligibility bureaucracy. No means testing. No case workers determining whether you are sufficiently poor to deserve a buffer. The estate tax revenue goes in; the dividend comes out. To every American citizen. Upon naturalization and age of maturity, there are catch-up distributions — so that no one is penalized for the accident of when they entered the system. The efficiency ratio approaches 1:1.

This is not a libertarian fantasy about eliminating government. Government has essential functions: defense, courts, infrastructure. Public goods that markets cannot provide. But the redistribution function — the buffer recycling mechanism — does not require a bureaucracy. It requires a ledger. And in 2026, we have the technology to maintain that ledger at trivial cost.

The simulation models this as a direct, frictionless transfer for a reason: because that is how it should work. Every dollar consumed by administrative overhead is a dollar that never becomes a buffer. Every layer of bureaucratic intermediation is a tax on the tax — a synchronous friction applied to the very mechanism we are trying to optimize. The same physics that tells us not to tax consumption during buffer formation tells us not to filter the dividend through five layers of government on its way to the recipient.

We are not proposing bigger government. We are proposing fewer intermediaries between the tax and the buffer.

The Gerontocracy Dissolves

Notice something else in the quintile tables. Under the baseline, the generational divide was obscene: Q5 retirees held $3.5 million vs. Q5 parents at $814,000 — a 4.3x ratio. Under the 50% estate tax, Q5 retirees hold $2.1 million vs. Q5 parents at $742,000 — a 2.8x ratio. A 77% rate normalizes it further still.

The Gerontocracy doesn’t vanish entirely; older agents have compounded longer, and they should be wealthier. But the 50% estate tax reduces the dynastic acceleration that turns retirees into a separate economic species. It clips the tail of the distribution at the exact point where intergenerational transfer would otherwise create an aristocracy. The 77% rate “solves it.”

The 1950s code doesn’t fight the physics. It uses physics as a judo master might use their opponent’s strength. It acknowledges that geometric compounding will always produce concentration over a lifetime, and it introduces a reset mechanism at the natural boundary between generations.

But We’ll Be LESS Wealthy!

