Nobody gets fired for buying IBM

But maybe IBM wants some people to quit IBM...

While I Have Your Attention:

Dear YIGAFers… I am immortal.

Not really, but a small piece of me has become so via ChatGPT. The innovation that is occurring in ChatGPT/AI is truly incredible. While not the focus of this piece, I wanted to highlight the latest iteration of ChatGPT, which, exactly as anticipated, has become personalized.

“My hypothesis is that because the bias in ChatGPT we want to see is ours. In other words, this technology is destined for hyper-personalization — ChatGPT needs to evolve in a manner similar to the “echo chambers” we cultivate in other social media platforms so that we can “trust” it.” — YIGAF, “Chat Amongst Yourselves” (Feb 5, 2023)

Less than a year later, ChatGPT has been loaded with all of my writings to become, or at least for me, the man behind the curtain — ProfPlumv1! And I trust him completely (/s):

I’ll be experimenting with ways to use this tool and would welcome thoughts from the crowd.

Back to Regularly Scheduled Programming…

A reminder that all institutional subscribers should have received a replay and copy of materials presented during last Tuesday’s Institutional Call. If you have not, please let me know.

What I’m Reading Now

I had the privilege of joining the Collaborative WIM annual conference to discuss a range of issues for Women in Investment Management. This was much less about the “easy” job of asset management than the very hard job of living a life well. Immediately after me, Oliver Burkman spoke. As I’m often reminded by my participation in these types of events, I should sit down, STFU, and listen to somebody else talk more frequently. I immediately went out and purchased his book, “4000 weeks: Time Management for Mortals.” I encourage you to do the same. We’ve all got roughly 4,000 weeks in this journey (~52 x 40), and I highly doubt that will change meaningfully over the remaining 1,500 I have at my disposal. How you choose to spend those weeks is up to you and you owe no one else an explanation. This is not a book that tells you how to more efficiently use the 168 hours in a week. It simply asks you to ask, “Why?"

Top Comment

Doug asks:

Thanks for another thought provoking article MG. After watching a recent interview with Andy Constan, I have a few questions for you as it appears you both are in some disagreement as to what may transpire in the near term.

How do you weigh the recent lower-than-expected Treasury long-end issuance against your view of a recessionary trend? Could the easing financial conditions mentioned by Andy Constan in the short term alter your long-term outlook on corporate profits? In light of Andy's bullish stance based on fiscal policy, do you see any fiscal measures that could sustain current corporate profit levels? Do you believe investor sentiment could continue to drive a risk-on rally, despite the fundamental economic concerns you've raised? Considering the potential for short-term market rallies, how might investors balance the apparent reinvestment risk in treasuries and CDs?

MWG:

Doug, would appreciate the link as I can’t entirely know Andy’s arguments without hearing the case. I would guess you’re referring to his argument that the expected increase in fiscal spending paid for with a higher fraction of bills (or more accurately a lower fraction of coupons) is bullish for risk assets as articulated in this Blockworks video. There’s certainly merit to this argument. When spending is financed with bills, it’s very close to simply giving money away; when spending is financed with bond (coupon) issuance, the cash that is tied up in bonds is now a risk asset and reduces overall risk-taking capacity. I don’t disagree with his argument there.

Where I am more bearish than Andy is the composition of risk in the economy. I can give money to people who already have money (eg increase interest expense) and it has very little stimulative effect on Main St as the propensity to spend is relatively low. Meanwhile, I’m restricting credit to those with a low propensity to save/high propensity to spend. Perversely, this can be positive for risk assets as the increased savings (transfer from public sector to private sector) need to find a home even as the economy weakens. This is magnified by the above dynamics.

So eight days after that interview, I can’t help but emphasize that the MAJORITY of stocks have given back almost all of their gains. The equal-weight R2000 and R1000 are down sharply. An argument that treats these types of events as fundamental, rather than purely risk-taking capacity, does not explain this behavior. I’d also note that Andy’s statement that “no one fires people with their stocks at all-time highs” doesn’t match the same data. On a market cap weighted basis, the “average” stock is down 13.5% from 52-week highs; if I do the same calculation on an EMPLOYMENT-wtd basis, the average stock is down 18.5%. The 52-week highs story is simply not accurate.

