What Really Happened in 1971...

Thoughts on narratives and deglobalization

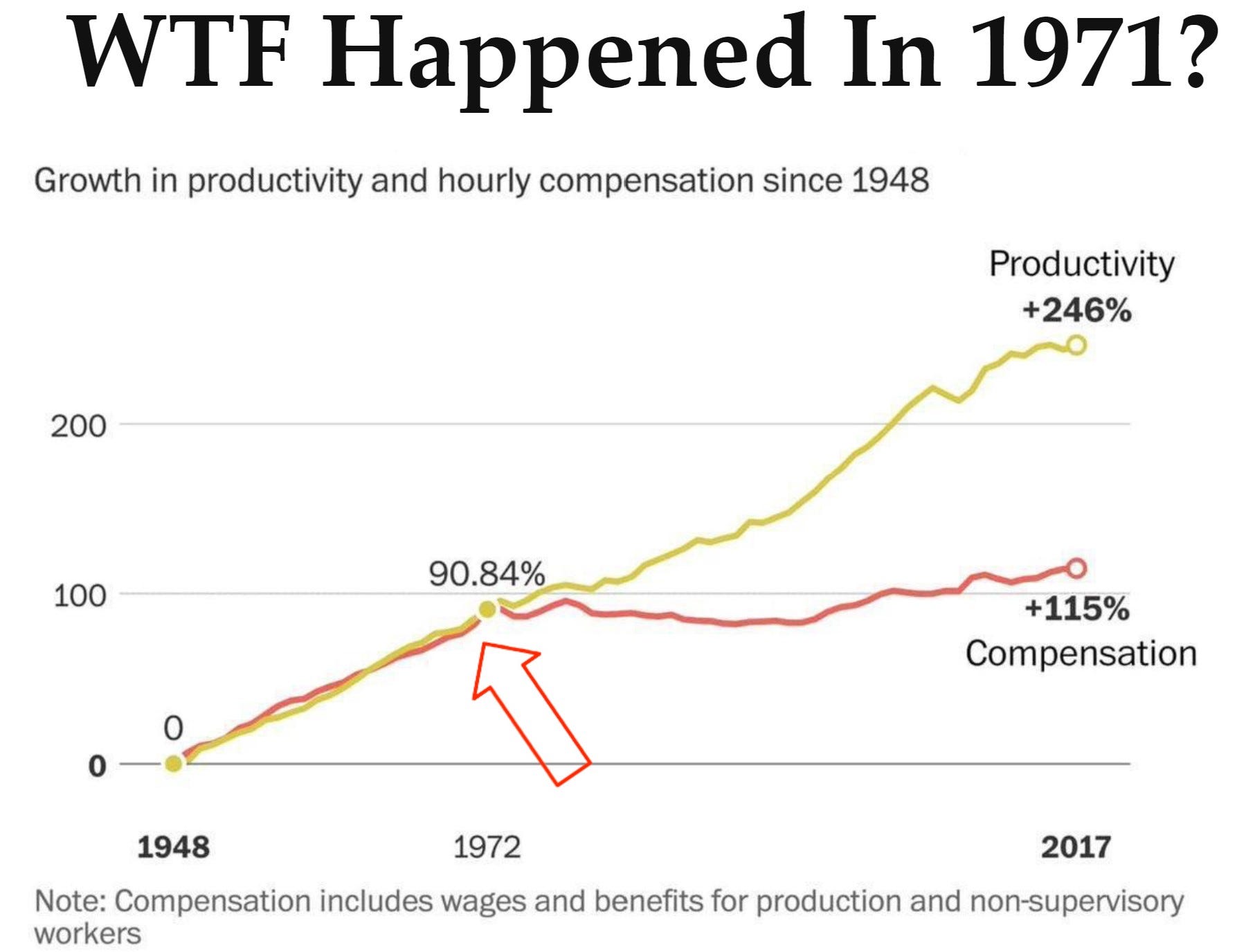

The internet is replete with memes about the collapse in purchasing power of the US dollar. One of the most common is the theme “WTF Happened in 1971”, complete with its website wtfhappenedin1971.com, which hypothesizes that decoupling the US dollar from gold drove a substantive change in the direction of income and wealth inequality. Unsurprisingly, I believe this false narrative confuses cause and effect. A typical chart from wtfhappenedin1971.com shows something along these lines:

It’s almost impossible to ignore the implications — “it all began to go wrong for the American worker when the US left the gold standard.” But this is a false narrative. First, the astute reader will note that the break in the index occurs MUCH earlier — in the 1960s:

A rolling linear regression can be utilized to estimate how much compensation rose for each 1% increase in labor productivity. Note that by 1971, compensation was rising only 60% of the rate of productivity gains, and that fell to 20% by 1981 before recovering through 1994… only to begin falling yet again:

Now this is a very different picture. It suggests that rather than something change in 1971, substantive trade breaks occurred in 1948 (not shown), 1983, and 1994. What could have changed? Trade rules!