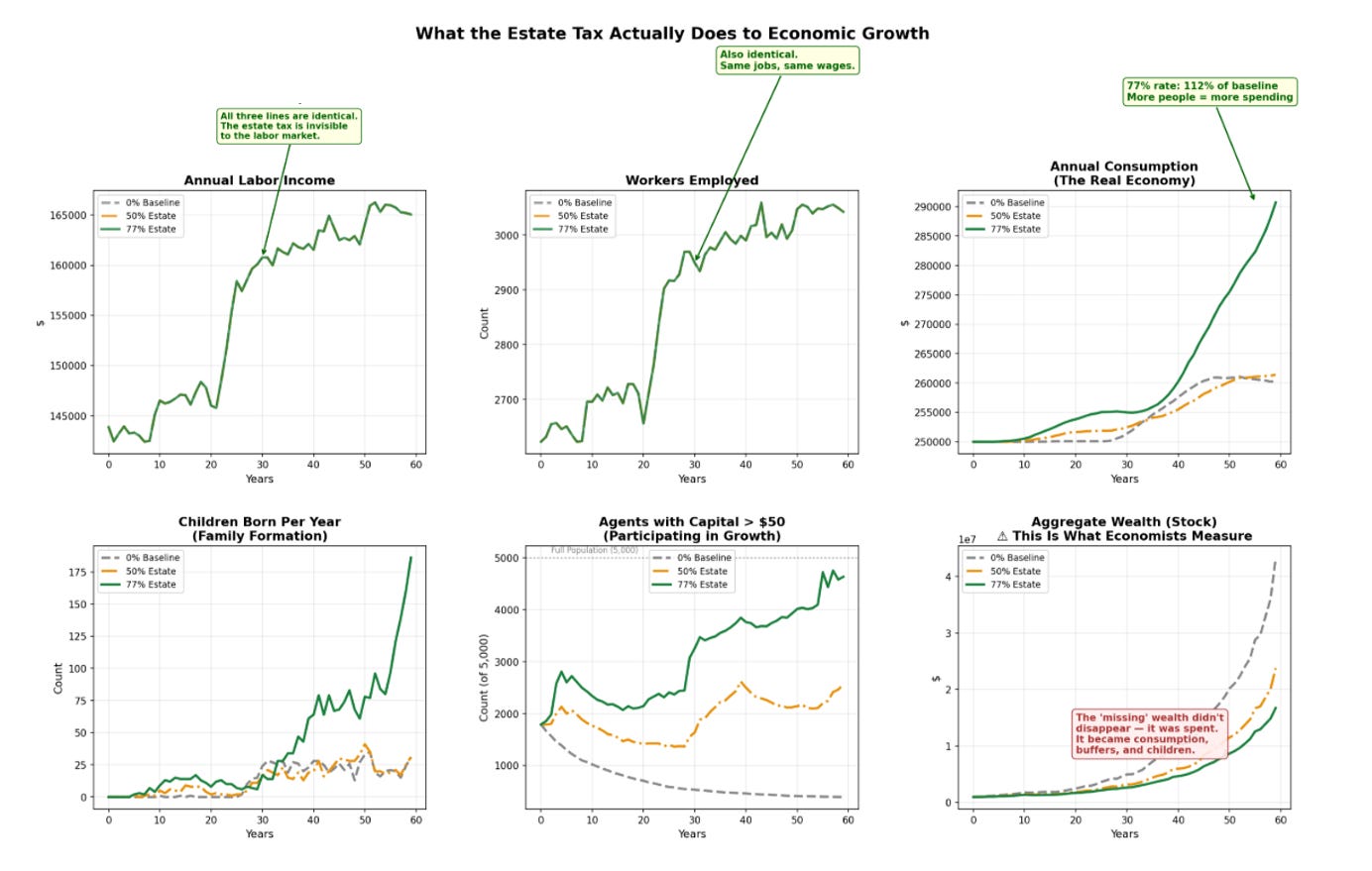

The 77% estate tax does have an unfortunate reality: the aggregate absolute wealth DOES decline versus baseline. By nearly 60%! But that’s because we’re defining wealth narrowly. Look what happens to the number of children… consumption… the number of participants with ownership stakes. You want “the ownership economy” replete with the social goods (safety, reduced crime, greater civic engagement) we were promised? This is the path. A small segment of our society will be worse off in relative terms. A not insignificant number of my readers (and my children) will be among them. But our society will be richer; our trust will be higher.

Addressing Sandy’s Objection

One of the most thoughtful comments on Part 2 came from Sandy, who raised a structural point I want to address directly. Sandy argued that the 1950s tax code was the last layer of a multi-layer buffer system: manufacturing employment providing wage floors, unions providing surplus transfer, employer benefits providing non-wage buffers, and then the tax code compressing top-quintile decoupling. Today, three of those four layers are gone.

The estate tax is the only one of the four mechanisms that works through the compounding channel. Unions and manufacturing provide income floors — they raise the salary line at the risk of higher unemployment. Employer benefits reduce the cost line, but the predictable risk is that they lock workers into coercive relationships. The estate tax operates on neither. It operates on the starting condition — the buffer, the endowment, the initial coordinate that our simulation has shown is THE driver of lifetime outcomes.

The other three layers address symptoms. The estate tax addresses the root cause.

You can have unions without an estate tax and get a strong middle class for one generation. But without the estate tax, the dynastic compounding eventually overwhelms every other buffer. The aristocracy reconstitutes itself. Which is, of course, exactly what happened in the real world.

The political obstacles to this reform are real — we'll return to them. But first, the mechanism requires more than a tax rate.

But the Vampires Already Thought of This

I can hear the objection already: “The estate tax exists. We already have one. It doesn’t work.”

And that objection is correct — but not for the reason most people think.

Regular readers will recall my January 2025 piece, “The Undead Among Us,” where I detailed how the American elite effectively achieved immortality through legal engineering. The estate tax has a statutory rate of 40%. The effective rate is approximately zero. And the mechanism by which this was accomplished is one of the most elegant pieces of financial engineering in history — far more impressive than anything Wall Street has produced.

