Size Does Matter

It’s Not That “Big Won.” It’s That the Index Can’t Stop Buying.

Anyone watching the stock market over the last decade, knows the headline: “A handful of giant technology companies got enormous, kept climbing, and left the rest of the market behind.” The explanation everyone reaches for is the obvious one: these are great companies. Huge profits, rapid growth — they earned it.

That’s probably part of the truth. But it leaves out a second force, one that has nothing to do with whether the companies are any good. It’s the mechanical passive bid that’s wired by policy into the way most people now invest. And the strongest part of the case — the part most people miss — is that we can actually *test* the obvious explanations against it. Twice, the world changed the conditions for us. Both times, the “they earned it” story predicted one thing, and the opposite happened.

Let me build it from the ground up.

The Passive Bid

Roughly half of all the money in U.S. stocks is now “passive.” It isn’t run by a person picking winners. It’s run by a rule, and the most common rule is: “Own every company in the index, in proportion to how big it already is.”

So if one giant is 7% of the market and some smaller firm is 0.01%, then every dollar flowing into an index fund buys 7 cents of the giant and a hundredth of a penny of the small one. Nobody chooses this stock by stock, it’s rules-based. Occasionally, like last week, the rules are changed. But most of the time, the rule chooses. The biggest companies automatically collect the biggest share of every incoming dollar. When that buying pushes a big stock up, the company becomes an even *larger* slice of the index — so the *next* dollar buys even more of it, which pushes it up again.

It’s a loop: price up → bigger share of the index → more of the next dollar flows in → price up. The rule rewards bigness with more buying, and the buying creates more bigness. No one is steering. It’s a machine following instructions — and when half the market is wired to that machine, it becomes one of the largest buyers in the room, every single day.

The free test that separates “great companies” from “the machine”

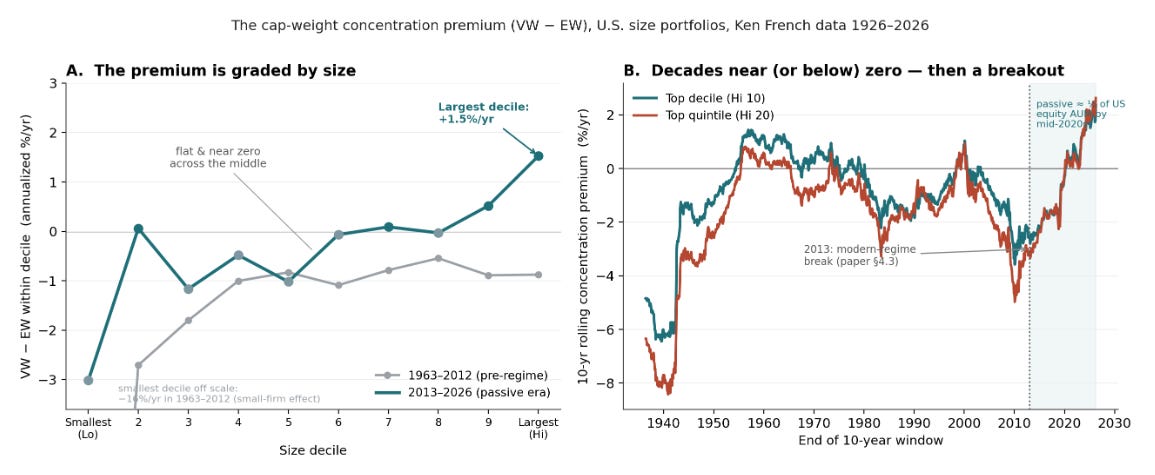

“Big won” compares big companies to small companies. Of course, the big ones did better — they’re big. That tells you nothing about “why.” So do something smarter. Take the same group of giant companies and build two versions of a portfolio from them. In the first, you put more money in the bigger ones — that’s the index rule. In the second, you split your money evenly across all of them. The exact same companies. The only difference is how you weight them.

If these are simply wonderful businesses that earned their gains, both versions should do about equally well — after all, they hold the identical stocks. But that’s not what happens. The version that weights by size has steadily pulled ahead of the version that weights everyone equally over the last 15 years. That gap means the very biggest are outrunning the “merely-big” — not because they’re better businesses than their neighbors, but specifically because of the act of weighting by size.

The size-weighting itself is producing the return. The circularity is the point.

Two more clues confirm it. The effect is strongest in the very largest stocks, weaker in the mid-sized, and basically absent in the smaller ones (excluding microcaps). That’s the exact shape you’d expect if mechanical index buying were the cause, since that buying piles onto the biggest names and barely touches the rest. And the timing lines up: for most of market history, this gap was roughly zero; it exploded right as passive investing took over.

Two obvious objections — and how the world tested them for us

You can’t run a controlled experiment on the entire stock market. But the next best thing happened twice. The two natural “fundamental” explanations each make a clear prediction, and reality ran both tests.

Objection 1: “It’s just low interest rates.”

