The Summer Slide Part 2: The Rise of the Gerontocracy

When “Eating” Became a Luxury and Retirement Became a Weapon

Last week, in Part 1, we ran a simulation that broke the meritocratic narrative. Today’s piece continues to refer back to the code provided in this post. There is a TON of interesting market action, but I’m going to send those observations out in a separate note on Monday. This is already too long, and I’m past my self-imposed deadline. As many paying readers have requested, I’m placing the paywall below the entire piece. It’s a quirk of Substack that excluding the paywall limits distribution. I thank all of my paying readers for subsidizing these notes. Your generosity is appreciated.

A Quick Review

Last week, we showed that in a world governed by geometric growth and volatility, talent doesn’t win—buffers do. The “Gifted Poor” went extinct at 25x the rate of the “Normie Rich.” The market selected for safety, not skill. The Ferrari broke an axle on the dirt road.

But that simulation was still a game. The agents didn’t eat. They didn’t have children. They didn’t retire.

This week, we add all three. And the model stops looking like a thought experiment, and it starts looking like a census report.

Phase 3: The Volatility Trap (or, “Why You Can’t Save Your Way Out”)

In Phases 1 and 2, our agents lived in a frictionless world. They bet, they won or lost, and the only cost was the bet itself. But in the real economy, you have to eat—every single day, whether you won or lost.

So we introduced the physical requirement of survival.

The Setup:

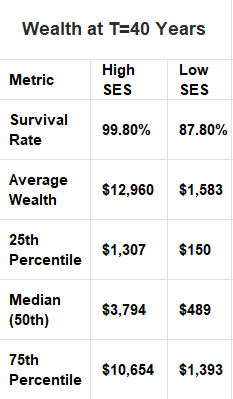

We gave every agent a job paying $55/year and a non-negotiable cost-of-living allowance of $50/year. That’s a theoretical 10% savings rate—generous by American standards. We then introduced a realistic unemployment shock: a 4% steady-state rate with a 3-month average duration.

Here’s the critical addition: re-employment isn’t free. Every restart costs $10—the new clothes, the lost security deposit, the COBRA payment, the repo’d car. That’s the “Restart Haircut.” It’s a small number that produces catastrophic results.

We split our agents into two classes. Not by talent—everyone is equally skilled. The only difference is the starting buffer:

High SES (high socioeconomic status): Starts with $500. Ten years of breathing room.

Low SES: Starts with $50. Exactly one year of subsistence.

The Result: A massive widening of outcomes.

Importantly, note that we are assuming 100 years(!). The compounding eventually takes over, which is an important clue to our current gerontocracy. But with only a 40-year working life, the median low-SES ends up worse off than they started. Less than 10% of high-SES people end up worse off than they started.

The High SES group compounding is nearly uninterrupted. Their buffer absorbs decades of shocks. They barely notice unemployment, the way you barely notice a pothole in an SUV.

The Low SES group enters what we can call the Capital Decay Regime. For the unlucky agent, the Restart Haircut and the unemployment shocks overwhelm the 10% savings rate. They spend their working lives recovering from the previous restart rather than compounding. Two unemployment events in a decade—which is not unusual, it is average—is enough to drive their wealth to zero.

The survival rates are the most damning output. The High SES group: near 100%. The Low SES group: nearly 13% ruin rate (bankrupt). And remember this is with a constant 4% unemployment rate — near the lowest in history. Same talent. Same work ethic. Same economy. Different starting coordinates. Different outcomes.

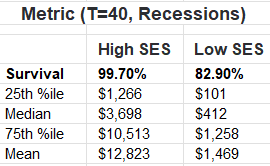

If we introduce recessions every 10 years, with unemployment rising to 8% and the duration of unemployment during recessions doubling to 6 months. Look familiar?

The Insight: Redundancy—starting wealth—is THE driver of outcomes. Without a buffer, the low-wealth agent is trapped in a sub-critical regime where growth is challenged, regardless of skill or effort. We have built a system where the “Cost of Survival” is set by the average, but the “Ability to Survive” is denied to the median.

I want to pause on that, because it maps perfectly to the empirical data.

When researchers decompose the White-Black lifetime earnings gap, two factors explain the overwhelming majority of the differential at the low end: years of full-time work (largely a proxy for unemployment frequency) and possession of health insurance. Not education. Not “grit.” Not IQ. Time in the game and a buffer against medical ruin.

