The Phantom Tollbooth

The Kingdom of Wisdom Beckons

This week, I’m going to be stingy with the paywall. I will publish the entirety of the Bitcoin saga as a downloadable PDF next week. But for this week, it’s going to be below the paywall as a “reward” (punishment?) for my paying readers. In the meantime, some updated thoughts on oil and the Middle East… also, Nick Nemeth is offering a 30 day free trial to my readers. If you’re interested, sign up for a month. Unfortunately, Nick does not have the same luxury that I do in offering cheap access to his Substack, as it is his primary source of income. If you can afford it, I think he’s worth it.

We’ve been here before:

Let there be no mistake about the cost of war. We have arrayed an impressive international coalition against Iraq, but when the bullets start flying, 90 percent of the casualties will be Americans. It is hardly a surprise that so many other nations are willing to fight to the last American to achieve the goals of the United Nations. It is not their sons and daughters who will do the dying. Most military experts tell us that a war with Iraq would not be quick and decisive, as President Bush suggests; it’ll be brutal, and costly. It’ll take weeks, even months, and will quickly turn from an air war to a ground war, with thousands, perhaps even tens of thousands, of American casualties. — Senator George Mitchell, Jan 11, 1991

I fielded a call this week from a hedge fund manager who told me I was delusional. His exact assessment was that “Iran has already won.”

It was a perfect, real-time distillation of the consensus analytical trap. He sees the Strait of Hormuz functionally closed, U.S. interceptors being drained by cheap drones, and Brent crude elevated. To a standard model, that looks like an unmitigated U.S. defeat.

If this is an Iranian “victory,” it is the most suicidal victory in modern history. Winning a war of attrition by threatening your own country with a return to the pre-industrial age is only a victory if your goal is martyrdom. And some monolithically ascribe that goal to the Iranian people. I do not. But if Iran has “won” by breaking the global energy plumbing—specifically the structural 3-to-5-year hole in LNG and refining from the Ras Laffan strikes—who are the actual losers?

It is not the United States.

The consensus is screaming about a permanent, 1970s-style geopolitical rupture. But the commodity term structure is calling their bluff.

