Shall We Play a Game?

What can the bear market of 2022 tell us about likely market response in a Fed cutting cycle when markets are dominated by passive?

This will be a short note as I’m going off-grid with my oldest son this weekend. I love you all, but not as much as I love him.

After weeks of economic exuberance and theories of a broadening market rally, Friday’s jobs report brought us back to earth with a rebuttal to the endless commentary that “there’s simply no signs of a recession.” These commentators mean other than rising unemployment rates, deteriorating consumer confidence, warnings from consumer retailers, rapidly rising delinquencies, etc, there are no signs of recession. In other words, equities remained near all-time highs.

At a macro dinner on Wednesday night in NYC, I was reminded of how far I’ve deviated from my hedge fund brethren. “The market only cares about first release Non-farm payrolls — knowing the number is more important than the truth!” is a reasonable summary of the attitude that evening. Others reiterated the current refrain, “as long as the government keeps spending at these levels, we can’t have a crisis.” The problem with growing old and not yet senescent is that I remember the arguments in the other direction from 2006:

Now that 10 years are comfortably back below 4%, we are unsurprisingly hearing far fewer questions about “Who will buy the bonds?” despite the robust deficits. I continue to believe we will ultimately see 10y yields back below 2% as the world grapples with the realities of an aging population and slower global economic growth. While demand for goods and services is theoretically unlimited, the empirical reality remains — in a world of constraints, the best predictor of global aggregate demand remains population growth. With 2023 seeing the population of children worldwide turn negative for the first time since the early 2000s, it is very difficult for me to become particularly excited about projections for further growth acceleration.

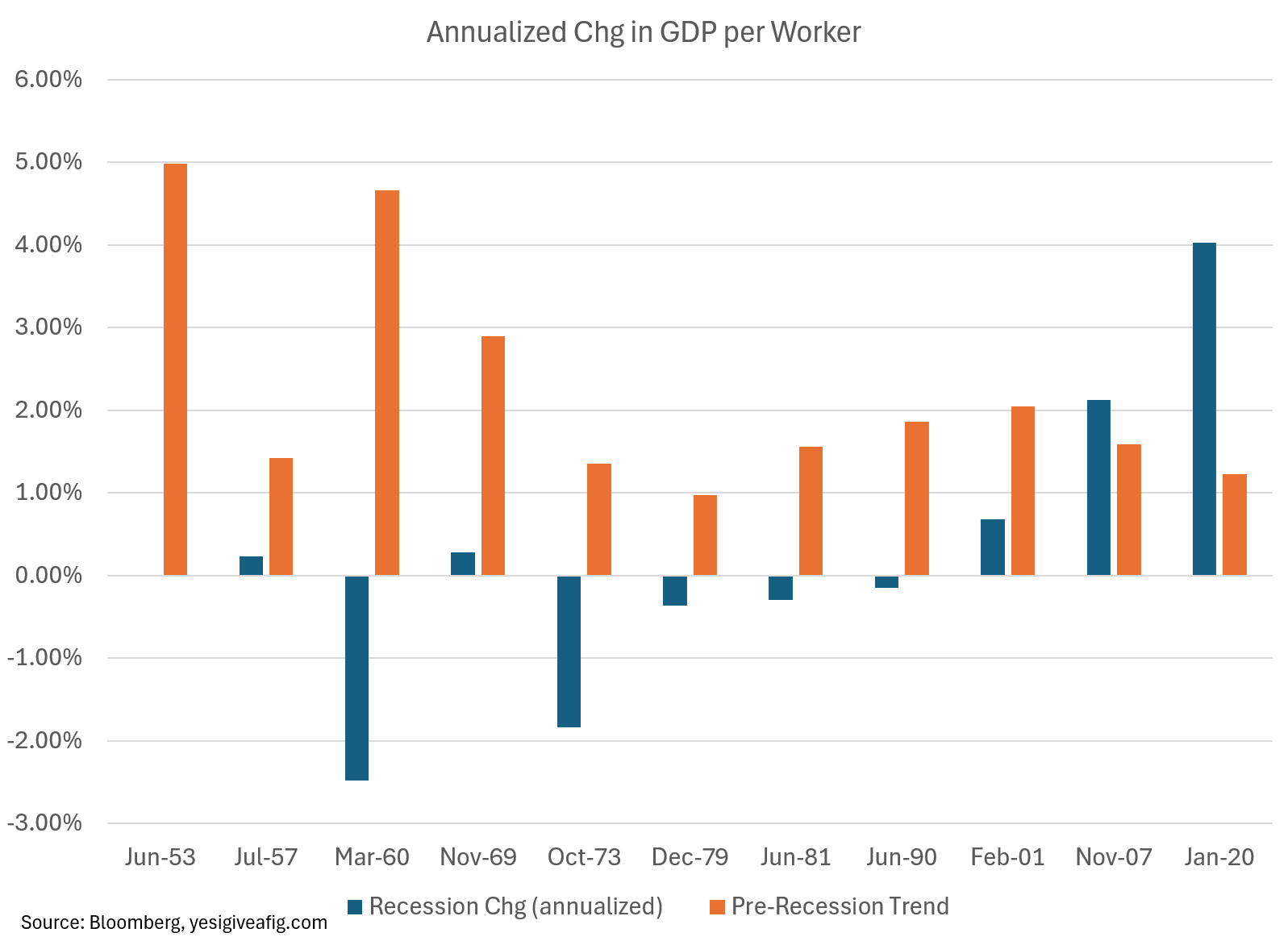

Will declining future worker populations raise real wages? Almost certainly. We’ll also figure out ways to use those worker populations more productively, which will lower real costs. On this front, rising labor productivity is one of the recent signs that we are in recession. Recessions prior to 1990 harmed productivity as firms retained employees while losing work; margins fell. The advent of the “jobless recovery” in 1990 presaged an era of productivity rising during recessions as firms ditched marginal employees and made existing workers work harder. While I applaud elements of this as a capitalist, we’re kidding ourselves if we think this is the way to build a functional society. The net result of a deteriorating corporate and social safety net? Falling fertility.

True to form, 2023 & 2024 have seen rebounds in productivity that many have attempted to hail as an “AI-driven renaissance.” This is untrue, although it may yet emerge. What we have so far is good old-fashioned “work harder to keep your job,” a classic recession indicator.

I remain somewhat agnostic on the MMT-driven theory of “no landing due to deficit.” The deficit of the public sector indeed becomes income for the private and foreign sectors. And with a deficit of 7% of GDP, that is a lot of income being injected.

However, there are so many voices that have joined the “With a fiscal deficit of 7%, we simply can’t have a recession” chorus that I’m increasingly skeptical. First, the deficit is not 7% — it’s now closer to 5%. Second, the US trade deficit consumes 3.2% of that fiscal deficit, transferring that income to the foreign sector. And finally, monetization DOES matter. A fiscal deficit funded by QE is one thing. A fully funded deficit, which requires X% of the private and foreign sector income received to be deferred in favor of earning interest, is simply not the same thing. And it’s the latter we are experiencing today.