An Unexpected Update

Given the chaotic messaging around Iran, a quick note

I was traveling this weekend and did not expect to find time to write; unfortunately, a delayed flight left me with the time to share a few thoughts. I was in Tampa for the meeting of the Philadelphia Society, an organization that was at the vanguard of the rebirth of the American conservative movement in the 1960s. I’ll discuss that visit, but more importantly, things are now moving quickly in the US-Iran conflict. Fortunately, largely in the direction I had proposed.

You have likely seen the confusing headlines:

Got it? Perfectly clear. To help you understand this complex topic, we bring you Samuel Jackson:

What?

“Iran” no longer exists as a unified political voice. The IRGC, the National Security Council, and the diplomatic class are arguing publicly:

“Following the unexpected tweet from the Foreign Minister about the liberation of the Strait of Hormuz, Iranian society has been plunged into an atmosphere of confusion.”

They also directly called out the “absolute silence” of the Supreme National Security Council and the negotiating team, demanding explanations so the “narrative of the enemy” doesn’t fill the vacuum. — Fars News Agency (IRGC outlet)

“Bad and Incomplete Tweet by Araghchi and Incorrect Ambiguity-Creation Regarding the Reopening of the Strait of Hormuz.”

“Publishing this tweet, without any verbal explanation or at least sufficient written explanations, constitutes a complete lack of tact in communication.” — Tasnim

Now some in the media are, of course, seizing on the confusion to highlight that Trump is once again deeply out to a Taco Bell salad lunch. And I want to emphasize that there can be two truths — Trump can be deeply disturbed AND Iran’s leadership has fractured as the US prevails in the conflict. We have precedent. After victories in Italy, Germany, AND Japan in WW2, internal conflict prevented consolidated messaging. After Hitler’s suicide and contested elevation of Karl Dönitz, pockets of German and Czech military refused to accept the surrender.