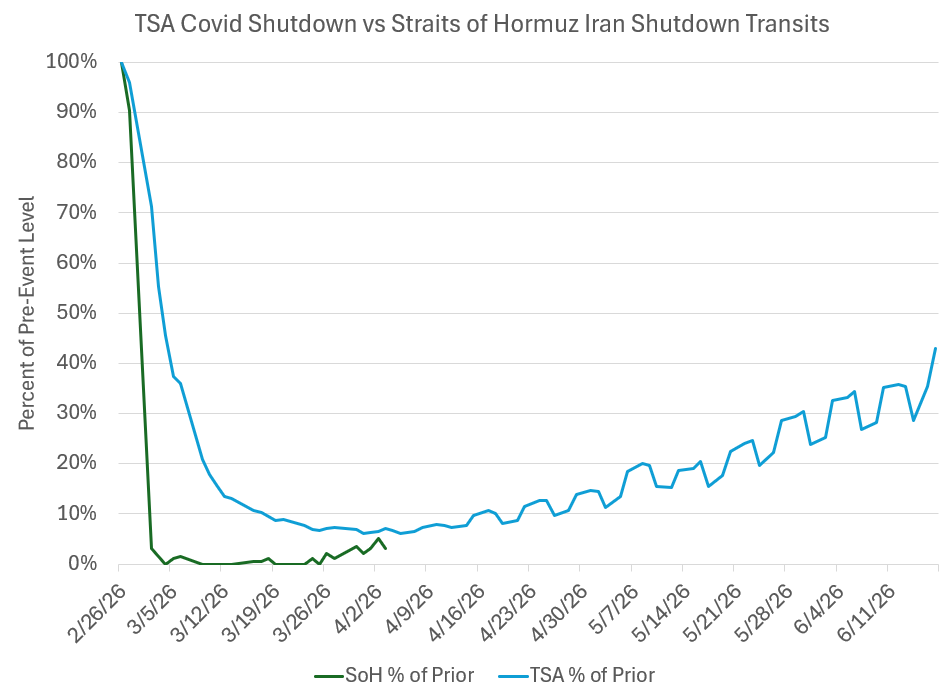

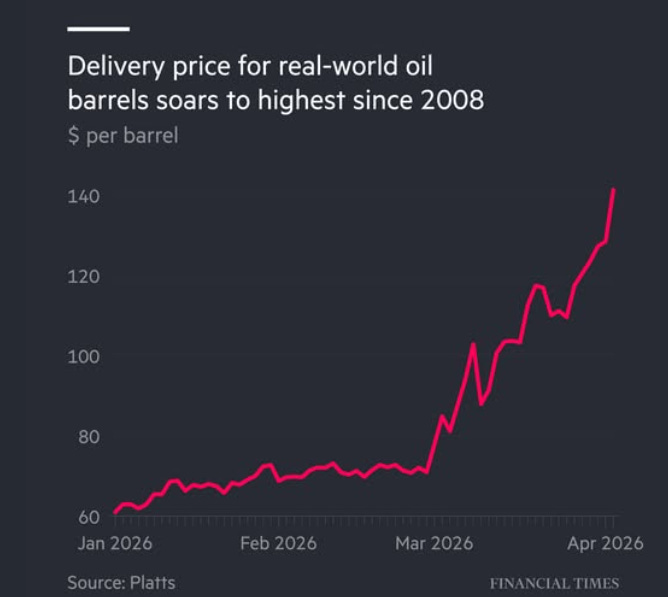

Look at the COZ6 (Dec 2026 Brent) contract. It is sitting at $79.02. That is up a mere 12.5% from June of last year—a period when the market was completely asleep. This is an absolute joke for a “World War III” energy crisis. The back of the curve is telling you the Strait of Hormuz will be cleared quickly. If you disagree, there are plenty of trades available. The on-the-ground reality is that over 50% of the blocked oil has already found alternate routes. Traffic is slowly opening in the Strait through the Oman coastline (~1.6 MMBpd starting this week), Saudi pipelines are maxed out (7 MMBpd), UAE pipelines are flowing (~1.5MMbpd), and Iran is shipping it’s own oil and tolling additional oil (~2MMbpd). While press headlines scream “$2MM toll!”, that is a $1 per barrel premium for a VLCC. And those deals become free if the IRGC falls. For those counting, that’s roughly 11MM of the 20MMbpd. The threshold for complete replacement, given gains in pipelines, increased production, and likely demand destruction, is 35%. We’re already well ahead of COVID…

Tanker rates are falling, but insurance remains expensive at 4x normal if you can get it. Both are likely to continue to retreat. But impressive as the numbers you may hear sound, that quadrupling of tanker insurance adds about $0.50 per barrel.

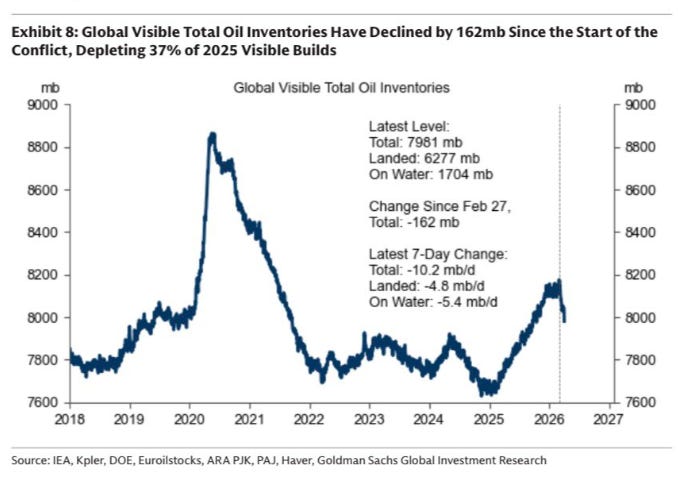

And remember that the “lost” 20MMbpd were from an oversupplied 105MMbpd total market. So we’re now delivering roughly 96MM of 105MMbpd pre-war demand. That excludes releases from strategic petroleum reserves (which must ultimately be made up in the future). The net result is that the alarming inventory drawdown of 10.2MMbpd will be lower this week. And likely even lower the week after that. And the 2025 floor of ~7700 mb is important, but we can go lower if needed. Rich countries can afford it. Poor countries cannot. Sucks to be poor, I’m sure. Never given it much thought (since it is 2026, I feel obliged to add the “/s”. At least it’s not March 2020).

Super backwardation in oil markets — prompt delivery at a 30% premium to spot, spot at a 30% premium to Dec 2026 futures — is incentivizing inventory release into markets; and the premium of prompt for both crude and products is destroying demand. Leisure travel is being reduced, work from home is being deployed, and emerging markets are introducing emergency rationing.

More importantly, the imminent arrival of U.S. ground troops fundamentally alters the kinetic math. The moment Marines land, the IRGC can no longer afford to waste their degraded missile inventory lobbing shots at passing tankers. They must pivot 100% of their surviving assets to a defensive, anti-invasion posture. By forcing Iran to fight a symmetric ground war, the U.S. functionally neutralizes Iran’s asymmetric anti-ship campaign. The crude blockage is temporary, even if the UAE LNG hole is structural. If traders actually believed in a permanent oil void, that Dec ‘26 contract would be in the triple digits. Maybe you believe differently. The markets are there for you to place your bets.

With this degree of positive carry, shorting is somewhat pointless. If I’m right, those Dec 2026 contracts fall to $60 (perhaps lower, depending on supply and demand). If I’m wrong, the carry from $79 to $110 (or higher) eats me alive. There is no trade on the short side. So you are hearing the motivated reasoning of crude oil longs in market commentary, and the cowardly voice of “no position” on the other side. I’ll remind you, that my insights took you for a 30% loss in Oil vs Gold last September… or a 44% gain, depending on how you want to look at it. Right now, there is no clear trade in either asset in my opinion.

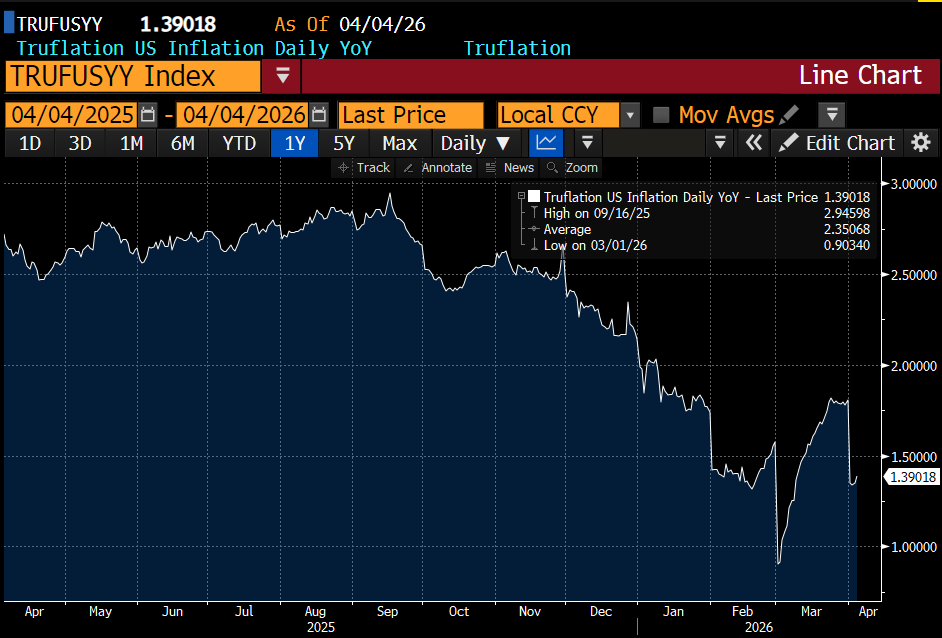

Where I do think there is a trade, the US 2-year yield has violently reversed more quickly. We watched it spike to a 4.00% high in mid-March, prompting pundits to declare a new regime of structural inflation and endless Fed hikes. That was an illusion. It was a mechanical liquidity event—a VaR shock where levered yield-curve steepeners hit margin calls, and front-end Treasuries were indiscriminately liquidated to reduce gross exposure. Inflation is not the concern. I continue to believe Truflation is the “most” honest reporter of current prices:

But if you don’t believe them, perhaps you should check out Penn State, which, like Truflation, uses current real estate prices:

Today, that 2-year yield has fallen back under 3.80%. The mechanical liquidation is exhausted. The global panic is actually funding the U.S. Treasury market, as capital flees the structurally “doomed” industrial centers of Europe and Asia and floods into the only sovereign safe haven that is a net-energy exporter. But it didn’t reach 3.80% in a straight line. A “stellar” jobs report and rising PMI prices has raised doubts that the Fed will need to cut. First PMI Prices… whatever could it be? Oh… oil.

“Yeah, you’re delusional, Mike. Fine… so PMI is being driven by oil… I get it. But oil is a pass-through to everything else.”

Yes, by and large it is. A doubling of oil prices will raise prices… by about 1.5%. You know what else causes prices to rise? Tariffs. And we’re about to celebrate the anniversary of the largest tariff increase in nearly 100 years… with CPI down 0.4% YoY. Inflation swaps have this figured out… short-term inflation up. Forward inflation down. They did the same thing last year when tariffs were introduced:

“OK… but the strong job report…”

Yeah… about that:

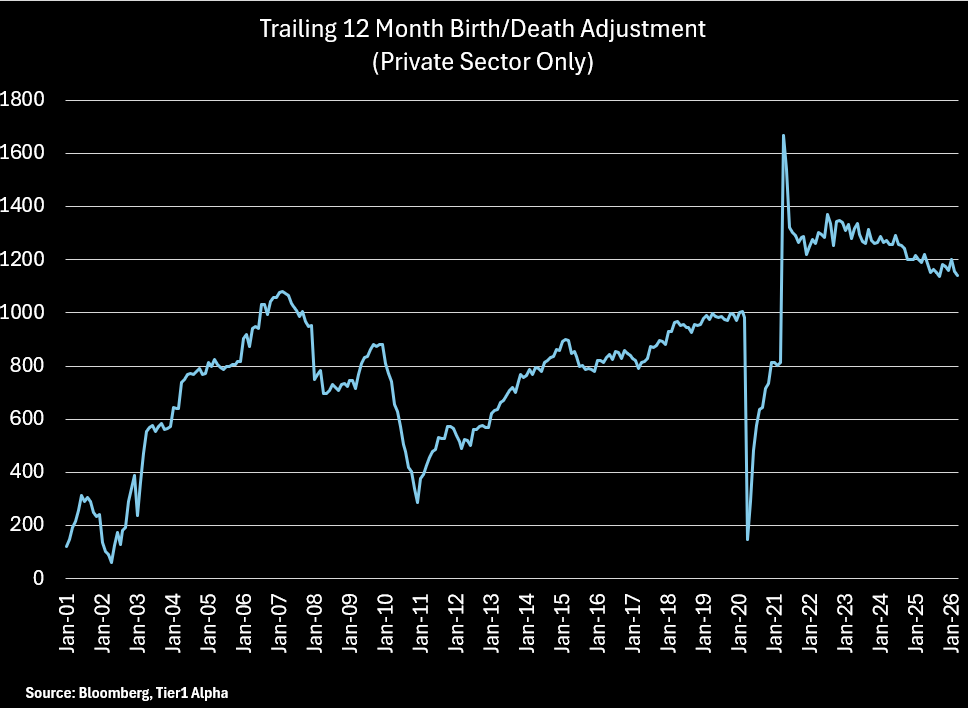

And that’s before we get to the still-not-fixed Birth/Death adjustment, plugging away, adding roughly 100K to-be-revised-away jobs per month:

Which just might leave the BLS in the same position as private credit… “lying.”

And now… what you have all been waiting for…

The Toll Booth: Bitcoin’s Extraction Machine in Practice

Part 2 of “Bitcoin Is Not Sound Money”

Introduction to Part 2

Part 1 established the theoretical machine: Bitcoin’s design hardwires a temporal caste through perfectly inelastic supply, front-loaded issuance, and zero holder accountability. The extraction mechanism is not a bug—it is the system operating exactly as its parameters dictate.

More fundamentally, Part 1 demonstrated that Bitcoin does not fix the pathologies its proponents often correctly diagnose in the existing monetary system. The Cantillon effect is made permanent and immune to democratic correction. Wealth concentration is intensified and stripped of any productive obligation. Rent-seeking is perfected into a “constitutionally protected” (code) activity requiring zero effort.

That was the mechanism. This is what it looks like in the world—what it would become at scale—and why the maximalist endgame would make every problem they identify in fiat catastrophically worse.