Two's a Crowd?

A Hypothesis on passive/systematic portfolio construction impact on theories of crowding out

Summary:

We are experiencing an anomaly where despite rising real risk-free bond yields, there has been no structural re-rating of U.S. equities. This challenges traditional discounted cash flow models, which would suggest a substantial increase in corporate earnings growth or a decrease in the equity risk premium to justify the current valuations.

The likely culprit is increasingly inelastic bond/equity relationships, driven by the prevalence of systematic "model" portfolios like target date funds. These portfolios have fixed allocations that are insensitive to changing yield conditions, essentially freezing asset allocations.

In a hypothetical scenario of a 100% passive market with fixed allocations, bond and equity prices would be determined solely by the intersection of savings flow and supply of bonds and equities. This could allow equity valuations to rise even as bond prices fall (yields rise), mainly because demand is fixed and supply determines the price.

Recent academic research shows a negative relationship between bond and equity returns, reinforcing the idea that they're treated as competing assets within a portfolio, not as competing claims on the same underlying assets. The author speculates that the inelasticity in portfolio allocation techniques might be the hidden mechanism causing this unusual market behavior, posing the risk of a violent market reversal if these allocation models are challenged.

Top Comment:

There were several comments on the Serenity prayer. I’m glad most took it as intended. If only it were so easy to practice what we preach!

Meanwhile, Evan James came in with a humdinger:

On the decreasing usage of "openings" in Fed statements/writing: I've long thought that the Fed has already decided what they want to do, and in order to maintain the appearance of 'data dependency' they support their chosen path with the favored data point de jour. When it moves against them, they simply never mention it again and move to the next one that supports their aims. See: Near Term Forward Spread, Real Wages, inflation expectations, etc... I'm sure super-core inflation and JOLTS will be relegated to the dust-bin of data dependency in due time.

MWG: Evan, unfortunately I agree with you. This month we get to see if Jerome Powell meant it when he said “There’s really not anything that we can do about oil prices,” he said. “They’re set at the global level.” I am hopeful he sticks to his statement, but I’m nervous he won’t.

The Main Event:

This week’s note is going to be painfully theoretical in construction and much shorter than normal. Over the course of 2023, I have written extensively on the deteriorating value proposition for US equities, especially relative to US risk-free bonds. Despite the very notable and structural shift in bond valuation, with REAL risk-free bond yields climbing from -0.6%/yr in 2021 to +2.1% in 2023, we have seen no structural re-rating of US equities (or global equities) as you might expect under these conditions.

The “money shot” chart here is the relationship between 30-year TIPS yields and forward dividend yields on the S&P500:

Expressed differently, guaranteeing real purchasing power gains over the next 30 years has become substantially cheaper in the last 18 months. And yet oddly, we see little evidence that this has impacted the valuation of equities. Under a discounted cash flow valuation model, this can only be explained by expectations for a substantially increased real growth in corporate earnings & dividends (difficult from this starting point) or a decrease in the equity risk premium. As a result, the market has become borderline obsessed with the narrative of a coming boom in corporate earnings growth tied to artificial intelligence, and rates markets increasingly reflect fears that the Fed will have to go further still in raising interest rates.