At the 85th percentile—the high-outcome cohort—these factors explain almost nothing. Why? Because by definition, the people at the top already have the buffers. The variance has been absorbed. Of course, “they” think talent explains everything and that meritocracy asserts itself over time; unfortunately, we readers of YIGAF know that to be “untrue.” From the summit, the road looks smooth, and we can comfort ourselves that we “deserve” what we’ve made.

This is also why wealthy people don’t want to pay for universal healthcare. They literally cannot see the point. Their buffer makes the problem invisible.

Phase 4: The Sandwich Generation

Having established that buffers drive outcomes more than talent, we asked the obvious next question: What happens over a lifetime? Not just one agent’s lifetime—across generations.

We added three things that economists love to model in the abstract but rarely simulate in combination: children, retirement, and inheritance.

The Rules:

The Inheritance Gap: High-SES children enter the workforce at 20 with a $500 buffer (their parents’ gift). Low-SES children enter with $0.

The Parent Trap: You can only have a child if your wealth exceeds $375—roughly three years of subsistence. Each child costs $25/year for 18 years. Maximum three children.

The Sandwich Transfer: Workers pay 10% of their salary to a retiree pool. Think of it as Social Security, Medicare, and the informal family obligations combined.

Retirement: At 70, your salary disappears. You survive on accumulated capital (still compounding at 8%) and the transfer pool.

We ran this for 100 years—a full “Post-New Deal Era.”

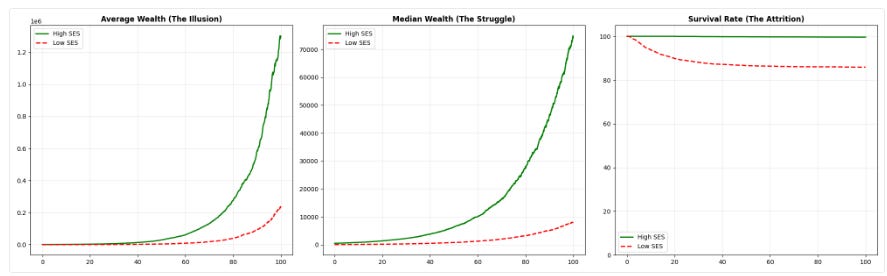

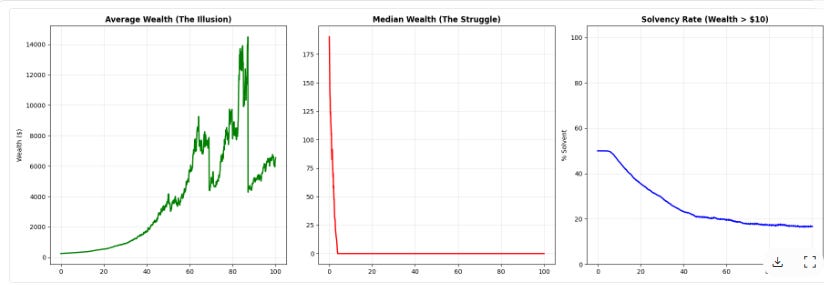

The First Graph: Average vs. Median

The Average Wealth line shoots upward. If you were an economist looking at aggregate GDP, you would say the system is working. The pie is growing. As Nick Maggiulli correctly points out, the average wealth is disrupted by inheritance dilution, but the family wealth continues to compound.

The Median Wealth line crashes and flatlines. The typical household—the one in the middle, the one that votes, the one that sends kids to public school—cannot compound. The combination of child costs, the retiree transfer, and the ever-present unemployment shock consumes every dollar of surplus before it can grow.

This is the Ensemble Illusion. The average is being pulled upward by the top 1%, whose buffers are so large that they operate in a fundamentally different economy. The median is treading water. And the bottom quartiles are drowning. It’s an America where “we’ve never been richer” and “59% of households can’t afford a $1,000 emergency expense.”

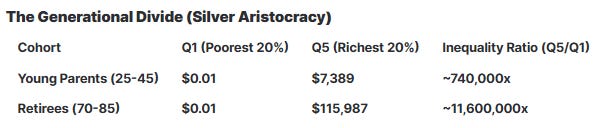

The Second Graph: The Quintile Breakdown

This is where the simulation stopped being a model and started being a photograph.

When we broke the terminal wealth into quintiles and compared Parents (ages 25-45) against Retirees (ages 70-85), the picture was devastating.

Q1 through Q4: There is no meaningful difference between working-age parents and retirees in the bottom 80% of the economy. Both groups are pinned to the subsistence floor. The 10% transfer and the 8% capital returns are insufficient to lift the median retiree out of the Capital Decay regime. If you didn’t enter retirement with a massive buffer, you’re just as broke as the young family down the street.

