Turning the Page

Chapter Too

Top Comment

Famous chef and TV personality, Dalton Brown, shares a recipe:

On Trade: I am excited by the tariffs as Trump seems to be taking the winning posture in the game of Iterated Chicken taking place over them. Similar to how one could've predicted a Trump-like figure in US politics due to one side intentionally ceding the games of Chicken taking place over domestic policy (Nick Land's 2013 essay "Chicken" actually does this in response to the debt-ceiling showdown occurring at the time), his statements acknowledging the potential pain and willingness to overlook it is also the way to signal you're above being reasoned with which is how you win Chicken. You'll notice that the Canadian response has been to claim betrayal and not point to the "rigorous academic literature demanding uncritically subordinating one's national economy to Free Trade".

On the Book: I look forward to simply linking to it as an example of what I refer to when discussing the impact of passive investment vehicles instead of having to link 4 or 5 hour-long interviews.

MWG Response: Dalton, you’ve inspired me to look for recipes for “Iterated Chicken.” For those less culinary-inclined, iterated chicken refers to repeated games of chicken, a variant of Prisoner’s Dilemma games. As Dalton notes, a technical summary of game play and strategies can be found all over the internet, but here’s a reasonable link that introduces “the trembling hand” aspect of chicken — when intentions do not match actions.

Or you can rewatch Footloose to reinforce that YIGAF is indeed within the Six Degrees of Kevin Bacon universe:

Trump’s strategy on tariffs is indeed a game of chicken, but it is an unbalanced game. Imagine a game of Prisoner’s Dilemma where one of the prisoner’s “cares” much more than the other. I had ChatGPT create an illustration:

Unbalanced (Asymmetric) Version of The Prisoner’s Dilemma

To illustrate a situation where one side has a lot more to lose (e.g., a smaller trading partner facing the U.S. in a tariff standoff), we can give each player their own values with different magnitudes—yet still preserve the Prisoner’s Dilemma logic for each player individually.

Here’s an example matrix:

The first payoff in each pair belongs to Player A; the second belongs to Player B.

Each player still faces the same dilemma:

Defecting (imposing tariffs, betraying, etc.) offers a “temptation” payoff if the other side cooperates.

Both prefer mutual cooperation over mutual defection overall, but defecting is individually tempting.

Player A(United States)’s payoffs are relatively small:

A “swings” only from 0 to 3 depending on outcomes—less to gain or lose.

Player B(Canada or Mexico)’s payoffs are larger:

B’s payoffs swing from 0 to 20—much more to lose if things go badly (or to gain if it can defect successfully).

Despite these differing magnitudes:

Each player individually still sees defecting as the rational choice (the “temptation to defect” is highest, the “sucker’s payoff” is worst), which is what keeps it a Prisoner’s Dilemma.

The mutual-defection outcome is worse collectively than mutual cooperation. Yet, fear of being the “sucker” (0 payoff) can drive both to defect.

Linking to Tariff “Chicken”

When the U.S. threatens tariffs on a trading partner with a much smaller economy, it mirrors this unbalanced payoff structure:

U.S. (Player A): Gains or losses from a tariff war are meaningful, but the absolute impact may be relatively modest in percentage terms of GDP (hence smaller swings in payoff).

Smaller Country (Player B): Has a lot more at stake. If a trade war escalates (both defect), the smaller partner may suffer proportionally bigger losses, creating a strong incentive to cooperate or concede.

This dynamic can push the more vulnerable side to concede faster—knowing they have far more to lose if negotiations fail—making it effectively a “game of chicken” layered atop a Prisoner’s Dilemma.

The risk for the United States is not the potential losses — under almost all conditions, the weaker party will concede. The risk is of the trembling hand — what if conditions occur (like a stuck shoelace) that prevent the other side from conceding even though it is rational? Hence the embrace of the “Crazy Man” persona — if you know in advance that your opponent is “nuts” with a high propensity for stuck shoelaces AND you have far more to lose from an unsuccessful negotiation round, you are far less likely to even let the game get to the point that the tractors are in motion. So far, Trump has not had to fire up the tractor, but the tougher rounds are ahead.

And on the book? I really hope you’re right, but given I can’t get Rick Ferri to even watch ONE video, I doubt the book will solve your challenge. But I’m going to try nonetheless!