It starts with the Generation-Skipping Trust (GST). Prior to 1986, English and subsequently American law had limited trusts to 21 years past the death of the creator — the Rule Against Perpetuities. This was not an accident. For 500 years, the common law understood that allowing wealth to compound in perpetuity, beyond the reach of any living person’s judgment, was a threat to the social order.

Then came the 1986 tax reform, which created a GST tax exemption. The idea was modest: allow a small amount to pass to grandchildren without double taxation. But it opened a door. Almost simultaneously, states began competing to attract trust business by abolishing the Rule Against Perpetuities. South Dakota won the race to the bottom. Today, South Dakota — a state most people associate with plains and cold weather — holds more than twice the banking assets of New York. $3.4 trillion vs. $1.7 trillion. It is the world capital of the perpetual trust.

Here is what a perpetual trust does in the language of our simulation: it removes the generational boundary entirely. The agent never dies. Its wealth compounds forever. It pays no estate tax because there is no estate — the trust owns the assets, and the trust is immortal. It pays no capital gains tax because nothing is ever sold — the trust distributes income while the principal compounds untouched. The step-up in basis at death? Irrelevant. There is no death.

In our simulation, the estate tax works because every agent dies at 85 and the wealth is recycled. In reality, the Q5 retirees figured out how to become vampires. They created a legal structure that compounds like a corporation — forever — while being taxed like a dead person — never. And like Chicago, the “undead” get to vote through Citizens United.

The 1950s tax code worked because the vampires hadn’t been invented yet. The Rule Against Perpetuities was still intact. Trusts expired. Wealth was recycled. The generational boundary was real. Today, it is fictional, and the estate tax is a Maginot Line — impressive on paper, trivially circumvented in practice.

So our simulation tells us the mechanism that works. But to implement it, we need to slay the vampires first.

The Complete Prescription

The simulation has identified the core principle: tax at the generational boundary, not during accumulation. But the real world has created legal structures specifically designed to eliminate that boundary. A complete reform must address not just the tax rate, but the avoidance architecture that renders it meaningless.

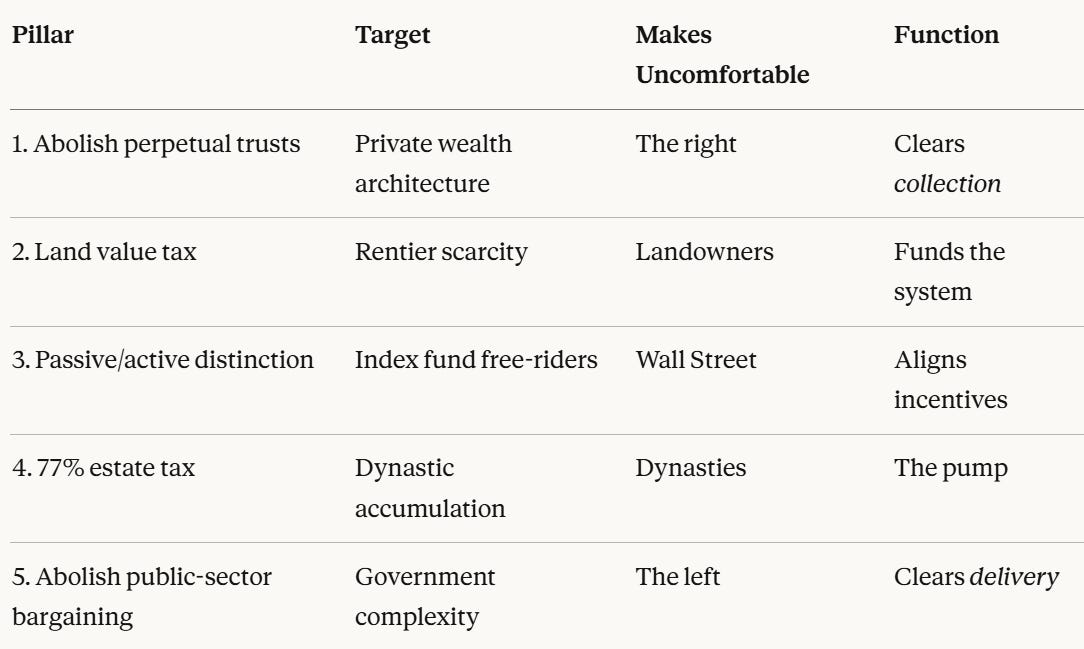

Here are the five pillars:

With detail:

Pillar 1: Restore the Generational Boundary

Abolish perpetual trusts. Restore the Rule Against Perpetuities — the 500-year-old principle that trusts must terminate within a generation of their creator’s death. Eliminate the GST tax exemption. Every dollar of wealth must eventually pass through the generational boundary where the estate tax applies. No exceptions. No South Dakota. No vampires.

