Seems important...

Declining payroll growth continues and suggests the long-awaited recession is finally here.

Summary:

Private payroll data is showing concerning trends with downward revisions and misses, adding to skepticism about the reported job growth tied to new business formations as suggested by the Birth/Death model.

Historical patterns of corporate profits as a percentage of GDP indicate fluctuations with notable peaks and troughs, but recent records show an unprecedented rise to 12% in 2021, driven by a mix of organic growth and favorable tax and interest rates. This trend is in jeopardy.

Current trends suggest that the claimed improvements in net interest expenses for corporations are likely based on inaccurate data, with the largest companies such as AT&T beginning to feel the pressure of rising interest rates and very few companies benefitting from higher rates.

A Federal Reserve paper highlights that while smaller businesses initially benefited from stimulus, their margins are normalizing and turning lower, in contrast to the largest companies. This shift, along with slowing revenue growth, could signal challenging times ahead for corporate profits and expectations.

What I’m Reading Now

As highlighted in today’s note, I’d encourage reading the recent Fed Governor piece on corporate profit margins https://www.federalreserve.gov/econres/notes/feds-notes/corporate-profits-in-the-aftermath-of-covid-19-20230908.html

Top Comment

Spencer asks for clarification: “What S&P dividend rate in your mind reverses your thought process? Please correct me for my over generalization:

Right now is a good time to buy treasuries/CD to lock in the 5.5%ish rate. Short term

S&P goes through a correction, either the price drops significantly to account for the risk compared to the risk free rate, the dividend rises closer to the risk free rate, or rates drop.

MWG: Spencer, today’s note is largely on this topic. My expectation is that we’ll see a combination of the two and unfortunately rates rallied pretty sharply in the last week. The offset, of course, was the near record breaking equity rally. As you’ll see below, my expectation is that earnings and dividends will stagnate for an extended period of time and stocks will either correct sharply as investors reallocate to bonds or slowly as new money is allocated. The key risk for CDs and bills is the reinvestment risk.

The Main Event

I read the news today, oh boy…

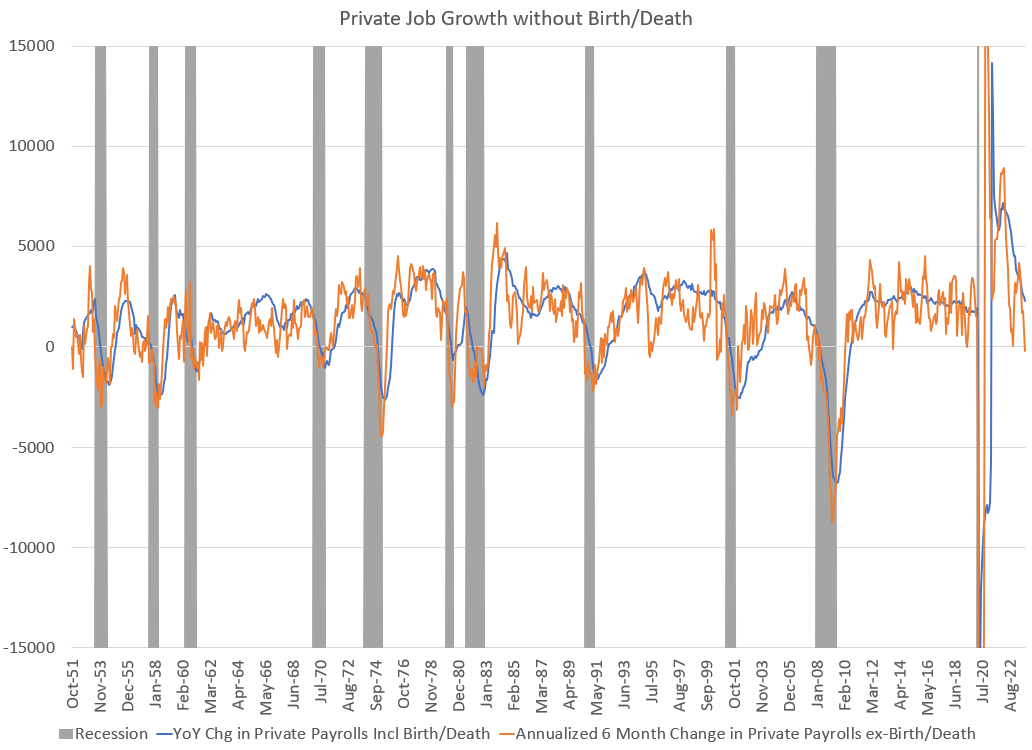

The private payroll data was not good, with both downward revisions and a general miss on what many dismiss as “strike-related” declines. Perhaps that’s right, but remember that we’ve seen a never-ending string of downward revisions that have now pulled private sector payrolls to the cusp of zero. Perhaps it bounces again, perhaps it doesn’t. I’m leaning towards “doesn’t.”

Regardless, we know the culprit — the infamous Birth/Death model which continues to suggest near record levels of job growth tied to new business formations:

As I’ve discussed ad nauseaum, “No, we are not enjoying a brand new surge in entrepreneurship.” The Birth/Death adjustments are now effectively the tool that prevents a recession from being announced. If we look at the pace of hiring, it’s obvious:

If we look at the six-month change in non-farm payrolls EX-birth/death it has turned negative. Can this happen without a recession? Of course. Is it likely? No.

So now let’s shift to a discussion of what’s likely to happen to corporate profits. A good place to start is with Warren Buffett’s 1999 classic:

As you can see, corporate profits as a percentage of GDP peaked in 1929, and then they tanked. The left-hand side of the chart, in fact, is filled with aberrations: not only the Depression, but also a wartime profits boom- sedated by the excess profits tax — and another boom after the war. But from 1951 on, the percentage settled down pretty much to a 4% to 6.5% range.

By 1981, though, the trend was headed toward the bottom of that band, and in 1982 profits tumbled to 3.5%. So at that point, investors were looking at two strong negatives: Profits were sub-par and interest rates were sky-high. — Warren Buffet, 1999

The accompanying chart was sobering, even if many dismissed it in the heady days of 1999… who could imagine corporate profits rising significantly as a fraction of GDP versus its nearly 100-year record? I heard Jeremy Grantham offer the exact same analysis in Feb 2000.

And yet, that’s exactly what happened. Corporate profits as a % of GDP hit a new record high of 12% in 2021, nearly 50% higher than the prior 1929 record!

In fact, whether we measure based on S&P corporate margins or the broader BEA data for the entire US non-corporate sector, the answer is the same — clearly Warren (and Jeremy and myself…) lacked imagination as margins have exploded relative to any prior period. Corporate profits after tax in 1999 were approximately 12.5% of gross-value added, that has now been nearly doubled to 22%. The driver of the change is about half “organic” — actual change in mix of companies and changing company fundamentals — and half tied to declining tax rates and interest rates.