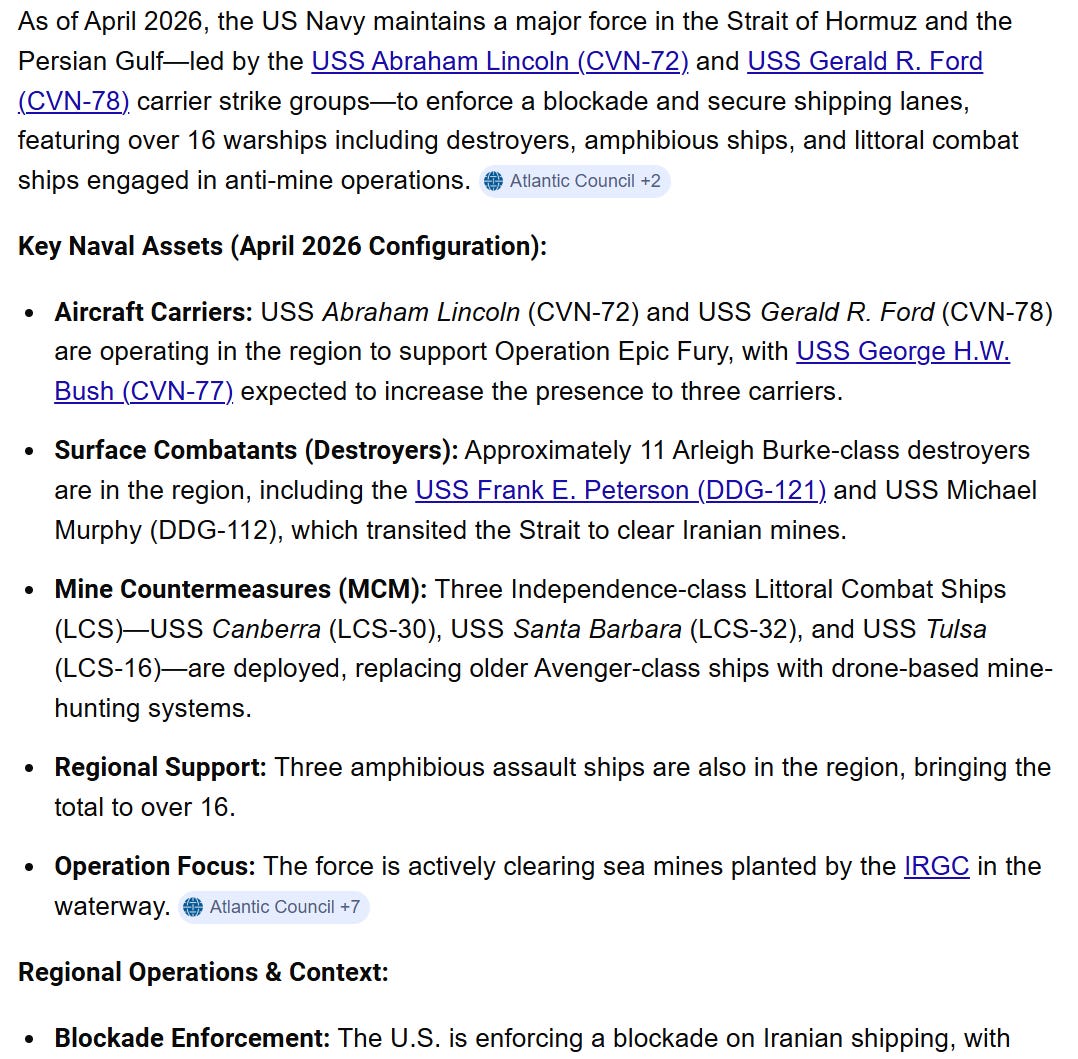

The US Navy is fully in control of the Hormuz. Those carriers hanging outside missile range are no longer threatened.

We’ve moved from Iran enforcing a blockade, to the US enforcing a blockade ON Iran. The terms to open the SoH from Iran? “Stop being so mean to us! It’s not fair you’re blocking the way!”

Feels pretty spot on with the outline from exactly a month ago:

This bifurcated dynamic is the foundation of the macro landscape. The Hormuz crude issue is an asymmetric warfare problem that U.S. air and naval superiority will resolve within weeks to months. Once escorts and minesweeping begin, signaling American control, it’s largely over. Marine deployments will likely limit incursion to control of coastal regions, leaving the Iranian people to resolve their remaining internal conflicts. Unlike Iraq, a shadow government embraced by the people is ready to go.

Now I know many readers will say, “You can’t know this!” And they’d be right. There is no “knowing” until it’s over. But it’s pretty much over. There was no 5-D chess. Just math.