When interest rates are near zero, money you’ll receive far in the future is worth a lot today — which makes “growth” stocks, whose biggest payoffs are years away, look more valuable. So the story goes: rates were near zero, which inflated the tech giants, end of story.

It’s a testable prediction: if low rates were the cause, then high rates should deflate these stocks — and the tech giants most of all.

Rates rose to their highest level in about twenty years and stayed there through 2023 and 2025. If the low-rate story were right, the giants should have sagged. Instead, those were the strongest years of the whole effect — the size-weighting gap hit record highs precisely while rates were highest. The supposed cause went into full reverse, and the effect got stronger. It’s like insisting a room is hot because the heater’s on, then watching someone shut the heater off and crank the air conditioning — and the room gets hotter. At that point, you realize the heater wasn’t your answer.

Objection 2: “The giants just earned it — incredible cash flows.”

This one sounds airtight until you look at what these companies were actually doing with their money. Picture two lemonade stands earning the same profit. One pockets its profit. The other is forced, year after year, to spend most of its profit on new equipment just to keep up with rivals — and the equipment wears out fast. Which stand would you pay more to own? Obviously, the one who keeps more cash. The forced spender’s spending isn’t a jackpot; it’s just the cost of staying in the game.

That’s exactly the situation the giants walked into. To compete in artificial intelligence, they were forced to pour staggering sums into data centers and chips — equipment that goes obsolete in a few years, with payoffs nobody can yet measure. As a result, the cash actually left over for their owners (free cash flow) grew far more slowly than their reported profits did, because the building costs ate it up.

Standard valuation says spending more only makes a stock more valuable if that spending earns attractive returns. Forced, defensive, fast-aging spending is the opposite of a spectacular-return opportunity — so the textbook prediction is that investors should have paid less for each dollar of these companies’ profits, not more. The opposite happened. The “they earned it” story doesn’t merely fail to explain the re-rating; it predicts the opposite sign.

So both obvious explanations were handed clean tests by events, and both got the direction wrong. That’s a lot stronger than a hunch. The only fundamental escape left is pure faith — “the AI spending will pay off enormously someday” — which may be true, but is a bet on an unknowable future, and it still wouldn’t explain why the effect is neatly graded by company size. The mechanical story explains all of it without a single leap of faith.

Why it doesn’t just fade away

Normally, a price that’s been pushed too high drifts back toward fair value. So why doesn’t this?

Think of pushing someone on a swing. One push sends them up, then they coast back down — the push fades. Unless you keep pushing in rhythm. Then they stay high, not because any single push lasts, but because the next push arrives before the last one dies.

That’s what continuous index buying does to the giants. Each day’s buying gives them a push. That push would fade — but tomorrow’s buying re-energizes it. As long as money keeps flowing in, elevated prices are kept artificially high. This is why the effect doesn’t quietly correct itself. It isn’t waiting to fall — it’s being propped up, continuously, by a pump that runs every trading day.

Why nobody competes it away

Here’s the genuinely strange part, and it’s what makes this different from every market factor you’ve heard of.

Usually, when there’s an easy way to make money in markets, people notice, pile in, and ruin it for everyone — the opportunity gets competed away. A crowd rushing to a sale empties the shelves. That’s the normal rule.

This one runs backward. The “crowd” here isn’t clever traders chasing a profit. It’s index money on autopilot. It isn’t betting on these stocks; it’s following the rule, and it can’t choose to stop. So when more money joins the passive crowd, it doesn’t compete the effect away — it makes the effect stronger, because there’s now even more mechanical buying flowing to the biggest names.

It’s not a crowd at a sale. It’s a conveyor belt that speeds up the more you load onto it. That single property — gets stronger the more crowded it gets — is what lets this keep running when normal opportunities would have died.

What happened to momentum?

Quick heads-up: this part is a bit more technical than the rest. If it gets dense, skip to the last line — that’s the whole point.

For decades, one of the most dependable patterns in markets was called momentum: stocks that had been rising tended to keep rising, so you bought the recent winners and bet against the recent losers. It worked so reliably for so long that it became a standard strategy, with billions of dollars behind it. Then, over the last several years, it broke down — by the standards of its own long history, the strategy has had one of its worst stretches on record.

The obvious conclusion is that “winners keep winning” simply stopped being true. But it didn’t disappear. It moved.

The classic strategy is a comparison: rank every stock against all the others and bet on the relative winners. That’s an easy recipe to copy, so everyone piled in — and as we’ve already seen, anything a crowd chases gets competed away. Momentum became the textbook case: so many people ran the same playbook that they bid away the very edge they were chasing.

But there’s a second flavor of “winners keep winning” — not a stock beating its peers, but a single stock’s own move carrying forward: it rises one month, and that alone makes it a little more likely to rise the next, on its own steam. (The technical word is autocorrelation — a stock’s move echoing itself.) That flavor hasn’t faded. It’s gotten stronger — in exactly one place: the giant, flow-fed stocks at the top. Why there? Because that’s where the machine’s continuous buying lives, relentlessly pushing the same handful of names so their moves echo forward instead of dying out. And this version can’t be competed away, because betting against it means betting against the flow — and we’ve already seen how that fight ends.