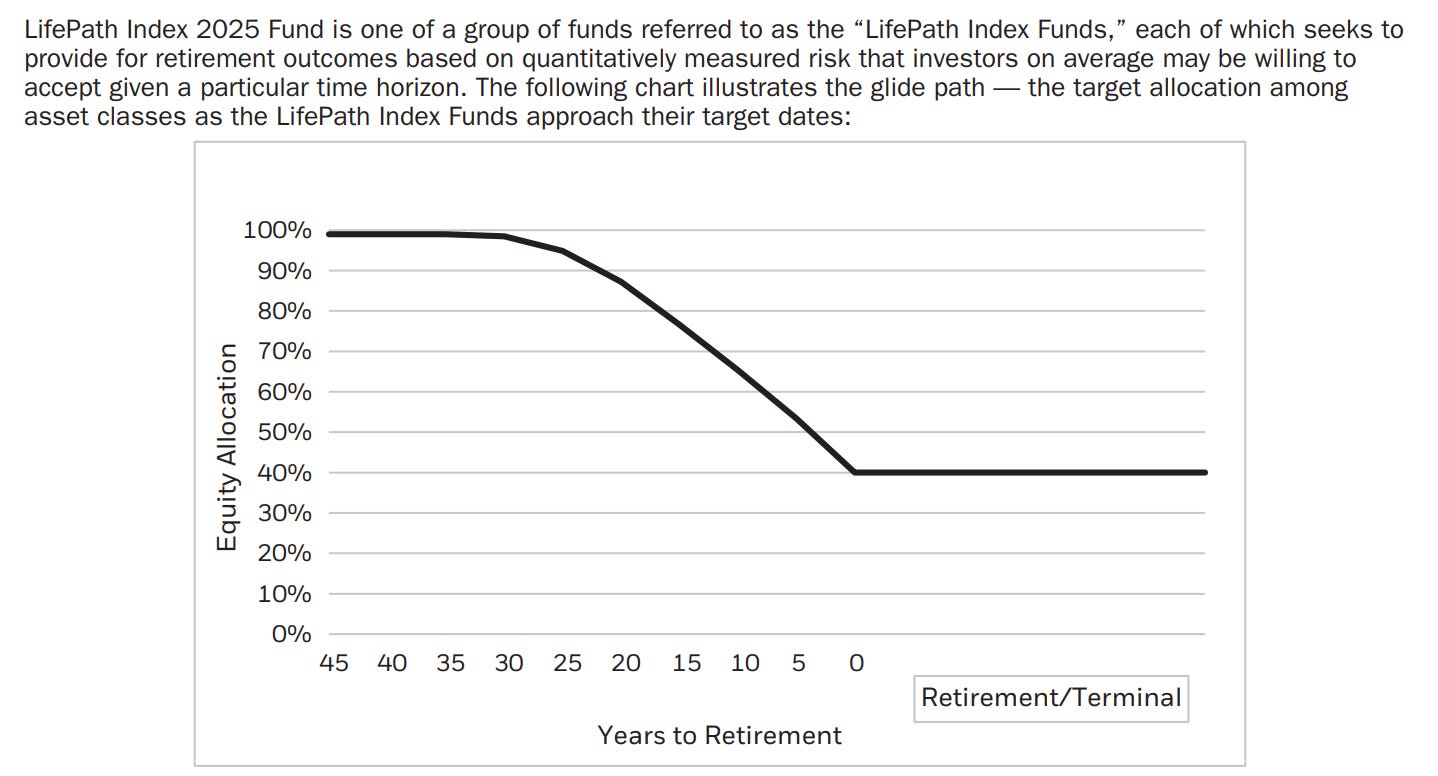

What if there’s a much simpler explanation tied to increasingly inelastic bond/equity relationships as systematic “model” portfolios become a larger and larger fraction of total invested capital? The simplest and most intuitive example would be a target date fund. For example, Vanguard’s 2035 retirement fund has the following allocation:

What is the allocation of this portfolio when bond yields are zero? Unchanged. What if bond yields went to 20%? The same. It is PERFECTLY inelastic across assets. The expected forward return of the asset class has no impact on allocation. Moving to Blackrock’s target date fund portfolios (equal opportunity offender), we can see that there is NO input for bond yields in allocation:

This is a byproduct of a world in which we decided to ignore the disclaimer, “Past performance does not guarantee future results.” While we can argue Monte Carlo-type analysis allows us to stress test portfolios, they are, by definition, using historical return data and assuming that something like a historical return distribution defines the possible range of outcomes. The shortcut to “expected returns and risk looks like historical return and risk” results in “optimal” portfolios that freeze allocations regardless of asset “state” characteristics (like valuation, yield, etc).