Q5—The Decoupling: The only meaningful wealth accumulation happens in the top 20%. And within that quintile, the Retirees pull away from everyone else. They are the only cohort with enough capital to actually benefit from 50 years of compounding. They receive the transfer payments. They consume a shrinking fraction of their wealth. They have zero dependent costs—their children are grown. They don’t work, so they take no unemployment shocks.

They have become Capital.

Not “people who have capital.” Capital itself. A wealth object that compounds, extracts, and never resets.

The most profitable strategy in our simulation wasn’t to invent the future. It was to have already invented it 40 years ago and get “lucky.”

The Gerontocracy Is Not a Metaphor

We have inadvertently created a society in which the old hold all the capital, and the young are burned as fuel to keep them warm.

This isn’t generational warfare rhetoric. It’s the physics of the system.

The retiree class in Q5 benefits from every feature of the economy simultaneously: compound returns on a large base, transfer payments funded by workers, zero labor risk, zero child costs, and—here’s the kicker—preferential tax treatment on capital gains. The step-up in basis at death means that a lifetime of untaxed gains can be passed to heirs with the tax liability erased entirely.

Meanwhile, the Sandwich Generation (ages 30-50) is simultaneously funding:

Their own rent (Cost of Living)

Their children ($25/year per child for 18 years)

The retiree transfer (10% of salary)

The restart risk (unemployment shocks with no buffer)

They are paying for everything and compounding nothing.

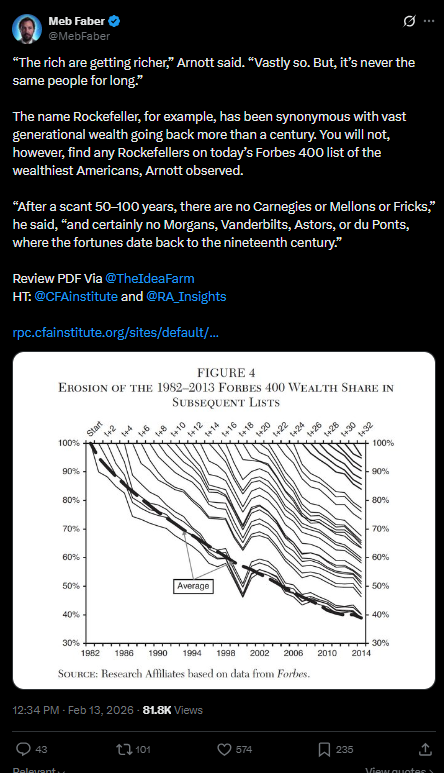

I recently saw Rob Arnott present data showing the “declining fortunes” of wealthy individuals across generations and label it “hopeful”—evidence that wealth doesn’t persist. But he misread his own data. What he was seeing wasn’t degradation; it was inheritance dilution. The family dynasty’s wealth continues to compound. It’s just being split across more heirs. The per capita decline is an illusion. The dynastic wealth is growing faster than ever.

The Mechanism We Refuse to See

What our simulation reveals is that the American economy has a caste system, and it is not based on race, gender, or even education. It is based on Redundancy at birth.

If you enter the labor market with a buffer—parental wealth, a paid-for education, a family home to fall back on—you can survive the volatility. You can take risks. You can fail and try again. You can be a Ferrari on fresh asphalt.

If you enter without one, the math is against you from day one. You are not lazy. You are not untalented. You are simply operating in a sub-critical regime where the physics of geometric growth cannot help you, because every dollar of surplus is consumed by the cost of survival before it can compound.

We haven’t built a meritocracy. We’ve built a buffer-ocracy. And the biggest buffer of all is age—specifically, having been born early enough to accumulate capital before the ladder was pulled up.

The Cliffhanger

We have now diagnosed the disease: a system that selects for starting resources over talent, that concentrates wealth in retirees, and that traps the working-age population in a subsistence loop.

The obvious question was: Can you tax your way out of this?

I expected the answer to be simple. It wasn’t.

When we tested the reform that both libertarians and orthodox economists call “optimal”—cutting taxes on capital and raising them on consumption—the system didn’t just fail to improve. It got worse.

But when we tested a different structure entirely—one that most policy experts would dismiss as politically impossible—the simulation independently derived something remarkable: the tax code of the 1950s.

Part 3: “The Tax Code We Already Had” next week.