This is not radical. This is restoration. For half a millennium, Anglo-American law understood that immortal wealth was incompatible with a free society. We abandoned that principle in a fit of deregulatory enthusiasm in the 1980s, and we are living in the wreckage.

Pillar 2: Tax Scarcity, Reward Development — The Land Value Tax

Henry George figured this out in 1879, and the economics profession has spent 150 years pretending he didn’t. A land value tax — a tax on the unimproved value of land, not on the buildings or improvements upon it — is the only tax in existence that even Milton Friedman called “the least bad tax.” I’ll add more to this discussion in future pieces, but grant me the grace to consider it for now despite the lack of simulation.

Land value is not created by the landowner. It is created by the community — by the roads, the schools, the hospitals, the neighbors, the economic activity that surrounds the parcel. When a landowner’s property appreciates because a new subway stop is built nearby, that appreciation is pure societal luck. It is the equivalent of our simulation’s “Luck Bucket.” Taxing it does not interrupt buffer formation, because the landowner did nothing to create it. It is a tax on scarcity rent, not on productive effort.

Better yet, the LVT actually encourages development. A vacant lot in Manhattan and a skyscraper on an adjacent lot of the same size pay the same land tax. The skyscraper pays nothing additional for the improvement. This reverses the perverse incentive of our current property tax system, which penalizes building and rewards holding empty land as a speculative asset.

In the language of our simulation, the LVT is an asynchronous tax on positional scarcity — it extracts revenue from a source that cannot flee, cannot be hidden in South Dakota, and whose taxation does not destroy productive incentive. It is the ideal complement to the estate tax.

Pillar 3: Distinguish Luck from Skill — Passive vs. Active Investment

This is where we connect directly to the work I’ve been doing on passive investing for the past decade.

Our simulation treats all capital returns identically — 8% with 25% volatility. But in the real world, there is a critical distinction between active investment (selecting companies, building businesses, allocating capital based on judgment) and passive investment (buying an index fund that mechanically allocates capital based on market weight).

Active investing is an attempt at skill. It can fail. It adds information to markets. It performs the essential capitalist function of price discovery — directing capital toward productive enterprises and away from unproductive ones. In the language of our simulation, the active investor is the “Gifted” agent: high return, high risk, high social value.

Passive investing is societal luck. The passive investor makes no judgment about which companies deserve capital. They buy everything in proportion to its existing size. They are, in the language of our simulation, free-riding on the price discovery performed by others. And as I’ve documented extensively, when passive investing exceeds a critical threshold — roughly 40-50% of total flows — it creates a mechanical feedback loop that inflates prices based on index weight rather than fundamentals. The Price-Weight Spiral.

The tax code should reflect this distinction. Active capital gains — from businesses you built, stocks you selected, risks you took — should be taxed lightly during life and at the generational boundary at death. Passive capital gains — from index funds that mechanically benefit from the societal infrastructure of price discovery without contributing to it — should be taxed at a higher rate. Not because passive investors are bad people, but because the return is a social externality that the investor did not create.

This is the same logic as the land value tax: tax the returns from luck and societal infrastructure. Exempt the returns from effort and skill. Both Henry George and Adam Smith would approve.

Pillar 4: The Estate Tax That Actually Works

With Pillars 1-3 in place, the estate tax can finally function as the simulation predicts. A progressive estate tax reaching 77% on the largest estates — the actual rate that prevailed from 1941 to 1976 — with no step-up in basis, no GST exemption, no perpetual trust escape hatch. Revenue recycled as a universal buffer dividend. Our rate sweep under real-world Boomer demographics shows that 50% is not enough — it achieves only 75% solvency when wealth is concentrated in a single generation. The 77% rate is the critical threshold: the point at which the dividend just barely exceeds escape velocity for the bottom quintiles. Below it, the system improves but does not heal. At 77%, solvency reaches 99.4%, and the Gini inflects and reverses during the death wave.