The Main Event

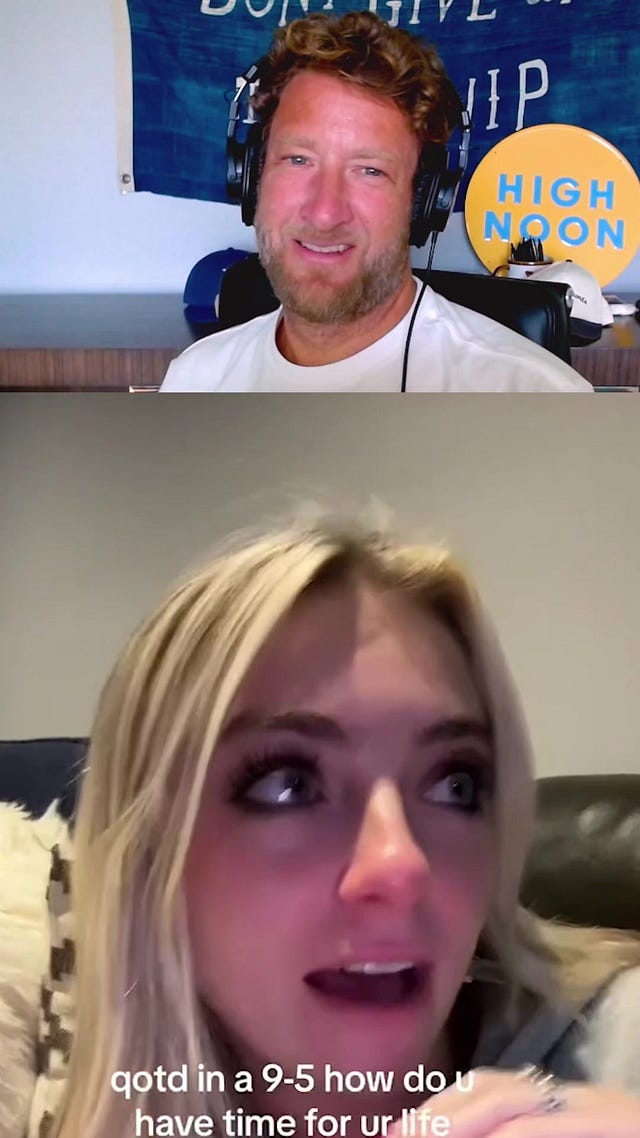

As I watch my (increasingly) adult children navigate this world, I question the “obvious” choices available to my generation and wonder if there isn’t a better world available to them. The recent viral TikTok of “9-5er girl” has been polarizing. A sizeable fraction of my Gen X peers have taken the perspective that, “Hey, that’s life cupcake…”

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

It doesn’t have to be. The resources are increasingly there to consider the same type of fundamental rethink of society that occurred in the late 19th century as governments and businesses attempted to persuade individuals to give up the food security of the farm for the permanent INSECURITY of urban employment. As the demand for employees in urban factory environments (or ex-urban mining) exploded, the competition for workers, particularly skilled/literate workers who could manage the increasingly large teams, exploded. This originated the social insurance schemes we take for granted (or bemoan). And this week, we saw a potentially momentous change in the direction of these plans:

It’s worth briefly reviewing the history of retirement schemes in order to put this in context. The first corporate pension plans emerged in the United States in the late 19th and early 20th centuries. One of the earliest recorded corporate pension plans was established by the American Express Company in 1875. This was a significant development in the history of retirement benefits, as it marked the beginning of companies providing structured retirement benefits to their employees, a practice that would evolve and expand considerably over the following decades. The concept of corporate pension plans grew in popularity, particularly in the early 20th century, as more companies began to recognize the value of providing retirement security to their workers.

The American Express Company's first corporate pension plan, among the oldest in American history, established in 1875, had several notable characteristics:

Eligibility: It was available to employees who were 60 years or older and had been with the company for at least 20 years.

Pension Amount: The plan provided for a pension that was half of the employee's average salary during the last ten years of employment, but not exceeding a maximum of $500 per year.

Disability Provision: The plan also included a provision for employees who were unable to work due to a disability, regardless of their age or length of service.

Funding: The pension was funded entirely by the company, without any contributions required from the employees.

This plan was groundbreaking at the time and laid the path for future corporate pension plans. It reflected a growing recognition of the importance of providing financial security for employees in their retirement years. It also wasn’t that meaningfully different from the Roman Republic's retirement schemes.

Upon completing their service, which typically lasted 20-25 years, legionaries were awarded a retirement package that could include a pension in the form of a lump sum of money (known as the "aerarium militare" and/or a grant of land. This land was often in conquered territories, both rewarding the soldiers and promoting Romanization and security in these regions. This system provided security for retired soldiers and acted as an incentive for recruitment into the Roman military. The promise of a tangible reward upon completion of service was a significant motivator for many men to join and remain loyal to the Roman legions.

When American Express established its pension plan, it was among the elite institutions with more opportunities than employees. Attracting and retaining employees provided a competitive advantage for the fledgling titan. Historically, the introduction of new employee benefits has been the purview of these types of institutions; companies who are struggling rarely seek strategies to attract more employees. Think gourmet cafeterias and metal slides…

