kNAVes and Fools...

The impact of higher interest rates on private equity-owned businesses is being obscured by leverage on leverage

Summary:

The recent “largest-ever private credit debt deal” reveals much about the dynamics underpinning private equity growth.

PE fund returns appear to deliver good returns on paper, but these are misleading. Using broad public equity benchmark CAGRs versus sector specific IRRs is absurd. Using more appropriate benchmarks, performance is often lackluster, particularly when considering the leverage involved in their investments.

The growing use of net asset value (NAV) loans, which optically reduce portfolio company leverage by borrowing at the fund level are the latest trick to hide an inevitable repricing of underlying asset values. LPs are being abused by agency issues.

Increasingly, private equity investments are essentially "all the worst aspects of public investing with leverage on leverage." The designation of “private” investments is simply a marketing pitch as LPs lack control over BOTH fund managers and the portfolio companies while receiving a fraction of the information available on public companies.

What I’m Reading/Listening to

This coming week is a travel week and I’m candidly a bit behind. It’s reduced my freedom to listen and read which makes me grumpy. With that said, I really enjoyed listening to my partner, Harley Bassman, on the latest Macro Voices. While I still believe Harley is dead wrong on his inflation narrative, he’s in good company and he has been brilliant in his formulation of strategies to take advantage of the opportunities created by interest rate markets. Just like he correctly intuited the opportunity to buy payer swaptions in rates (long delta and vol), he’s now highlighting the opportunity created to be SHORT convexity and rate vol via deeply depressed mortgage-backed securities pricing. I agree with him that this is one of many “alligator jaws” destined to close. My bias is it will close through higher IG spreads and lower yields (and Harley being early on MBS spreads), but with mortgages I believe Harley is spot on in noting that refinancing risk is overblown. The underlying note can be found here:

Top Comment:

Zach: With artificially high corporate interest rates drying up debt issuance we should see reduced capex and therefore slower growth. Is it reasonable to think that with expanding equity multiples the decade plus of stock buybacks will reverse as new stock issuance becomes the most plausible place to raise cash in a slowing economy and high borrowing costs? The increase in public stock supply could be a final variable that rebalances the equation resulting in the ultimate payoff for bondholders. Is that a reasonable or even possible expectation?

MWG: Zach, I think this is already happening in many ways and is “somewhat” the subject of this week’s note (“equity” injections in private equity). A similar event happened with Carvana where a “successful” equity raise was accomplished with the founding con-man, sorry car-man, contributing half the equity proceeds at a premium to the existing stock price. But this is likely to occur at the lower end of the stock market capitalization; the mega-caps, ex-Tesla, seem largely immune for now.

The Main Event

This week’s note takes a break from the deeply theoretical concepts of last week to express a bit of populist outrage at yet another growing abuse in the PE space. This past month saw a new record private credit debt deal close as Vista Equity Partners refinanced the debt of Finastra, a financial services software roll-up that has been privately held by Vista in one form or another since 2007. Remember that private equity funds are typically given a 10-year expected life and that it is now 2023. Perhaps I’ve been inspired by my recent reading of John Coates, “The Problem of 12” as noted in my post “Sahm Rules are Better than Others”.

Finastra was formed by the merger of David & Harris (D+H) and Vista portfolio company Misys in 2017. At the time, D+H had $1.5B in revenue. The last publicly disclosed revenue for Misys was in January 2012 when it reported six-month revenue of $320MM. It merged with another Vista portfolio company, Turaz, that year. Vista acquired Turaz from Thomson Reuters earlier that same year (Feb 2012). No revenue level was disclosed for Turaz, although at the time it was described as “already a very successful business in its own right” with “offices worldwide” and employing over 1,000 skilled professionals. Quick back-of-the-envelope math suggests at LEAST $200MM in revenue. I apologize for the sketchy data, but there is only so much a public fund manager can find out about “private” assets.

So let’s just do a quick summary of the Turaz+Misys+D+H revenue combination:

Entities with a combined revenue of roughly $2.34B when the deals were announced, with zero organic growth (and ignoring additional acquisitions made along the way), should have roughly $2.91B in revenue today. But of course, we know it’s better than that, because Vista adds value to its acquisitions:

Asked whether the merger with Turaz would lead to job losses, (acting Misys CEO) Kilroy said: "The direction of travel is the other way. Vista buy and grow software companies. The way they operate is to make companies more successful by sharing best practice about how to run them well."