So momentum didn’t die. The version traders could crowd into died; the version the machine powers quietly took its place. It’s the whole essay in one line: *the part you can compete away fades, and the part the machine drives wins.*

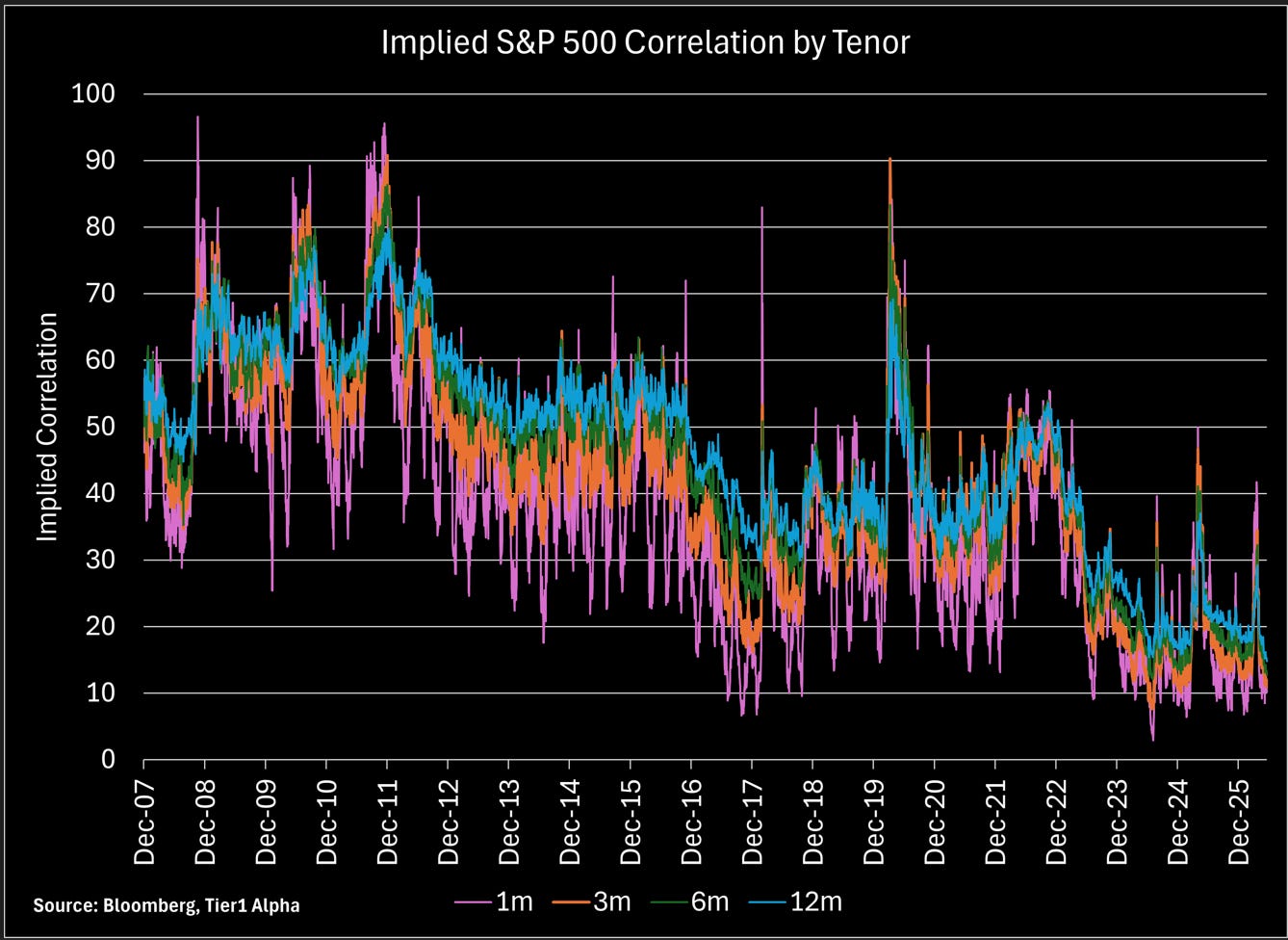

The correlation paradox

Here’s a fresh clue, and it’s one almost everyone reads backwards.

Lately, individual stocks have stopped moving together. The degree to which they rise and fall as a herd — what analysts call correlation — has, by some measures, dropped to lows not seen since before the 2008 financial crisis. Each stock seems to be marching to its own drummer.

The flattering read is that the market has gotten smart again: investors finally judging each company on its merits, a “stock picker’s market,” proof that careful analysis is back and the market is healthy. It’s almost exactly backwards — and unwinding why reveals a second machine sitting right next to the first.