You Can Lead a Horse to Water

But you can't make them think

AI-Generated Summary

The “impossible” disentanglement has been done — and it just won an award. In 2020, the FT dismissed my passive-investing arguments as “far-fetched,” the blow-up prediction as “fatuous,” and disentangling passive’s effect from larger forces as “impossible.” Hannah Unterberg’s prize-winning paper now shows passive flows — not vanishing skill — penalize active managers

The FT’s fallback — the “poker table” — cannot generate any of the actual findings. The paradox of skill predicts alpha compression, not a sign flip on Active Share timed to passive flows. And its premise is false: the fish never left the table. Retail noise trading is at record highs, yet the correctors are starving while market makers post historic profits — the noise trader’s losses now fund facilitation, not price discovery. A poker game whose only reliable winner is the house is called a casino.

Unterberg isn’t carrying this alone; six independent literatures now identify one machine. Incidence (Jiang: flows inflate the largest, most overvalued names), elasticity (Haddad: active offsets only ~two-thirds), clearing (Sammon-Shim: firms, not arbitrageurs, supply the shares), information (Coles: index ownership causally reduces research production), returns (Unterberg), and stability — my model with Krishnan and Sturm showing that past calculable passive-share thresholds (as low as ~65%), violent boom-bust volatility becomes endogenous to the market’s architecture. The claim called fatuous is now a formal result.

2022 was the mechanism running in reverse. Lu and Wu’s dual-share test shows identical-fundamental corporate share class “twins” diverging after Fed surprises based purely on rebalancer ownership, attributing one-third to two-thirds of the market’s excess-return response to monetary shocks to this single flow channel. The mega-caps that led the fall roared back at still-elevated rates: flow, not duration.

The concentration premium is compounding — and the answer to “what should we do?” is coming. My research finds the flow premium to the largest, most volatile names has accelerated ~0.33pp per year since 2005 — a run rate near 7% annually today, roughly a doubling versus their own size cohort cumulatively, and convex from here. Because it’s flow-driven rather than earned, that’s stored energy, not banked return.

The Main Event

In December 2020, Robin Wigglesworth wrote up my arguments about the structural impacts of passive investing in the Financial Times, after a two-hour interview, a pass through my work, and, by his own account, conversations with plenty of others. He described the core mechanics accurately: fully invested index funds create a secular lift in valuations, and market-cap weighting mechanically allocates the largest share of every new dollar to the largest constituents, so appreciation raises a name’s claim on the next dollar in. He even conceded that passive was plausibly a contributor to several of these patterns.

Then he dismissed them. The notion that passive had become a nefarious force wrecking the natural order of markets was “far-fetched.” The prediction that it would eventually blow up and rip a hole in financial markets was “fatuous”—the word that closed the article. And disentangling passive’s effect from larger forces was, in any case, “impossible.”

In June, Hannah Unterberg’s “Passive Flows, Active Woes: Passive Investing and the Decline of Active Mutual Fund Alpha,” out of UC Irvine, took the Two Sigma Award for Best Paper in Investment Management. It disentangles the effect, showing that passive flows penalize active tilts through demand—no deterioration in manager skill required. A prediction I made over a decade ago:

And this month, reviewing the paper in FT Alphaville, Wigglesworth pivoted: the explanation for active underperformance is now the “poker table”—Michael Mauboussin’s paradox of skill.

