xAIr Supply

A mixture of hype and growing equity supply threatens the simple story of passive

What a wonderful way to ruin a perfectly good week… While I was in the midst of an interview with The Information, the tech-focused ‘zine, on the subject of index modification to facilitate the inclusion of SpaceX ($SPCX), I noted that, “I can understand why Nasdaq may have modified the index, after all, they have a listings business to consider, but I cannot for the life of me figure out why S&P would have put the reputation of the S&P500 at risk.” The reporter replied, “The headline just came across that S&P is NOT going to modify their criteria.”

Mudville rejoiced:

It was much worse over in the land of “What’s Next,” led by our friend, fElon:

The AI bubble is not simply a valuation story. It is a financing story. The market has treated AI as a demand shock for a handful of capital-light monopolies. But AI is turning those same firms into capital-intensive infrastructure companies. The passive bid absorbed buybacks. It may now be asked to absorb issuance.

Perhaps this is the start of the turn in the localized mania of AI breaking. While much of the behavior remains “passive at work,” we’ve seen a growing role from the actual flows into AI stocks as retail increasingly decides it has “figured it out” — it’s all about AI:

I wish it were that simple. We’re increasingly seeing behaviors that suggest more sophisticated parties are now playing along — with leverage. For example, look at the behavior between NVDA and its 2x levered ETF variant. The shares outstanding for NVDU, the Direxion 2x levered NVDA ETF (one of a surging number of levered single-stock ETFs classified as “active”), have begun tracking inversely to NVDA share price, a notable change from 2023-2024:

Typically, when we see this pattern, it’s a sign that the volatility harvesters are in play. Buying NVDU while selling NVDA call options is a fairly efficient call overwriting strategy. The emergence of derivative-income ETFs (like NVDY or similar capped-upside, high-yield products) plays a massive role in changing the plumbing of single-stock levered ETFs:

These yield-harvesting funds often use a mix of options and levered underlying instruments to generate high monthly distributions.

Because they harvest premium by selling upside call options, they cap their gains on the way up but absorb downside beta. When the underlying stock rips through the strike prices, these funds are forced to dynamically manage their collateral and delta-hedging exposures—often resulting in trimming underlying levered long exposure (NVDU redemptions) during massive rallies to lock in premium or cover assignments.

This suggests the characteristics of NVDA’s shareholder base are starting to shift. Rather than a performance-chasing retail play, it has matured into an institutional tool with many holders trapped by a highly-appreciated stock they are unwilling to take taxable profits on. When a single stock becomes a systemic macroeconomic proxy, professional desks use the 2x vehicle as a highly efficient, capital-insulated tool to trade mean reversion, harvest high variance, or hedge complex options books without tying up massive amounts of prime brokerage margin.

In other words, it’s no longer about love for NVDA — it’s just become another stock. That alone SHOULD be a warning sign.

But there were others this week:

I’m increasingly convinced that the AI universe has deeply misunderstood its product offering. While many, myself included, are loving the access to productivity-enhancing tools, AI has been embraced by users in an unprecedented manner:

There are a number of key points in the above graphic, but let’s focus on the “2:1 Personal use exceeds work use.” My growing conviction is that AI is being perceived by personal users as “Subsidized access to ‘help’ in answering the many questions that would have previously been unavailable to me in an economic manner, delivered in a non-judgemental and non-invasive manner.” Consider:

This appears unsurprising to me. The most popular columns in newspapers for decades were the “personal advice” columns. In internet parlance, “AITA” (Am I the asshole?) is a common theme. The market for professional-level advice seems unlimited at $0 to $20/month. There’s only one problem:

Those who lived through the original online retail bubble may remember this model. Yes, there is tremendous demand for Ben & Jerry’s ice cream delivered by Kosmo.com at subsidized prices below those of local retail stores. It is not a good business model. So AI companies have turned to marketing themselves to businesses as “labor replacement.” It’s not going so well:

Why? Because it’s a very deep misunderstanding of economics. AI companies are marketing AI as “labor replacement” and appear captured by the narrative that we can move to a “post-capitalist” society where all the “work” is done by machines. In economics, labor has a unique signature — a backward-bending labor supply curve:

This, in turn, plays a critical role in forming models for utility and innovation. Since humans exist in non-ergodic space, i.e., they have only one life to live, as incomes rise, the demand for leisure increases. This, in turn, spurs innovation in time-saving goods and services to replace previously labor-intensive tasks. In other words, technology exists to AUGMENT human labor. TASKS can be replaced by machines, but the core of economics remains the system of human wants, and humans cannot be replaced.