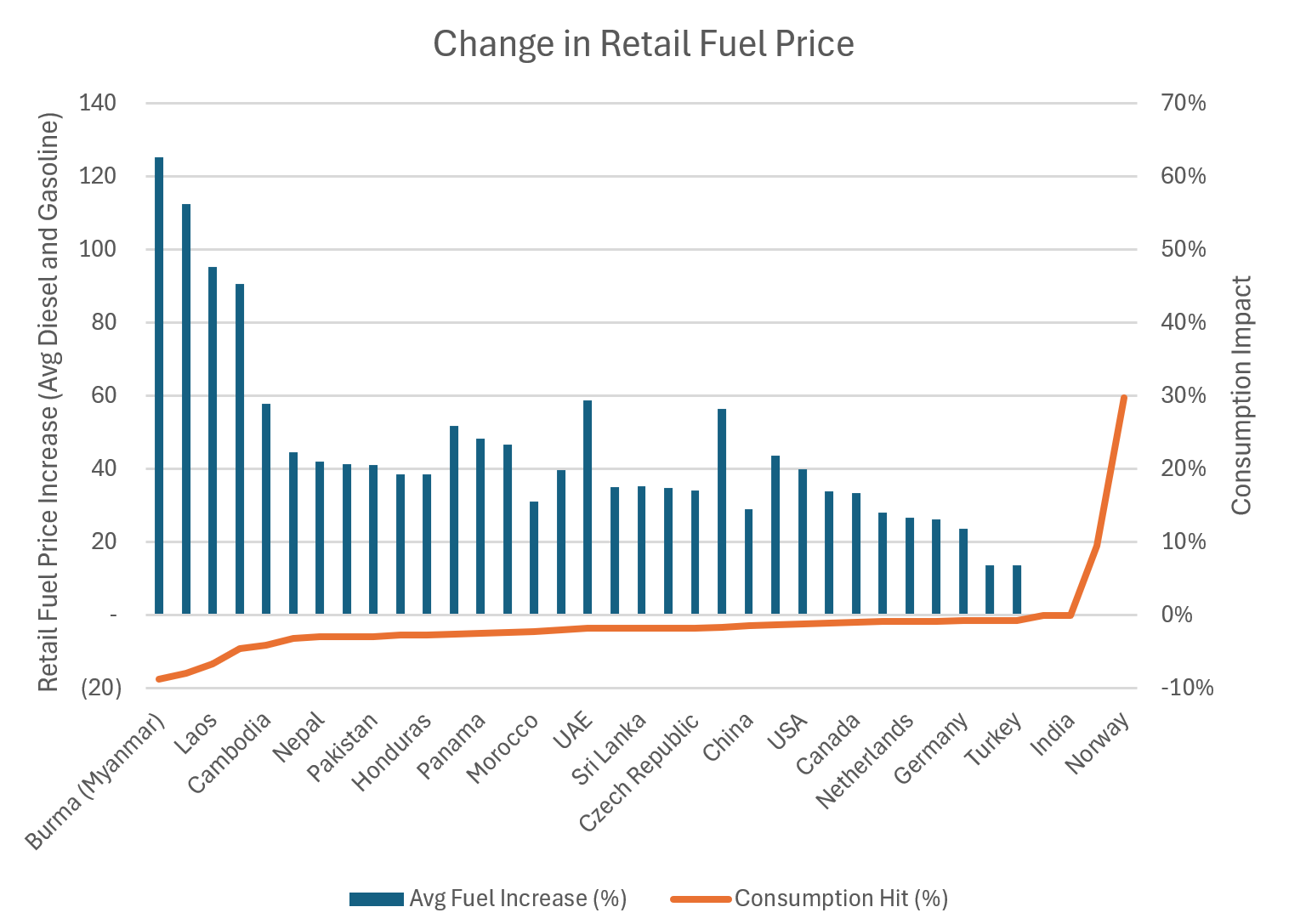

The oil story collapsed under its own weight on Friday. Sure, Trump was the catalyst. But the reality that many are recognizing now has been well publicized on these pages — much of the oil was already making it out and demand destruction, particularly in emerging markets has been significant:

By my calculations, roughly 2MMbd in demand has already been destroyed. Had prices maintained at these levels, within six months we were looking at 10-20MMbd. Some of that lost demand will return as prices fall and we restock strategic reserves, but some will be permanently lost. We don’t run HVAC twice as much after skipping for a day, nor do we make two trips to the store to make up for the one we skipped last week. Combined with modestly increased production and (as predicted) removal of restrictions on Russian exports, oil will be increasingly well supplied. Meanwhile, the disruption is likely to prove unhelpful to a fuel likely already at peak demand.

Equity markets have recovered, albeit narrowly (poor breadth). Again unsurprising — “macro” products (SPX) have dominated single stock. It’s “RISK” on, not “specific risk” on. With that said, though positioning remains muted overall as the flow has been dominated by retail inflows and short-covering, the PACE of inflows is among the fastest in history:

I am reminded of the language of 1968:

“And all through the stormy course of 1967 and 1968, when things had been coming apart and it had seemed that the center really couldn’t hold- the rising national economic crisis culminating in a day when the dollar was unredeemable in Paris, the Martin Luther King and Robert Kennedy Assassinations, the shame of the Chicago Democratic convention, the rising tempo of student riots– the silly market had gone its merry way, heedlessly soaring upward as if everything were O.K. or would surely come out O.K. as mindlessly, maniacally euphoric as a Japanese beetle in July. Or as a doomed man enjoying his last meal. One could only ask: Did Wall Street, for all its gutter shrewdness, have the slightest idea what was really going on?” — The Go-Go Years, John Brooks

As history can tell us, 1968 was not “the end.” But it WAS the beginning of the end. With the late 1960s, the IPOs slowed and the torrid pace of retail participation began to disappear despite markets making new all-time highs. By the early 1970s, corporate distress was beginning to restructure the American economy as “old economy” behemoths could no longer cover their mounting pension bills.