The key insight is that the estate tax alone is insufficient without closing the immortality loopholes on the collection side and the bureaucratic friction on the delivery side. But with both cleared, it is transformative. The expectation that each successive generation should expect to do better than their parents is restored.

Pillar 5: Abolish Public-Sector Collective Bargaining — Clear the Delivery Channel

This is the pillar that will make the left uncomfortable, just as Pillar 1 makes the right uncomfortable. Good. Discomfort is symmetry.

The simulation models the universal dividend as a frictionless transfer — estate tax revenue divided equally, deposited directly. The real world interposes a bureaucracy between the tax and the buffer, and that bureaucracy has, since 1962, been unionized. Kennedy’s Executive Order 10988 granted federal employees collective bargaining rights. The political logic was impeccable: it built a permanent Democratic coalition. The economic logic was catastrophic: it created a constituency whose employment relies on the complexity of the redistribution architecture.

Every means test requires a case worker. Every eligibility determination requires an appeals process. Every layer of federal-to-state-to-local pass-through requires administrators at each level. The universal dividend eliminates all of them. It replaces an army with a ledger. And the army, understandably, will fight.

This is not an argument that public employees are lazy or undeserving. It is a structural observation identical in form to Pillar 1. Perpetual trusts are a private architecture that prevents wealth from reaching the generational boundary where the estate tax can harvest it. Public-sector bargaining rights are the public architecture that prevents the harvested revenue from reaching the citizen as an efficient buffer. One blocks collection. The other blocks delivery. Both must be dismantled for the mechanism to work.

FDR, notably, agreed. He explicitly opposed collective bargaining for public employees, writing that “the process of collective bargaining, as usually understood, cannot be transplanted into the public service.” The 1950s policymakers who built the tax code our simulation rediscovered did not build it on top of a unionized delivery mechanism. Kennedy added that layer later, selling out the taxpayer for electoral victory, and the efficiency of every social program has suffered since.

The Synthesis

Let me pull this together, because the five pillars are not independent policies. They are a system — each addressing a different failure mode that our simulation has identified.

The estate tax addresses the core problem: dynastic compounding across generations. It is the generational reset mechanism.

Abolishing perpetual trusts prevents the legal circumvention of the generational boundary. It ensures that the estate tax actually collects.

The land value tax provides revenue from a non-distortionary source — scarcity rent that the owner did not create — without interrupting buffer formation during the accumulation phase.

The passive/active distinction aligns the tax code with the economic function of capital allocation — rewarding skill and price discovery, taxing free-riding on societal infrastructure.

Abolishing public-sector collective bargaining clears the delivery channel, ensuring that the collected revenue actually reaches citizens as buffers rather than being consumed by administrative friction. It ensures that the estate tax actually arrives.

Pillars 1 and 5 are mirror images: one dismantles the private immortality architecture that blocks collection, the other dismantles the public complexity architecture that blocks delivery. Together, they create an unobstructed channel from the generational boundary to the citizen’s account. The estate tax is the pump. The pillars clear the pipes.

Together, the five form a coherent system that respects the physics of geometric growth while preventing the inevitable concentration that uninterrupted compounding produces. They do not punish success. They do redistribute income — let’s be honest about that. But they redistribute it with a specific purpose: not to provide consumption, but to create buffers. To give the next generation a starting condition from which compounding can begin. The distinction is not whether redistribution occurs, but whether the redistribution creates the capacity to compound rather than merely the capacity to consume.

And critically, for those inclined toward the Charles Murray objection: bad decisions are still penalized under this system. The buffer is not a guarantee of outcomes. It is a guarantee of survivable mistakes. A kid from Q1 who picks the wrong degree financed with $80,000 in debt is not “learning a valuable lesson.” He is experiencing a catastrophic, irreversible shock that the simulation tells us pushes agents below the absorbing barrier from which there is no recovery. The same kid from Q5 who makes the same mistake? His family writes a check or calls a friend. He resets. He tries again. He compounds.