As mentioned in last week’s note, there will be LESS of traditional YIGAF and more of the book over the next few weeks. ONLY paid subscribers will have access to the book chapters, which means you not only pay for the privilege of pre-reading and editing my work (thank you to those who caught the error in the value investor portfolio!), but you’ll ALSO pay for the privilege of buying the book. And people think I’M the dumbest man alive? Hahahahaha… cough.

While I want to jump right into Chapter 1 (conveniently released after Chapter 6), I had some fun this week answering a question posed by an institutional investor who noticed the Goldman Sachs commentary on “passive investing doesn’t drive markets.” Regular readers of YIGAF know that I believe GS is being intentionally disingenuous due to the growth of total return swap business with Vanguard, but I figured I’d share the example.

First, the below chart highlights the relative performance of a Morgan Stanley index of “passive long” vs “passive short.” These indices are constructed using a methodology similar to GS by simply looking at “who owns” and labeling them “passive” or “active”:

The “Passively Held Short” index is composed of stocks with theoretically the LEAST passive influence due to ownership. In this case, the largest stock is AppLovin Corp, not to be confused with McLovin.

Looking at the holders of McLovin, sorry AppLovin, we quickly understand why this qualifies as “Passive Short” — while most stocks would show Vanguard and Blackrock as clearly #1 and #2 with ownership in the range of 10-12% EACH, Applovin has roughly half this representation. In addition, “Angel Pride Holdings” is a large investor. Who ‘dis?

Ahh… a single asset entity…

Owned by insiders…

That failed to properly file holdings reports for Q3, giving the impression that they sold nearly 17MM shares only to repurchase them a quarter later… which of course is wrong:

Regardless… we get it… this stock is less impacted by passive than other stocks… right? In case you can’t read the chart below to identify the news event that drove APP to double in a week, I’ll type it out:

“Applovin Corporation to Join Nasdaq 100”

Yeah… “Passive Short” indeed.

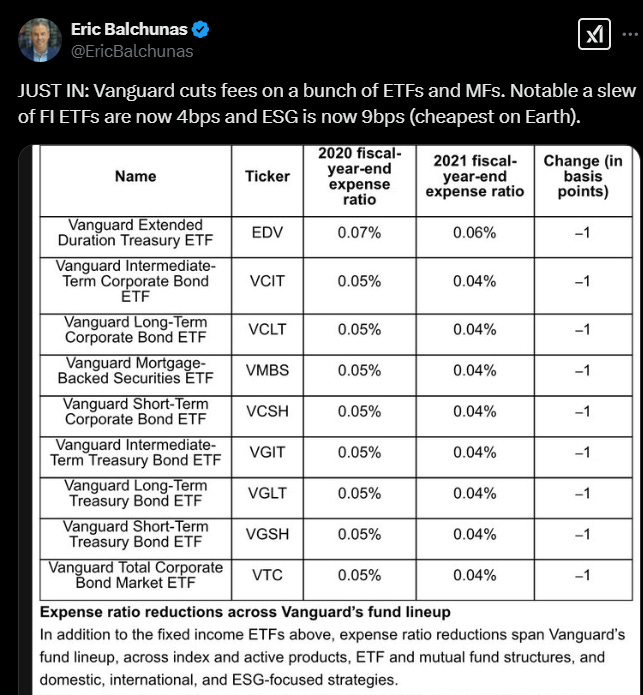

We also got “fundamental support” for the growth of passive with “the biggest Vanguard fee cut ever!” news as Vanguard slashed fees on many funds by an amazing 20%:

Wait.. 1 bps? What is this, a fee cut for ants? The simple reality is that the fund expense game is over (and perversely swinging the other way as funds add leverage to arbitrage the high margin fees as discussed in prior posts). Cutting from 5bps to 4bps has no impact on performance. When “passive” funds were introduced, most charged 75bps in a world of 200bps active managers. Bogle won that battle, but we continue to pretend it’s the driver of the story of passive outperformance. It is not.

And with that… let’s move to the real story! As always, comments and questions are strongly encouraged.

CHAPTER 1

The Need for Retirement Security and the Rise of Pooled Capital