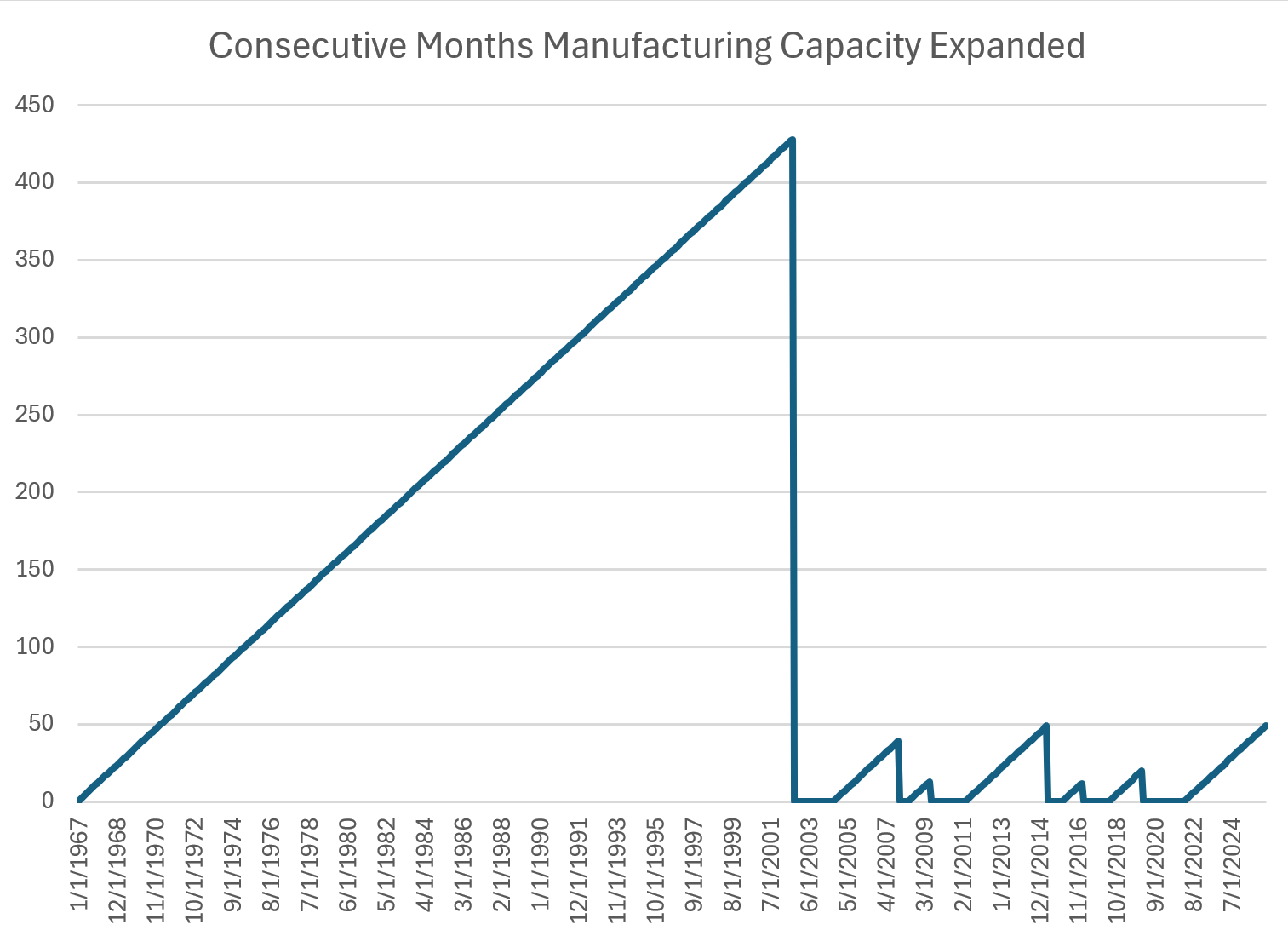

My hunch is that this will be similar. Not because inflation will return and the Fed will be forced to hike rates to 13%, as “accommodative” Arthur Burns did in 1974, but because the economy is slowing and restructuring. High-tech buildouts and tariffs are slowly leading to a recovery of domestic manufacturing capacity which has expanded for 48 consecutive months — a new post-2000 record:

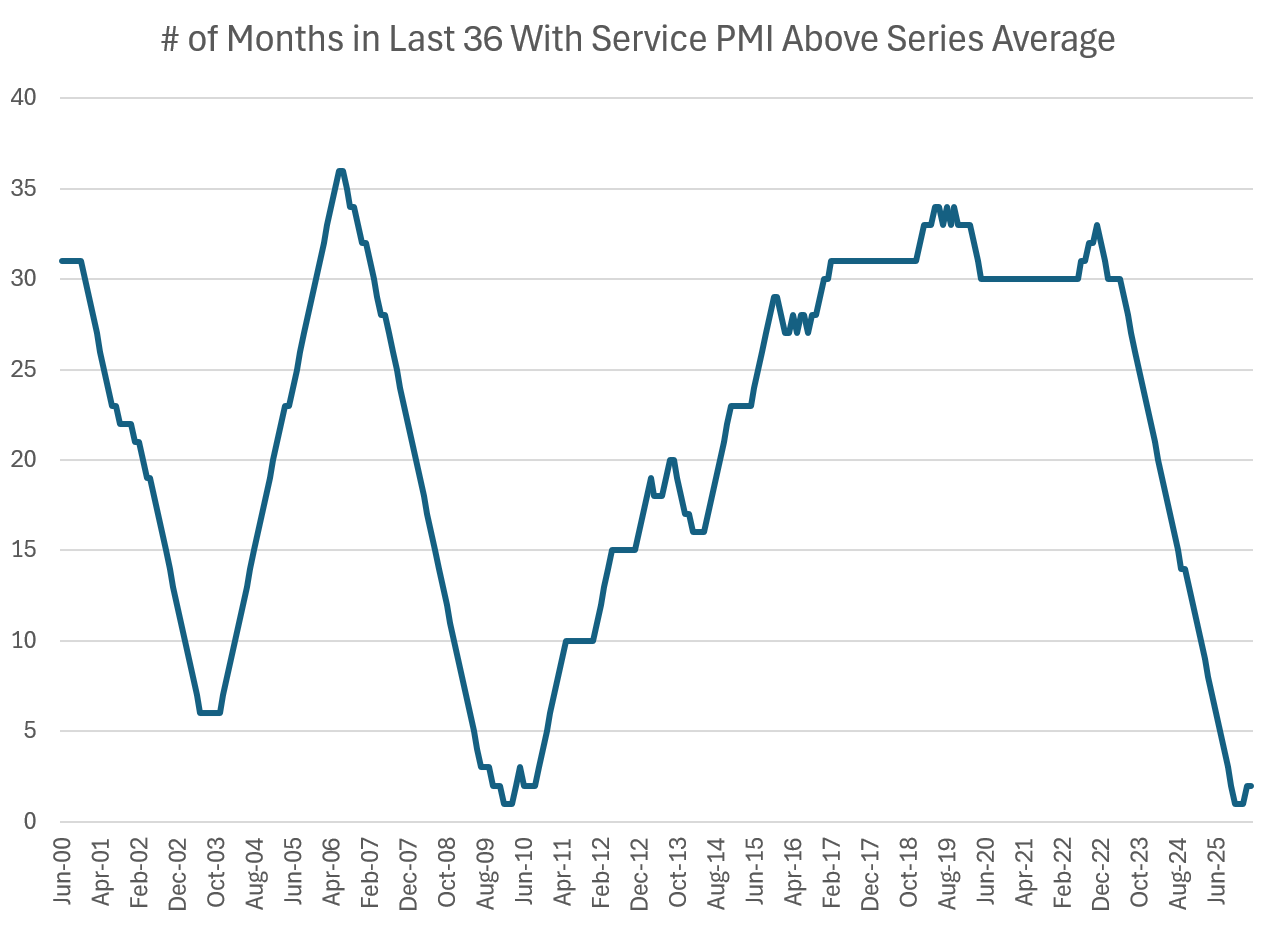

In contrast, Services PMI has been below the series average for the last three years. We are slowly healing from our 25 year manufacturing devastation, but that sector has shrunk to ~20% of the US economy and only 8% of employment. Meanwhile, as I hypothesized almost exactly three years ago, services is retreating (pre-ChatGPT btw):

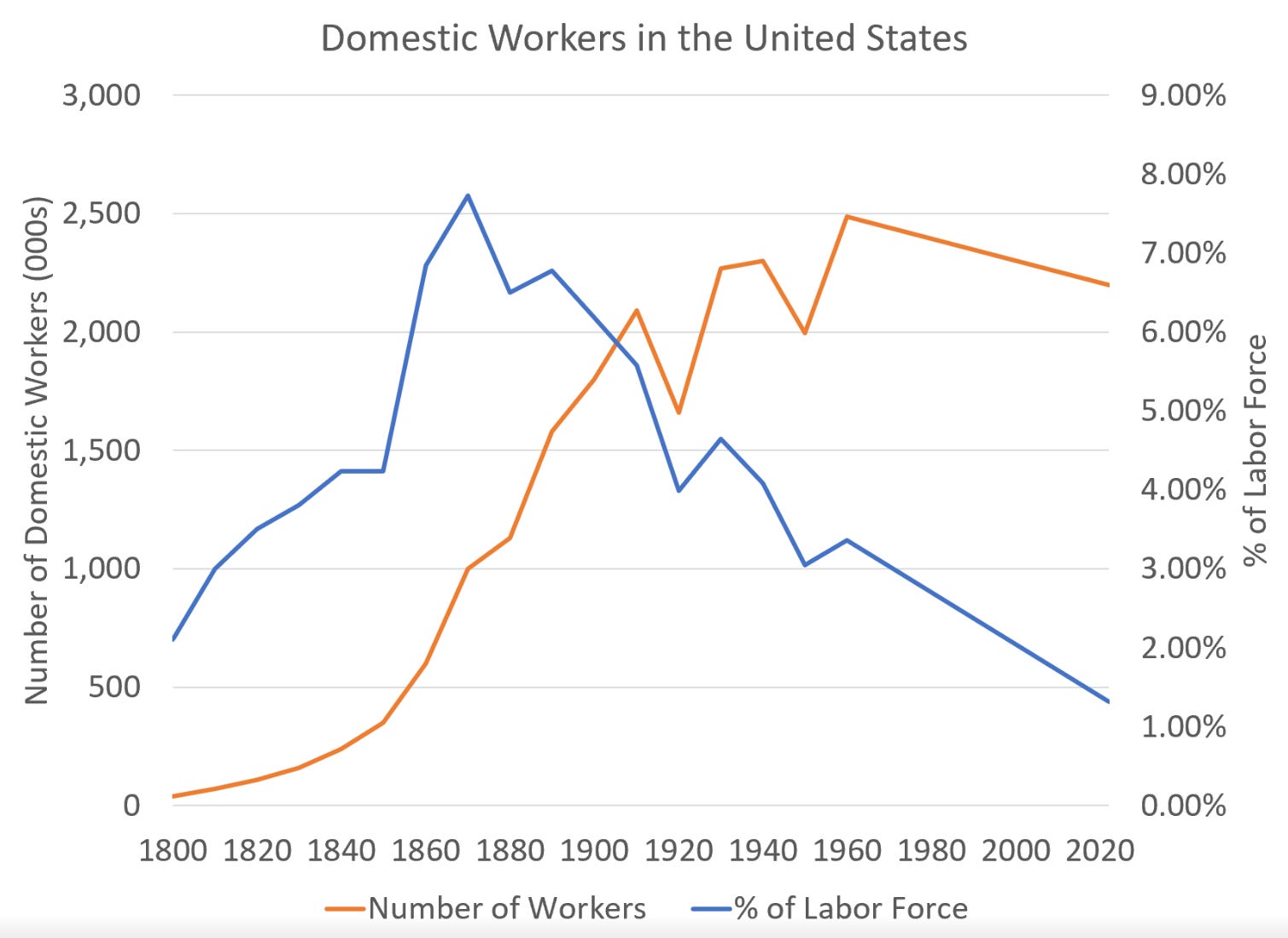

The US economy has undergone a significant shift towards a services-driven economy over the years. However, there has been a recent downshift in services consumption per capita growth, even before the pandemic. This downshift is similar to the decline observed from 1907 to the end of World War II. — Yigaf, May 2023

The late Industrial Revolution was really a revolution in services. Washer women became washing machines. Single-viewing theater performances became “movies.” Singers and orchestras became records. Lamp lighters became light switches. Over this period, lifestyles changed radically. As I posited in 2023, we are on the edge of a similar shift where LLMs and “AI” will radically shift our experience of services from “work” to “products.” And with that shift, we’ll likely see services employment plummet as a fraction of work:

Where this stops, we don’t know. But with self-driving cars, autonomous delivery robots, humanoid robots, and “self-programming computers” either here or on the near horizon, I can rest confidently that while our war in Iran is winding down, our war with the machines is just beginning.

So let’s pivot to the conservative movement…

What’s Left to Conserve?

Why the “Invention of Conservatism” is Fracturing

I had the pleasure of attending the Spring 2026 meeting of The Philadelphia Society. For the uninitiated, this is the intellectual “town square” of the American Right, founded in 1964 following the Goldwater defeat. It was intended as a sanctuary for the movement’s brightest—academics, journalists, and high-conviction activists—to debate the future of freedom away from the immediate, distorting pressures of the next election cycle.