The system we are proposing does not eliminate consequences. It eliminates the asymmetry where identical mistakes produce recoverable setbacks for the wealthy and permanent financial death for everyone else. It gives low-SES kids — and their families — the same reset that wealthy families already provide privately. The conservative who objects to this is not defending meritocracy. He is defending a system in which the punishment for being eighteen and wrong is lifelong, but only if your parents are poor.

The Political Economy Problem

Now the hard part.

The simulation can derive the optimal system. It cannot implement it. And this is where I must be honest with you, because the political economy problem is genuinely harder than the policy design problem.

The estate tax was effectively dismantled between 1981 and 2017 — from a top rate of 77% with a $175,000 exemption to a top rate of 40% with an $11 million exemption. The perpetual trust was created. The GST exemption was expanded. The step-up in basis at death was preserved. Each of these changes was the product of a fifty-year campaign by precisely the cohort that our simulation identifies as the primary beneficiary of the Gerontocracy: wealthy retirees in Q5. They funded the think tanks. They wrote the talking points. They convinced the bottom 80% — the people harmed by the policy — to vote for it, using the language of “family farms” and “death taxes” and “double taxation.”

It was, as Sandy noted in the comments to Part 2, strategically coherent. You cannot sustain low capital taxation if unions retain the power to recapture surplus at the point of production. So you dismantle unions first. Then you dismantle the estate tax. Then you create the perpetual trust. Then you cut capital gains rates. Each step is logically prerequisite to the next. Whether it was explicitly coordinated is irrelevant — the sequence was functionally optimal for the beneficiary class.

This creates what I’d call the Reform Paradox: the cohort with the resources to fund political change is the cohort that benefits from the current structure. And the cohort that would benefit from reform — the Sandwich Generation, the buffer-less workers, the Low SES agents trapped in the Capital Decay Regime — has neither the capital nor the political bandwidth to organize. They are too busy surviving.

Systems that reproduce their own conditions across generations are not typically reformed from within by the cohorts they disadvantage.

But they are occasionally reformed from without — by coalitions organized around clarity rather than ideology. The New Deal was one such moment. The physics haven’t changed. The design problem is solved. The question is whether enough people understand the mechanism to demand its implementation.

Left and right have been arguing about redistribution for fifty years. The simulation shows that the argument is malformed. This is not about taking from the rich and giving to the poor. It is about when you tax, not how much. Let capital compound. Let people build. Let the Ferrari run on fresh asphalt. And at the natural generational boundary, recycle the buffer so the next generation can run too.

This is not socialism. It is not libertarianism. It is the mechanical insight that a system governed by geometric growth and volatility requires a periodic reset at the point of intergenerational transfer, or it will inevitably produce an aristocracy.

This is not even a new idea. It is arguably the oldest economic idea in civilization. The Torah commands a Jubilee every fifty years — debts forgiven, land returned to its original holders, slaves freed. Leviticus 25:10: “Consecrate the fiftieth year and proclaim liberty throughout the land.” The Babylonians practiced misharum — periodic royal edicts canceling debts and resetting economic claims. Roman law limited the concentration of ager publicus — public land — in private hands, and the failure to enforce those limits was, by the republic’s own historians, a proximate cause of its collapse.

Every durable civilization in recorded history understood that geometric accumulation, left unchecked, eventually consumes the society that enables it. They didn’t have simulations. They had experience. And they arrived at the same answer: a periodic reset at a natural boundary.

The Founders understood this. Jefferson wrote about it. Adams warned against it. And for thirty years — from roughly 1945 to 1975 — we actually built it.

We can build it again. But only if we stop treating the economy as a morality play and start treating it as what it is: a physical system with knowable dynamics and designable interventions.

This concludes the Summer Slide Economy series. The full executable code for all simulations, including the tax policy scenarios in this piece, is available here. The code runs in Google AiStudio or any Python environment with numpy and matplotlib.

If you found this series valuable, please share it. The paywall is down. The argument is free. The only question is whether enough people hear it.