What to Expect When No One's Allocating

Is the "puzzling" underperformance of small cap and international a byproduct of strategies like Target Date Funds?

Top Comment

Evan asks: “Mike, what do you think about Dave Dredge's approach to coping with this dynamic? I think that passive flows damaging market signaling inherently fits into his framework of getting as much exposure to risk assets as you can while buying tail hedges. His main point is central banks will be forced to continue buying their own sovereign debt, driving asset price inflation, but some sort of unwind of passive ripping the current structure of liquidity away from these 'glamor stocks' could likely be included in your 'tail risk' probability set. Intuitively what he says makes sense, participate, but don't go out on the track without good brakes (his aphorism). Interested in your thoughts on this. Unfortunately the 'brakes' are not really available to the average investor.”

MWG: I agree with Dave. The problem is timing, as discussed in this week’s note… at Simplify, we TRY to address this problem, but unfortunately, it requires BOTH turbocharging your returns as a public investor AND having a good set of brakes. It’s devilishly difficult to remain sober, as my flawed efforts have highlighted. My preferred advice is to focus on generating the returns you need rather than the returns your neighbor wants. As I have highlighted, guaranteed REAL returns to bonds are exceptionally high, especially when considering the flawed inflation metrics that overstate inflation as I have repeatedly discussed (more below, btw).

The Main Event

A question came into the “Department of WTF Is Mike Green Saying” at Simplify:

“Mike Green frequently talks about how emerging markets are going to have a tough time going forward because the allocation of emerging markets in target date funds is going to continue to decrease as boomers age. Has he formally published anything with data?”

It’s a fascinating topic, because it gets at the heart of many of the issues that occur when we accept a monolithic entity, e.g. “passive”, owning/controlling a growing share of financial assets. I encourage readers to play along at home as we engage ChatGPT to solve the “problem” for us:

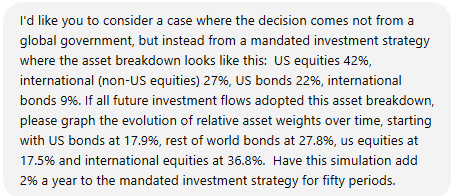

Great. Sounds like a reasonable starting point. Now let’s veer off into “absurdistan”:

OK, everyone with me so far? We’ve migrated to our classic, “If everything was passive” type world where no one is actually setting “prices” — instead they are imputing market “values” for these assets through financial models:

Now stop and think about this for a second — if there are no market prices, then we would STILL be engaged in the process of financial analysis in order to obtain imputed price series. For those who are paying close attention, this is exactly the process by which the BLS and BEA determine “imputed prices” for various data sets we cannot directly observe, e.g. “Owner’s Equivalent Rent.” It’s also the source for data series like “Portfolio Management Services.”

For a quick segue into inflation, while many in the alt-media decry the use of hedonics to keep prices from rising, e.g. “New cars! Flat Panel TVs!” the reality is that the hedonic and imputed adjustments have actually served to RAISE reported prices relative to their market-based equivalent surveys. This is particularly true if we exclude the mothership of imputed prices, OER. As you can see, the relationship between market-based and total can often boil down to commodity pricing (i.e., very market-derived pricing). Over the last year, market-based metrics have fallen even more sharply than commodity prices might suggest — this is the China-driven deflation in goods. This discrepancy is why I am increasingly concerned about DEFLATION rather than inflation… and the government is using the wrong models to track it:

Returning to the subject at hand, if prices are imputed rather than market-based, they reflect policy choices rather than the invisible hand:

And let’s make an extreme policy choice:

Now obviously this is a reductio ad absurdum argument, but because prices are always determined at the margin it is a useful exercise to consider when we discuss the impact of growing passive and systematic allocation strategies on financial markets and expected returns.

So let’s layout the underlying hypothesis:

“Because the MARGINAL allocation of capital is now coming through some form of retirement strategy like a TDF, the pressure on markets is to increasingly conform prices to the POLICY choices of these allocators”