What was THAT?

Thursday CPI release offered glimpses of a reversal

Update: apologies for the late notice, but a recorded institutional subscriber call will occur on July 18th. Look for the Zoom invite in your inbox

Summary

Algorithmic Influence and Market Response:

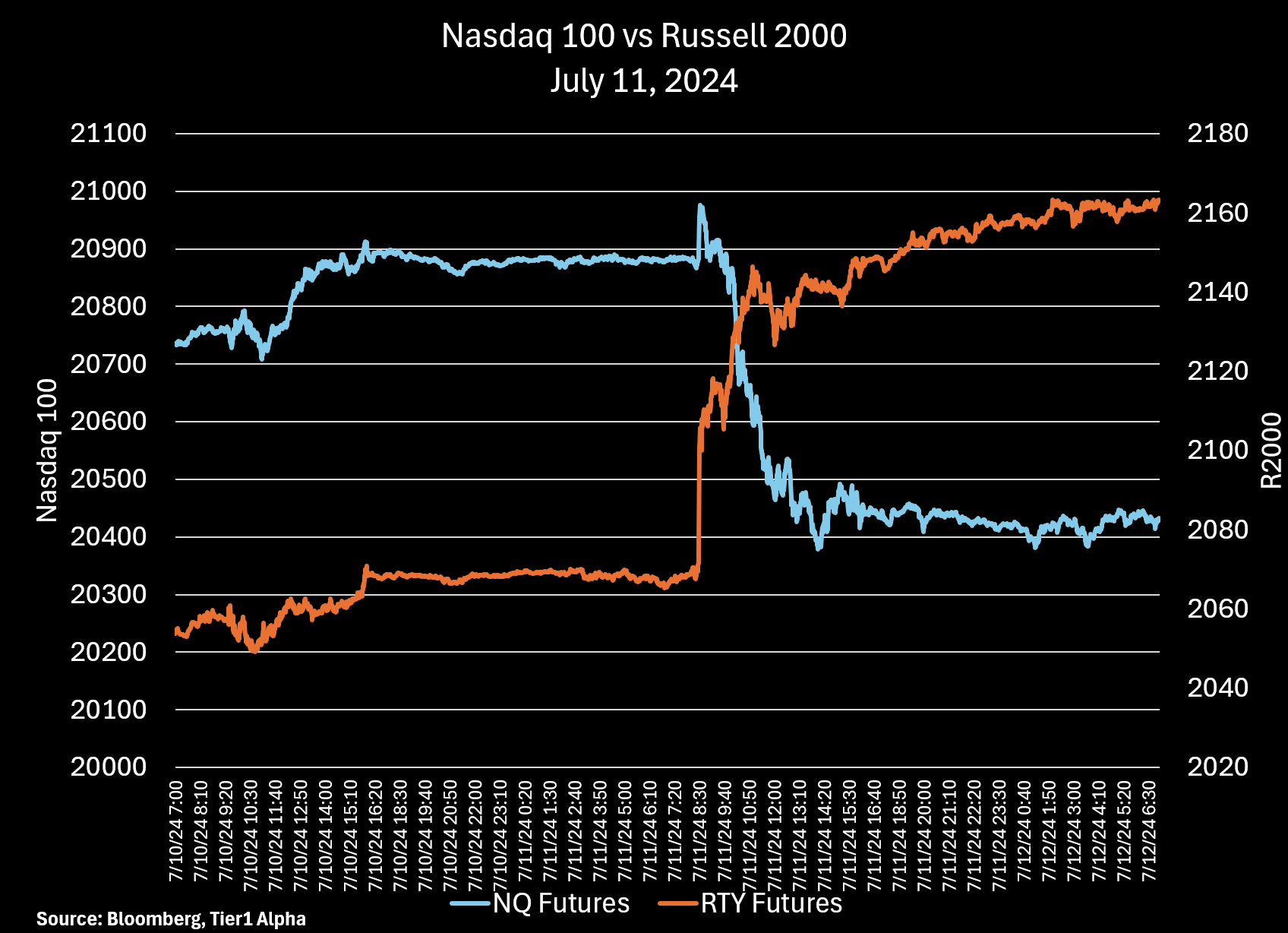

The immediacy of reaction to Thursday’s CPI release suggests algorithmic trading drove a significant portion of the Russell 2000 (R2000) gain shortly after the BLS press release.

The rapid Russell move set off protection trades in the Nasdaq futures which were unwound early in the day. An early dispersion indicated futures traders offsetting new futures shorts by selling positions in the largest NDX stocks and buying back the futures, resulting in a net buy of smaller stocks.

Narratives and Misconceptions:

There were no signs of a rotation from Growth to Value stocks; the performance disparity was due to the "small" factor rather than a genuine value shift.

The idea that anticipated Fed cuts would benefit highly leveraged companies likewise fails. Junk companies underperformed the R2000, showing no correlation with the expected rate cuts aiding these companies.

Market Positioning and Economic Implications:

While it’s possible that the R2000 continues to rally, this feels like yet another false step on the path to active manager redemption. Or perhaps more accurately, we see no signs the active manager redemptions are slowing relative to passive. As a result, we’d suggest we got a preview of what the real event may look like, but it’s yet another false dawn.

The CPI report highlighted continuing deflationary trends, particularly in durable goods, and raised concerns about the broader economic outlook. The Fed is trapped, but not in the manner most believe.

Top Comment

GB offers a thought: Mike, I think what you say makes sense, particularly the notion that people “supply labor” to get things they need or want. But I think the larger point about MMT is not that it might accurately describe how deficit spending works and impacts the economy, but that running deficits does have real mostly negative consequences when it comes to how capital is allocated in the economy. Unless we are talking about the world war 2 generation political class– Eisenhower doing the allocations, allowing the current political class to allocate an increasing share of the GDP sounds like a very bad idea and that is the real point about MMT and its dangers.

MWG: I am sympathetic, GB, but reiterate that I fall on Warren’s side: “Either you believe in representative democracy or you don’t.” I happen to believe a representative democracy, a system where the people elect a temporary elite to represent their interests. If the temporary becomes permanent, we have a problem; likewise, if the people are incapable of electing their own leaders, then we have a problem.

The first is less true than many believe. The average tenure has climbed, but I would suggest this is a somewhat natural evolution due to much longer life expectancy. The one true gain this election season has been the increasingly clear limits of service — a factor that will naturally rectify itself as the Boomers begin their last great adventure.

The second factor can only be accomplished through education. We know the current performance of primary and secondary education is unacceptable; we are FINALLY seeing evidence of halting change. The charter school movement has introduced models of choice and we currently have over 7% of school children educated in charter schools. Truly amazing programs exist, like Coney Island Prep, which Simplify sponsors with our annual ETF conference, that have provided a leg up for disadvantaged children in low income communities.

And MMT is “true” which matters. If properly considered, it highlights that our currency is our country’s equity. While our corporate sector is currently enamored of share buybacks to enrich management, understandably, the opportunities to invest in our infrastructure and human capital are robust. As highlighted in this week’s “Keeping it Simple” with Neil Howe, we have growing signs of change for the better. The Millenials are increasingly pragmatic about the realities of life choices while recognizing that our society must become more inclusive and collective, with true opportunity for success for all, in order to reform. As much as I hate to admit it, my generation is perhaps too cynical, focused on what “is,” unburdened by what CAN be. (yes, that’s a President Kamala joke)

The Main Event

What was that?

On Thursday, we received the CPI print showing the first deflationary impulse into the economy. Hilarity ensued:

The rapid reversal has spurred endless commentary and comparisons to March 2000. Is this the long-awaited rotation into small caps? My work suggests no. First, a couple of observations:

The divergence occurred within minutes of the BLS press release. Nearly half the R2000 gain occurred by 8:33am. This could only occur through an algorithmic response into futures

Within the NDX, a less dramatic, but similar dispersion occurred within the first 30 minutes of open trading as the equally weighted NDX, the QQQE, rose while the QQQ fell. this suggests futures traders offset their new shorts in NQ by selling their single-name positions in the largest NDX stocks (NVDA, MSFT, AAPL). This resulted in a net buy of the smallest stocks as the NQ shorts were reversed. By 10am, the dispersion was done, and once again, they traded inline.