Vista founder, Robert Smith, reiterated this growth focus in 2012, citing their deep experience with enterprise software:

Vista's chairman and chief executive, Robert Smith, said: "Through our deep experience with enterprise software companies, we believe that Misys has an attractive future that we plan to invest in and grow. With the combination of Misys and Turaz, one of our existing portfolio companies, we are creating the global leader in core banking, treasury management, capital markets and enterprise risk management software headquartered in the global banking centre, London."

This analysis receives further support from the Bureau of Economic Advisors (BEA) which tells us that real spending on computer software has risen 500% since 2011 and is up nearly 3x since 2017. And so a decade later, amidst a boom in fintech and software, not to mention further acquisitions, it comes as no surprise that Vista has managed to grow Finastera to $1.85B in revenues.

Note this meme is now a recurring feature to YIGAF… OK… time for a vote:

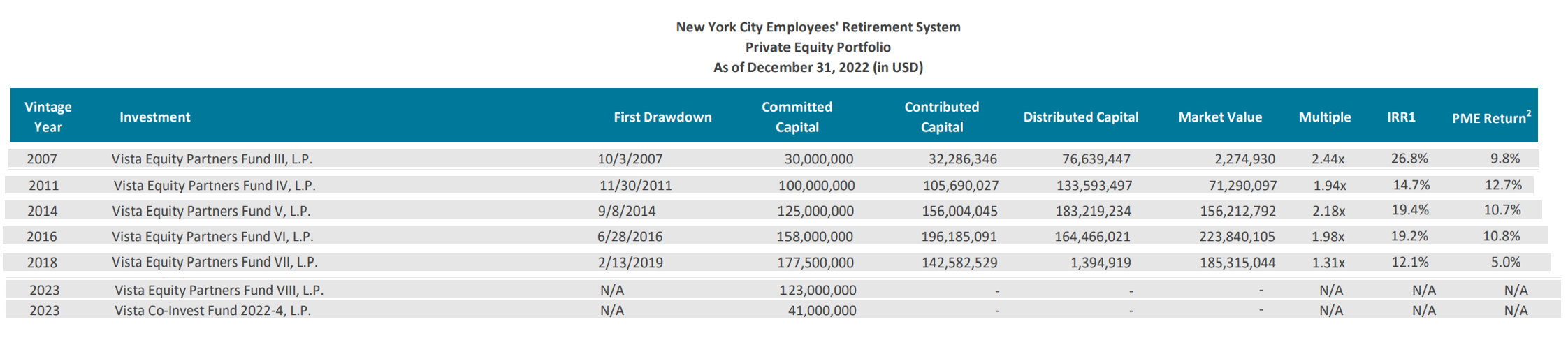

OK, so it’s not working out so well. But that’s been OK for Vista, which has managed to raise over $60B over the last decade. How’s it working out for investors in Vista funds? Well, using industry metrics, it seems pretty good. The Vista Fund IV which acquired Turaz and Misys has delivered a 14.7% IRR through Dec 2022 according to the NY City Employee’s Retirement System. Please note I am not uniquely criticizing the NYCERS. Pick an institutional allocator and the odds are they are in the Vista funds somewhere.

For NYCERS, $105MM contributed is now worth $204MM and meaningfully outperforming its “PME” (public market equivalent) return of 12.7%. See, beating the S&P 500 be easy if you’ve got the tools of private equity:

Except that’s absurd. This is LEVERED software investing. The public market equivalent is NOT (as the NYCERS suggest) the Russell 3000. A far more relevant benchmark is the R3000 Software and Services index which returned 16.0% UNLEVERED over the same period. Given the leverage currently on Finastra, it would suggest that Vista levered their equity roughly 3:1. Unfortunately, I can’t know because “terms were not disclosed.” With low interest rates over the period, that would suggest the appropriate hurdle was nearly 50%! And yet, as the above table makes clear, NYCERS and other institutional investors continually stepped up to add more money to Vista’s coffers over the last decade.