What the Unterberg paper shows

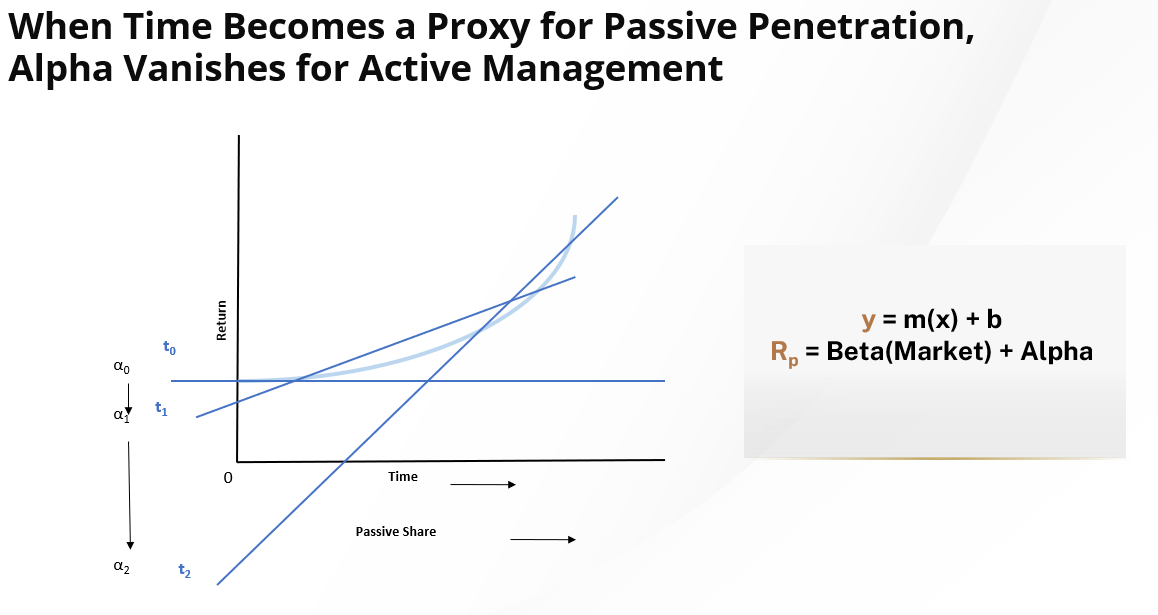

Standard theory has long predicted that as passive grows and the active sector shrinks, the surviving active managers should face less competition for mispriced securities and earn higher alpha. The data shows the opposite.

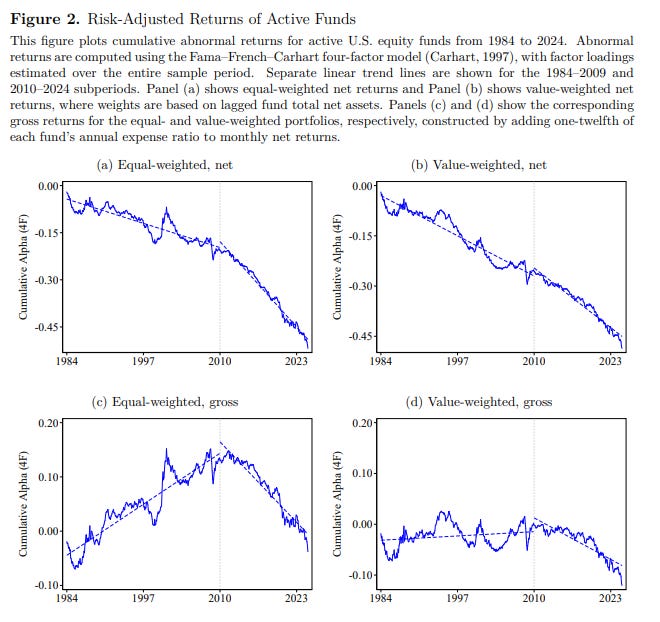

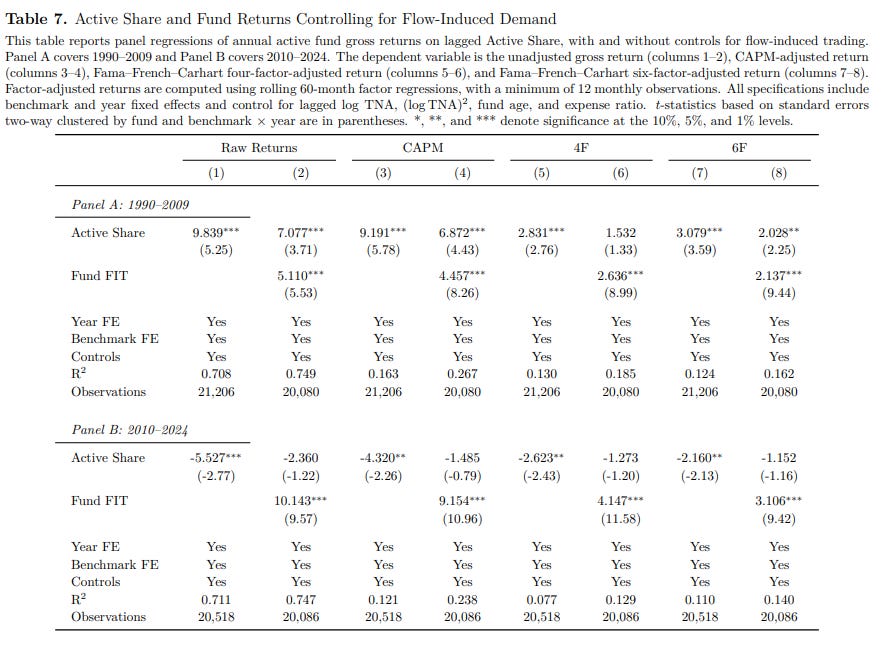

Unterberg documents that the average active U.S. equity fund earned a four-factor alpha of roughly -0.72% per year from 1984 to 2009. After 2010, as passive vehicles took market share in earnest, that underperformance more than doubled, to -1.82% a year.

This is not a fee story. The decline shows up gross of fees: the value-weighted active sector earned a gross alpha close to zero before 2010 and a four-factor gross alpha of -0.66% per year after. Fees fell over this period. The returns themselves deteriorated.

The smoking gun is Active Share. Historically, a fund’s deviation from its benchmark predicted outperformance. Post-2010 the relationship flipped, and high Active Share funds now systematically underperform low Active Share funds.

Unterberg then identifies the mechanism. She constructs a fund-level measure of flow-induced demand and shows that once this enters as a control, the negative relationship between Active Share and performance collapses to statistical insignificance. The post-2010 penalty on active tilts loads onto the flows, not onto any measured change in manager ability.

For a plausibly exogenous test, she isolates beginning-of-month passive inflows driven by mechanical 401(k) paycheck contributions, flows plausibly predetermined with respect to contemporaneous fund performance. In those windows, low Active Share funds earn higher daily returns and high Active Share funds get penalized, a monotonic gradient that appears for passive flows and vanishes for active ones.

The pivot to the poker table

In his Alphaville piece, Wigglesworth acknowledges the paper, but then proceeds to dismiss it as “Alphaville suspects” there are better alternatives. Borrowing from Mauboussin’s paradox of skill, the argument runs that passive investors drummed the “fish” out of the market, leaving only “sharks” at the final table. The game got harder because the remaining players got better.

It’s an elegant story, and it may describe a real force. But it can’t be the better explanation of these particular findings, because it can’t generate any of them.

The paradox of skill predicts alpha compression: the spread between good and bad managers narrowing toward the fee drag. It offers no mechanism for Active Share to flip from a positive predictor into a negative one; tougher competition makes deviation less rewarding, not punished. It has nothing to say about why closet indexers get rewarded during the first three trading days of the month, when mechanical retirement contributions arrive, and at no other time. And it can’t survive the hinge result: control for flow-induced demand and the Active Share penalty vanishes while the flow term stays significant. Skill and competition do not hide inside a lagged mechanical demand variable.

The two objections

Wigglesworth raised his two narrower objections before reaching for the poker table, and both are answered inside the paper he was reviewing.

The first is a measurement concern: an active manager facing redemptions need not liquidate every favored overweight proportionately, so a holdings-based flow measure rests on an assumption about how flows become trades. Fair enough. The constructed measure does follow the standard proportional-trading approach, with outflows passing through at close to one-for-one. But the objection is not an alternative explanation, because the beginning-of-month result doesn’t depend on the constructed measure at all. For discretionary liquidation to produce it, managers would have to generate a return gradient that appears only for passive flows, only in the first three trading days of the month when retirement contributions land, and vanishes for active flows. That’s a mechanical pattern, not a discretionary one.

The second objection is that active managers remain “price setters” while passive funds are mere “price takers.” This confuses how an order is submitted with whether it moves the price. Price-taking describes accepting the available quote; it says nothing about the marginal seller who must be induced to part with shares. A mechanical, valuation-blind buyer can take the offered price and still force the clearing price higher, no opinion about value required. And the premise that active investors still fully set prices is rejected by the evidence. Haddad, Huebner and Loualiche estimate that when some investors stop responding to price, the strategic response of everyone else offsets only about two-thirds of the effect. Jiang, Vayanos and Zheng show where the residual impact lands: disproportionately in the largest firms, and particularly in the ones already most overvalued. The supposed price setters do not supply an infinitely elastic countertrade. They absorb part of the shock and pass the rest through.

Compounding Evidence

Unterberg is not being asked to carry this argument alone. She completes a chain whose links have now been identified by separate researchers, with separate methods, none of whom needed the others to be right.

Jiang, Vayanos and Zheng establish the incidence: passive inflows disproportionately raise the prices of the largest firms, and especially of large firms that are already overvalued. Their framework even permits the aggregate market to rise when the passive inflow comes entirely from investors switching out of active funds, and they show that the flow-induced volatility itself makes correcting the distortion less attractive. Haddad, Huebner and Loualiche establish why active capital doesn’t arbitrage it away: the strategic response is incomplete, as above. Sammon and Shim establish who actually clears the flow, and the answer is not valuation-sensitive institutions leaning against the bid; most demand-side institutions trade in the same direction as the index funds. The shares come from the firms themselves, supplied at nearly a one-for-one rate through non-primary issuance like stock compensation, with price acting as the coordinating mechanism. One can argue that firms are informed sellers of their own stock, and that issuance into overvaluation is itself a corrective force. Grant it. What that concedes is the point at issue: the marginal counterparty to the passive bid is the issuer responding to price, not the infinitely elastic pool of valuation-sensitive arbitrage capital the price-setter story requires. And notice what kind of correction issuance is. The firm does not sell the price back toward value; it sells additional paper at the distorted price, which had to move first to induce the supply. Stock-compensation issuance answers payroll schedules, not valuation views. To the extent the flow-clearing trade is informed, the information runs one way—insiders supplying shares at inflated prices to the household’s mechanical bid. That clears the quantity while leaving the price where the flow put it. Coles, Heath and Ringgenberg establish the information effect: exogenous increases in index ownership cause declines in Google searches, EDGAR views and analyst coverage—a causal finding that indexing reduces the production of firm-specific information. And now Unterberg establishes the return consequence: the managers who keep producing and acting on differentiated views are the ones the mechanical flows penalize.

Incidence, elasticity, clearing, information, returns. Each link identified separately; together, successive components of one machine. One can argue about the strength of any individual link. What is no longer available is the claim that there exists no identified bridge from passive ownership to mega-cap price impact, or from passive growth to weakened information production.

The claim called fatuous

“Most of all, the theory that passive investing would inevitably blow up and rip a hole in financial markets when the tide recedes seems a little fatuous today.” — Wigglesworth, Dec 2020

In A Model for Passive That Breaks the Market, Hari Krishnan, Stephan Sturm and I formalize it relying on simple insights. One can dispute the calibration and the modeling choices; the paper devotes a section to anticipating which assumptions will be attacked, and defends each. The most natural objection—that at some level of distortion, new unconstrained capital must re-enter and correct—is the Grossman-Stiglitz reflex in its purest form, and the model already prices it: the Haddad strategic response enters as a time translation, delaying the thresholds by roughly thirteen years without changing the destination. That is now the available debate: assumptions and mathematics.

What is no longer available is dismissing the conclusion as self-evidently absurd. The claim called fatuous is now a formal instability theorem inside a calibrated model whose economic premises are independently testable, and are being confirmed one by one.

Call it the sixth link: incidence, elasticity, clearing, information, returns—and stability.

The false premise of the empty table

The poker table rests on an empirical claim that no one checks: that the patsies packed up and left the game for index funds, leaving only professionals to grind a shrinking pool of alpha against one another. But the patsies didn’t leave. We are living through the largest explosion of retail noise trading in modern history—zero-commission accounts, the meme-stock manias, the retail options boom, crypto. The dumb money didn’t go anywhere. If anything, it got louder.

Under Grossman and Stiglitz, that should be a feast. Informed traders are paid in alpha for the costly work of correcting mispricings; flood the market with noise traders and the pool of available alpha should widen, and the sharks should be gorging. Instead, as Unterberg shows, the high–Active Share managers, the ones actually deviating to pick stocks, are starving. Under the poker table analogy, that’s impossible.

Except someone is eating. In the same window that the correctors have been starving, the market makers built to intermediate the retail flood have posted the best numbers in their history. Citadel Securities, the largest single destination for Robinhood’s order flow, just booked a record $4.3 billion of trading revenue in one quarter, up 28% year over year, with net income near $1.9 billion, and it “benefited from volatility.” Jane Street, Hudson River Trading and Susquehanna are at the same feast. The food is being devoured, just by a different animal than the one Grossman-Stiglitz promised.

This is the distinction the poker table can’t see. There are two ways to make money off a noise trader. You can correct him: take the other side because you have a view about value, and get paid when price converges to it. Or you can facilitate him: take the other side because you can hedge it out in milliseconds, and collect the spread and the order flow while staying indifferent to whether the price is right. The corrector needs price discovery to happen; the facilitator only needs the trading to continue.

Grossman-Stiglitz routes the noise trader’s losses to the corrector, and that is what makes the market self-heal, because the reward for information funds the production of information. The modern market routes those losses, to a first approximation, to the toll booth, which produces nothing about value at all. Record market-making revenue has many parents (volume, volatility, market share, product breadth) and it is an existence proof the poker table cannot use: the structure that starves the correctors makes facilitation spectacularly profitable at the same moment, on the same flow. The noise trader’s losses have not vanished from the system. Increasingly, they fund the activity that lubricates the market rather than the activity that prices it.

And it matters who the noise trader is. In the models he is an abstraction. In practice, they are a household—the same household whose 401(k) rides the mechanical bid—now holding a phone with a sportsbook in one app and zero-day options in the next. The industry’s response to his arrival was accommodation, not correction: payment for order flow, gamified execution, an ecosystem engineered to keep him trading. The casino did not spring up in opposition to the index revolution. It grew in the space the index revolution vacated, monetizing the engagement that mechanical investing no longer required.

A defender will say market makers make the market efficient—look at the spreads. But there are two efficiencies here, and the error is conflating them. Market makers enforce consistency: no arbitrage between venues, ETFs pinned to their baskets, one price everywhere at once. What they don’t enforce, and are built not to enforce, is correspondence to value. They will make a tight, orderly, arbitrage-free market in a stock at whatever price the flow dictates. Tight spreads measure intermediation efficiency, not price-discovery efficiency—one more case where the comfortable reading and the real one print the same number. And this retires the last living version of the poker table. Citadel’s record haul isn’t the sharks winning the pricing game; it’s the pricing game being displaced by a turnstile. Ask who ultimately absorbs the retail bid, and increasingly the answer is an intermediary with no durable view of value. The tempting rescue is to redefine the shark: skill didn’t vanish, it migrated from reading balance sheets to managing flow. The skill is real. But the paradox of skill was never a claim about who gets paid; it was an explanation of why prices are right, and facilitation produces no view about price, however brilliantly executed. A poker game in which the only reliable winner is the house is not a contest of skill among the players. It is a casino.

And the reason the correctors can’t touch that pool isn’t that passive flows somehow “overpower” the noise. The players who could eat it have been walked out of the room mid-hand. Grossman-Stiglitz requires that informed capital can deploy against the mispricing. But the informed are being redeemed—capital is draining out of the correctors and into the mechanical bid—and the survivors are benchmark-chained, unable to take the large positions against the largest names that correction would demand. The fish are present. The correctors are defunded and handcuffed.

And when a corrector does take the other side, the flow doesn’t feed it. It runs it over. Ask Melvin Capital. Melvin was a top-performing, fundamentally driven fund carrying a large short in GameStop, a declining mall retailer it judged wildly overvalued. Whether that valuation call was ultimately right or wrong turned out not to matter. A coordinated retail bid, organized in the open and amplified by the options dealers it forced to hedge, ran the position over and margin-called the fund into a bailout it never recovered from; it wound down the following year. That is retail noise reaching the professional table and executing the professional, the exact opposite of noise becoming harvestable alpha for the skilled. And the survivors drew the only rational lesson: stop shorting anything the flow is supporting. Aggregate short interest as a share of market capitalization has since fallen toward historic lows. Even if you insist Melvin was simply reckless, the population-level retreat isn’t idiosyncratic. An entire ecosystem learned that correcting flow-supported overvaluation is a firing offense.

This is where the classical picture and the real one part ways, and the name for the gap is non-ergodicity, the distinction the physicist Ole Peters has spent a decade forcing back into economics, against the same resistance we will come to in a moment. An ergodic system is one in which the average across many players at a single moment equals the average of one player’s experience over time: the ensemble equals the trajectory. The poker table is ergodic to the bone. It reads Melvin’s loss as a transfer, alpha changing hands from one corrector to another, the pool conserved and participation intact. Average over the ensemble and correcting mispricings remains a positive-expectation activity, so the system self-heals. But no fund lives in the ensemble. Each lives one trajectory through time, and that trajectory has an absorbing barrier at ruin—hit it once and you never see the later hands in which your thesis pays. Melvin doesn’t get to average over the parallel worlds in one of which GameStop obliged. It is simply gone. And whatever the accounting identity of the counterparties who captured its losses, the specialized capacity it embodied—the willingness and mandate to carry a large fundamental short—did not transfer intact to another corrector. The dollars were conserved. The capacity was not.

None of this is unknown to finance. Shleifer and Vishny wrote down the limits of arbitrage three decades ago: financing constraints, forced liquidation, the agency problem of managing other people’s money through a drawdown. Position sizing and survival are components of investment skill, not excuses for its absence—granted, and Melvin plainly failed that test. But that is precisely the concession the poker table cannot absorb. If surviving the flow is now a binding constraint on correcting the price, then the parable’s premise—that exit is harmless selection, leaving a stronger population to do the same job—is false in its own terms. The limits-to-arbitrage literature is not a defense of the poker table. It is the reason the poker table was never a safe metaphor to build on.

That is the assumption the poker-table intuition smuggles in and the market violates. In an ergodic market the loss of any one corrector is invisible, absorbed by the ensemble. In a non-ergodic one, ruin is a ratchet: each casualty permanently removes a node, and because the casualties fall hardest on the funds willing to hold the largest, most contrarian positions, the removals are skill-weighted, subtracting the capacity the market most needs. Then the second-order effect turns one death into a regime. Every survivor watches the execution and re-prices its own odds; taking the other side of flow-supported overvaluation now carries a visible path to the absorbing barrier before vindication can arrive. So they stop. The pool of correction doesn’t shrink because sharper rivals competed it away. It shrinks because it is being destroyed one trajectory at a time, and each destruction lowers the expected payoff to trying for everyone still seated.

So the poker table has the diagnosis backwards. The market isn’t efficient; noise is everywhere. It’s uncorrected, because the mechanism that used to correct it has been redeemed, chained, and, when it shows up anyway, destroyed.

Why the resistance?

A fair question hangs over all of this: why would someone who described the mechanism accurately in 2020 spend six years resisting its conclusion? The cheap answer—he just can’t face being wrong—is the accusation every crank levels at every critic. It is unfalsifiable, it flatters me, and it is usually false. There are three better explanations, and unlike the cheap one, they don’t require me to read anyone’s mind. They compound.

The first is the sunk cost of a story you authored. Wigglesworth is not a neutral bystander to the index revolution; he is its foremost chronicler. His book Trillions is the definitive popular history of how indexing remade finance, and a sympathetic one. To concede that passive has crossed the line from useful tool to price-distorting force is not to lose an argument. It is to append an unwelcome final chapter to your own book. People defend the thesis they’ve built their name on (I am guilty as charged). This is human, not venal. The intellectual and policy architecture around passive investing was built to advertise its private benefits: low fees, diversification, simplicity. Evidence of market-level costs therefore arrives carrying a far heavier burden of proof than evidence of investor-level benefits ever did. The reluctance isn’t only personal; it’s built into which claims the system is primed to accept.

The second is that the strawman is the load-bearing move, deliberate or not. You cannot grant the mechanism and dismiss the argument in the same breath unless you first make the argument bigger than it is. “Flow-induced demand structurally penalizes active tilts” is too specific, and now too well-identified, to wave away. So it gets enlarged. The 2020 headline did the work in five words—a theory of almost everything—recasting a bounded, testable mechanism as a grand monocausal explanation for all market phenomena. And a monocausal theory of everything is exactly what a sober empiricist should distrust. From there it can be waved off as a force wrecking the natural order of markets, a claim I never made. The Mockery Machine at work. I didn’t argue that passive explains everything. I argued for a specific mechanism with bounded, separately testable consequences:

This mockery is where these debates are lost, every time, because the dismissal only ever lands on the absurdism. The real claim never gets touched.

The third is the progressivist misreading of evolution. This is the deepest reason, and it is barely about Wigglesworth at all. It is a mistake almost everyone makes, which is what makes it so effective. The poker table isn’t just wrong on the facts. It runs the logic of natural selection backwards.

The parable assumes that when the weak players bust out, the survivors are the strong ones, and therefore the population has improved. But selection never optimizes for strength in any absolute sense. It optimizes for fitness within a regime: reproduction in the current environment, and nothing more. Fitness is a relationship between an organism and its conditions, not a trophy the organism carries from one environment to the next. Change the conditions and the fitness function can invert. A trait that was adaptive under one predator becomes lethal under the next, and nothing about the organism got “better” or “worse.”

Now apply that to the game. The poker table assumes the survivors are better card players. Selection guarantees only that they are better adapted to the game as it is now dealt. When mechanical flows turned benchmark deviation into a negative-expectancy activity, the house began paying you to fold and taxing you to bet. In that regime, the survivors are not the sharpest analysts. They are the closet indexers, the benchmark-huggers, the managers who adapted by abandoning the very thing that used to define skill.

Survival has become anti-correlated with the trait the old regime rewarded. Wigglesworth looks at the survivors and infers rising skill; the correct inference is the falling relevance of skill. That is a population adapting to an environment that has switched off the reward for price discovery, not a population getting better.

This was Stephen Jay Gould’s fight in biology. Gould spent much of his career attacking this illusion, the idea that evolution is a ladder from simple to complex, culminating (naturally) in us. In Full House he pointed out that life began pinned against the simplest possible wall: you cannot get less complex than a bacterium. From there, random variation throws off a few more-complex offshoots, not because complexity is favored but because there is nowhere to drift but up from the boundary. The most common organism on Earth is still a bacterium; the mode never moved. What looks like a drive toward improvement is a random walk against a left-hand wall, and the sense of progress is an artifact of staring at the right tail and mistaking its edge for the direction of the whole. Henrik Bessembinder’s work on sources of return identifies the same mechanism.

“Markets got more efficient” is the identical illusion. You stare at the surviving active managers failing to beat the index, and you read progress into it: the market got smarter, the competition got tougher, the mispricings got harder to find. But the very same scorecard is produced by a regime that anesthetizes the market’s immune system rather than sharpening it. Efficiency by competition and efficiency by exhaustion look identical on the SPIVA scorecard, but they are opposites. One is a market whose informed traders are so good that mispricings vanish the moment they appear. The other is a market whose informed traders have been redeemed, benchmark-chained, and taxed out of deviating, so that nothing corrects the mispricing at all. The poker table can’t tell the two apart. The flow control can, which is why Unterberg’s Table 7, where the underperformance loads entirely onto flows and not onto skill, is critical.

None of this requires bad faith. The progressivist reading of evolution is the cultural default; it feels like rigor, which is what makes it dangerous. And the instinct to distrust a monocausal theory of everything is a good instinct, aimed here at a claim that was never monocausal. The error was never the skepticism, only where it was pointed: at a claim I never made.

Recognizing the shape of the resistance also matters because it isn’t unique to markets. It is the same reception Ole Peters’ ergodicity economics has met from orthodox expected-value theory: a correction that is technically hard to answer and institutionally expensive to accept, because absorbing it means conceding that a load-bearing assumption—ergodicity there, self-correcting efficiency here—was wrong the whole time. The resistance is rarely to the evidence. It is to the price of having built on the assumption the evidence removes. And whether or not one accepts Peters’ broader program, the distinction between ensemble averages and survivable individual trajectories is what the poker table suppresses.