The AI industry has mistaken usage for a business model and task completion for labor replacement. What consumers have discovered is extraordinary: subsidized access to nonjudgmental, always-available help in answering questions, organizing choices, drafting language, interpreting conflict, and reducing the cognitive burden of daily life. It may be one of the largest reservoirs of latent demand ever revealed. But it is not the same thing as enterprise labor displacement. The former is advice-column economics at a planetary scale. The latter requires workflow integration, accountability, liability transfer, trust, and measurable P&L impact. The industry is trying to monetize the first by promising the second.

And subsidized access to help is not, by itself, a capitalist victory. It is a revelation of demand. The business demand for AI will emerge, but it will require business-process reinvention, not merely sprinkling models over existing workflows. The early enterprise buildout resembles the pre-factory stage of industrialization: semi-skilled human labor was gathered into larger rooms and organized more tightly, but the production process itself had not yet been fundamentally redesigned around the machine. Much of today’s enterprise AI effort is similar. It asks: “How can we do the same thing with fewer people, faster?” That is not nothing. But it is rarely transformational. The real value arrives only when the workflow is rebuilt around the new capability.

With the introduction of the assembly line, a factory was not simply a workshop with more workers inside it. It was a new production architecture: power, sequencing, specialization, supervision, inventory, distribution, and capital intensity reorganized around machines. Likewise, AI will not create durable enterprise value merely by letting existing employees draft emails faster or summarize meetings more cheaply. The value comes when firms redesign the unit of work itself.

I’m fortunate that my work puts me in contact with younger, thoughtful individuals who have enough domain-specific knowledge in their industry to start this process. They are having tremendous success. In my own work, AI tools have transformed my ability to rapidly build agent-based models to simulate the behavior of individual stocks in an index, enhancing my insights on passive investing more in the last nine months than in the prior nine years. But it could not have been done without the knowledge accumulated over those prior nine years (and the ~25 years of work in financial markets that preceded those).

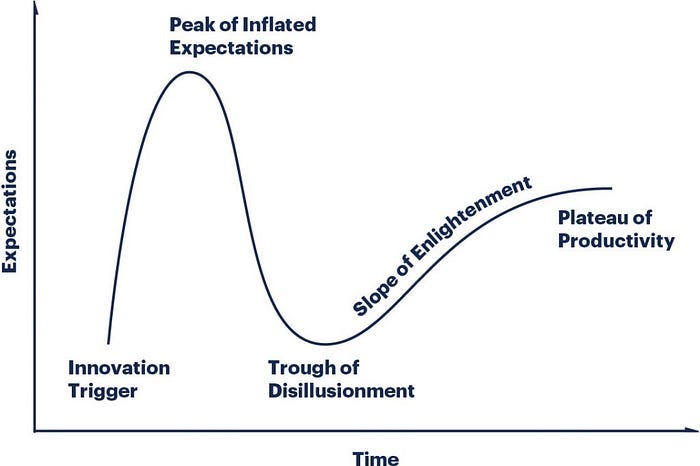

As a result, I am convinced we are cresting the peak of inflated expectations and shifting to the trough of disillusionment:

The question is no longer whether AI is useful. It is. The question is who funds the enormous gap between subsidized consumer usefulness, slow enterprise reinvention, and the capital intensity required to build the infrastructure. Increasingly, the answer appears to be: “public equity investors.” And this is occurring just as the (Air) Supply is shifting. It’s no longer just about new IPOs: