The Lord Works In Mysterious Ways

There MUST be a reason for our suffering

Carlo requests a small morsel:

Great piece. Could you help me understand this: "This past week saw one of the most important releases of information since the pandemic with the NY Fed sharing just how fraudulent ALL the data we received over the last five years has been. Those credit scores that were being reported as the “score at origination”? Yeah, they were fake" - the linked article is just about scores from people with student loans. Is there additional reporting from the NY Fed about credit scores being inflated for non-student loan borrowers?

MWG Response: Thanks, Carlo. You can find many new reports on this topic. Rising rates of credit rejections here. The FHA work of John Comiskey is here. Danielle DiMartino Booth has highlighted the Dec 2024 credit report from the NY Fed.

The Main Event

We’re gonna hit on three topics this week before jumping into the book. Now let’s jump into the book…

Just kidding. But I did want to share the 2018 podcast with John Bogle that Cliff Asness often mentions. This was the interview where John acknowledged he “made it up” (the possible level of passive that would create problems). Unfortunately, that clip was lost to the cutting room floor. But the remaining clips… I almost lost my mind listening to Bogle pontificate:

"Cliff, what’s all this about prices. Prices don’t matter in the long run. It’s intrinsic value that matters in the long run. And if you look at the stock market return over history, prices revert to the mean of intrinsic value which I will define as dividend yield and earnings growth… There’s a definite reversion to the mean. “You have to look at price, but don’t give it anymore weight than it deserves.”

MWG: “OK, John… so what’s your weighting schema?”

“Oh, that’s easy you overcharging active asshole:

(PRICE x Shares Outstanding)/(Sum of All [PRICE x Shares Outstanding])”

At 14:22, Cliff offers a defense of passive and the potential for distortion. In Cliff’s defense, this was widely believed to be true at the time:

“I’ll start out, first of all they don’t distort prices. Passive is cap weighted. Passive buys or sells everything proportional to its current size. It has a similar effect on all companies.”

This defense no longer holds in a world of Jiang:

And Haddad:

And Bouchaud:

The central result of GK is that buying (or selling) 1$ of an individual stock on average increases (decreases) the market capitalisation of that stock by M$ in the long run, with M ≈ 1 even for uninformed trades. Buying the market as a whole (i.e. the index or a basket of stocks) has an even larger impact, with M ≈ 5. The multiplier M is therefore very substantial, when rational models would predict that uninformed trades should move the price only very mildly (i.e. M ≈ 0.01), if at all.

This is why I am confident that Cliff will eventually come to the dark side of the passive debate (in Dave Nadig mode, dark = good).

But Bogle… I’m sorry… listen to his TONE while reading his comments:

“Well you tell me about this distortion that’s occurring! How is that occurring? What do we know? We know that index funds account for about 5% of all trading — so give them all the blame for distortion and let the 95% go free… I mean really, that makes no sense at all. Blame the guys that are doing it and not poor old Bogle.”

Unlike Asness, Bogle flat out lied. He KNEW that index arbitrage and market making in index ETFs and options made up the vast majority of trading activity in 2018. Yes, DIRECT index fund trading in mutual funds was only around 5%, but that’s an absurd metric to promote to the public unless you are trying to push “The Greatest Story Ever Sold.”

Look, I want to be nice. So I’ll stop there. But boy, that guy is almost as bad as Nick Timiraos.

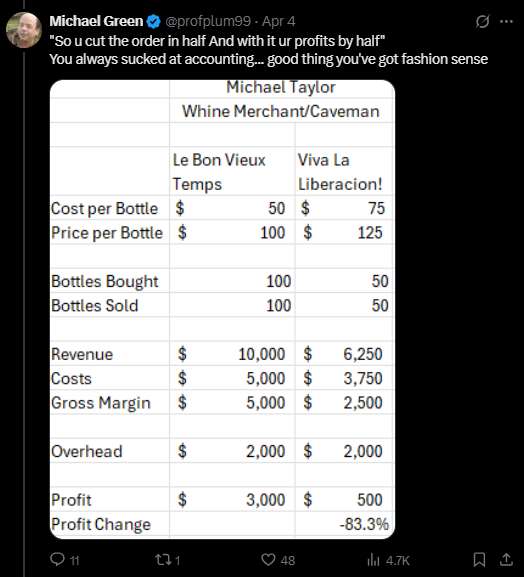

Thing 1: Tariff impact on margins

I had a brief exchange with Mike Taylor, one of my best friends, over Twitter. Mike was sharing some brief thoughts of the impact of tariffs on profits and made a classic error:

Now the nice thing about events like this is they force me to think about our assumptions. My immediate thought was shared above. But it’s a little more complicated than that.

First, wine elasticity is 0.65, meaning for every 1% increase in wine price, demand falls 0.65%. Passing through a 50% wine tariff (assume complete pass through for simplicity) means the price of wine has risen by $25 on a $100 retail price. Note that there is not a 50% increase in price — that would be a 200% pass through. This is going to matter, so keep it straight.

Notice that there are two approaches that can be taken — Scenario 1 and Scenario 2. Scenario 1 is “bite the bullet, buy enough wine to offset future sales and keep inventory unchanged.” Scenario 2 is “accept the new higher price and structurally lower demand and REDUCE inventory to keep ‘days of inventory’ unchanged.” They have radically different cash flow characteristics. Under Scenario 1, cash flow falls 28%; if inventory is drawn down, then there’s large cash generation. Which one do you think is more likely?

Regardless, once we settle down to a new equilibrium, cash generation has fallen a sustainable -28.3%. For those looking for the “fundamental reason” stocks could fall, here you go.

But let’s take a look at the SUPPLIER of whines. Noted French producer, Michelle Merde, I mean Vert:

Here, the factors are reversed — Scenario 1 is MUCH more attractive than Scenario 2, but in BOTH scenarios, my cash flow collapses over the next year, in part because it’s likely too late to change my production plans. Once again, the new equilibrium is lower cash flows even with full pass through; but the risk of ruin in the next year is remarkably high.

Thing 2: Tariff impact on credit spreads. Now add debt leverage and you get what’s happening to credit spreads — dollars are going to be in short supply unless the Fed starts moving VERY quickly. Friday was a squandered opportunity, imho.