In 1983, the US Congress approved the Reciprocal Trade and Investment Act, which President Reagan dutifully signed. This agreement was designed to address the increasingly “unfair” trade dynamics in the post-WW2 era that disadvantaged US workers by ensuring reciprocal access to foreign markets that wanted to sell into the US market. It worked. US workers gained a higher fraction of the incremental productivity gain for the next decade. And then NAFTA and China changed it for the worse in 1994, as so presciently predicted by Sir James Goldsmith in 1994.

Now importantly, this pattern also holds clues for the driver of inflation in the post-Covid era as labor compensation exploded relative to productivity — driven by a collapse in output relative to compensation and fiscal support for workers not working (raising the reservation wage). Over the last three years, on average, workers have captured more than 100% of any productivity gains:

And suddenly, it becomes clear why the Federal Reserve is targeting an increase in unemployment — corporate profit increases are “fine,” but wage gains greater than productivity are not.

ALL ANIMALS ARE EQUAL

BUT SOME ANIMALS ARE MORE EQUAL THAN OTHERS — Animal Farm

And yet, we are told the narrative is that Powell must break the Fed Put. Unless he does so, private equity will not properly suffer. Somebody tell Steve Schwartzman…. please:

Rather than destroy private equity, it appears that Powell has created yet another money-making opportunity:

A reminder — I do not believe in conspiracies. Powell likely means what he says privately and genuinely fancies himself a patriot. But if the tools are not fit for purpose, and interest rate hikes are not the right tool for reining in private equity as is becoming increasingly clear, then again, we return to my paraphrase of Hanlon’s Razor:

“Never assume conspiracy when incompetence will suffice.”

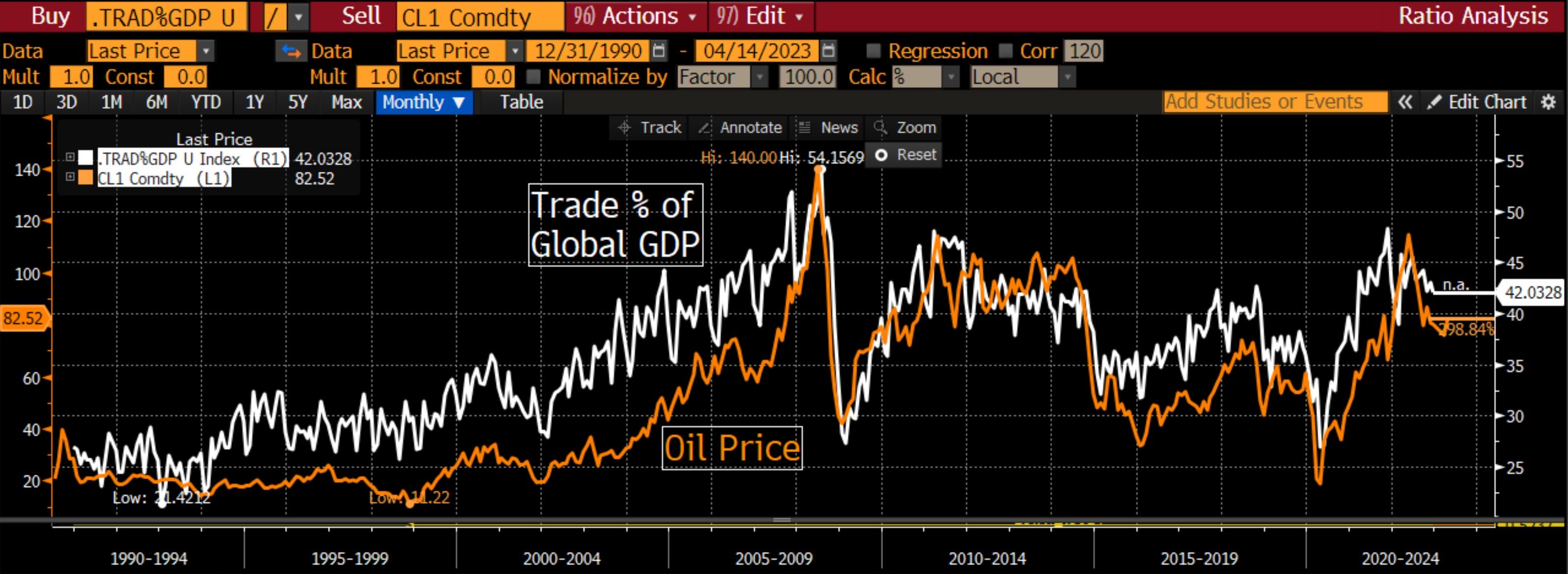

Theories of deglobalization do not hold water. Trade as a percent of GDP is far closer to a peak than a trough. There are few signs that this will retreat anytime soon as manufacturers like Apple focus on moving production to India rather than reshoring. When manufacturing returns to the US, it will likely be part of a wave of automation and additive manufacturing that skips labor in the same manner that agriculture no longer involves meaningful labor content.

Meanwhile, while the wealthiest Americans rush to buy US treasury bills offering 5%, and private equity utilizes their locked-up capital to buy back depreciated debt, we’re cutting food benefits to women and children with predictable effect:

Suppose you want to stop the consolidation of the US economy under the increasingly financialized framework we’ve seen over the past forty years. In that case, the answer is to enforce existing rules around antitrust. The fact that this may not be possible with the regulatory and political capture under current leadership is not an excuse for an unelected bureaucrat (Powell) to take matters into his own hands. If you are against an interventionist Fed when they cut rates, then you should be against an interventionist Fed when they hike rates — regardless of the reasons. And the answer is not to hand these decisions to an “independent Fed” if Congress cannot correctly manage its priorities. What is worse is that the Fed will fail because its tools are not fit for purpose, and in the process of failing, it will lose its independence.

Then we’re really in the soup. And Powell is the unwitting chef.

It had been felt that the existence of a farm owned and operated by representative democracy was somehow abnormal and was liable to have an unsettling effect in the neighborhood. Too many aristocrats had assumed, without due enquiry, that on such a farm a spirit of licence and indiscipline would prevail. They had been nervous about the effects upon their own subjects or their bureaucratic ranks. But all such doubts were now dispelled. Today he and his friends had visited the United States and inspected every inch of it with their own eyes, and what did they find? Not only the most up-to-date methods, but a discipline and an orderliness which should be an example to all farmers everywhere. He believed that he was right in saying that the labor class in the United States did more work and received fewer benefits than any others in the world. Indeed, he and his fellow visitors today had observed many features which they intended to introduce on their own farms immediately.

With apologies to George Orwell.

Comments appreciated.

For those of us who made our money advising people how to legally cheat on their income and employment taxes, the events in U.S. financial history can all be explained by how the U.S. Treasury collected the money that it did not borrow. For us tax plumbers the changes in net incomes can all be explained by the valves and leaks. The declines and stagnations in the wages earned by "ordinary" Americans that Mr. Greene notes can be tracked against the final end of tariffs. WW 2 and the period of worldwide reconstruction that ended in the late 1950s and early 1960s saw the decline of tariffs as a significant source of revenue to the Treasury; but the U.S. position as literally the last industrial nation left standing allowed American wages and labor demand to be protected from international competition as if late 19th century import taxes were still in place.

As a tax plumber I continue to find bitter amusement in the fact that "free" trade was first advocated by Southern planters because they objected to the head taxes imposed on the last decade of legal importation of slaves. It also makes me smile wryly to know that the income tax was first promoted as a substitute for evil tariffs; better to tax what people earned than to allow them to profit from "inefficient" taxes on imports that raised laborers' share of the national income.

We will know that the labor movement has revived when someone gains national popularity by advocating that (1) Social Security and Medicare coverage be unified at the lower age of 62, (2) employment tax rates be lowered, and (3) that lower rate be applied to all earned income regardless of its characterization.

Thank again to professor plum for allowing me to share this and other rants.

"if Congress cannot correctly manage its priorities." The focus on the Fed by the financial media is 99% mis-placed. Congress has 1000x more control over jobs and inflation. Writing about the Fed is nearly akin to the 1971 gold bug article. The Fed doesn't do anti-trust, make covid rules, send stimulus checks, deal with trade, etc, etc, etc. Why no one ever writes about Congress' "mandate" is beyond me. The Fed keeps banks afloat and greased, and controls the short end only. And yet all you hear is about their impact on jobs, stocks, etc. Total nonsense by ALL of you in financial media