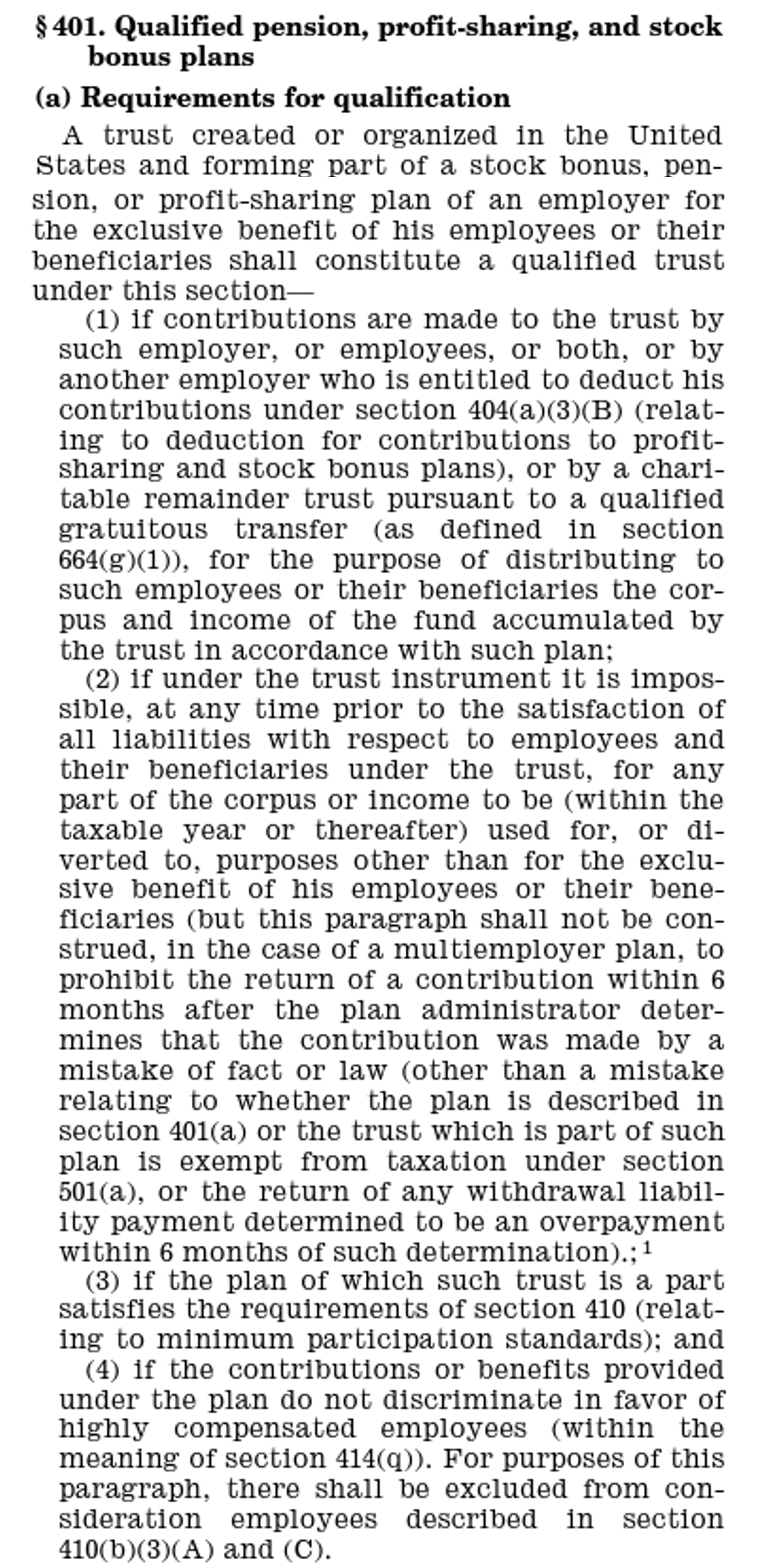

Technology companies have always been at the vanguard of corporate pension strategies — from Amex in 1875 to IBM in 1982. In 1982, IBM was among the first major employers to embrace the new innovation of 401Ks. 401Ks were the unintended consequence of a little-noticed executive compensation perk of the 1978 tax reform, Section 401k:

These plans became effective on Jan 1st, 1980. Unfortunately, Paul Volcker was in session, but that didn’t stop equity markets from rallying in the first month of 1980 (the classic “January Effect”) and once Volcker cut rates, equities exploded higher by 40% only to see them undone with Tall Paul’s second reach for the sky.

As noted, this was originally a perk for executives. However a far-seeing benefits consultant, Ted Benna, identified that these plans could replace traditional defined benefit plans. The rest was history. From a standing start, 401Ks grew to roughly $100MM in assets by August 1982. By 2021, they stood at $7.9T. Alongside IRAs (created in 1972 to facilitate defined benefit plan rollovers), they are likely the single most successful pension scheme in history. Unsurprisingly, companies embraced the idea of a defined contribution with no liability to ensure retirement OUTCOMES. As I have stated before, “Albert Einstein was wrong. Compound interest is not the most powerful force in the universe… liability avoidance is.” Today, Defined Benefit plans, particularly the historically common “percent of salary at retirement with COLA” is basically dead. Of the $3.7T in private sector defined benefit plans, approximately $1.3T is in “cash balance plans” which guarantee a modest return on a cash contribution, but offer no guarantee of outcomes relative to income. So apples:apples, Ted Benna’s creation has grown to over 3x the size of its predecessor.