Rinse, Warsh, Repeat

Make Regulators Great Again

I was unable to listen to Kevin Warsh’s opening meeting live. Fortunately, I had many friends to watch for me. Most were pleasantly surprised at the new Chair’s apparent restraint and emphasis on improving data quality. I will suspend my disdain for a bureaucrat introducing new “task forces” and wait to see what emerges. Danielle DiMartino Booth took Warsh with understandable skepticism, but highlighted that he is indeed right — “the data stinks.” She quotes Warsh:

“So even inside of official statistics I would be open-minded if the task force and our own best thinking had recommendations how those official statistics can be brought up to a standard of our time, using new analytic methods. I’d also say this: Almost every private company CEO that’s running his or her business is doing so with real-time information that isn’t subject to much revision that is telling them what just happened at that very moment. As you know, there are normal long and variable lags in the conduct of monetary policy. What we’re really interested in is what’s happening right now. What we’re less interested in is echoes of history. And you’re hearing from my answer that some of the data that we receive, that we’re waiting for on the first Friday after the month, the payroll index or something else, that might be an echo of history that’s quite useful on its THIRD revision. We need to take those error bounds down because we have to make hard decisions in real time.”

She notes:

“Did he say “THIRD” revision? Was Warsh speaking about the Quarterly Census of Employment and Wages, the QCEW last week’s Quill was devoted to in full?… For all his certitude, Warsh may not appreciate that he acknowledged he’s likely walking into a repeat of the 1980 episode (MWG note: double dip recession) with the critical caveat that he’s not battling Volcker’s inflation. The U.S. economy suffered – past tense – a recession in 2025’s first three quarters. As for what followed, for the record, the QCEW indicated an upward revision to the fourth quarter of 2025, which preceded a spike in announced mass layoffs in January of this year.”

Regular readers of YIGAF are well aware of my disagreements with the BLS-reported data and the Birth/Death methodology. More on that below. And while I share Warsh’s frustration with revised data, I’d argue he has a snowball’s chance in hell of getting the BLS to play ball. From my perspective, Warsh is just signaling that forward guidance is not the only thing ending. “Data dependent” is likely giving way to “Trump dependent.” And there’s no better man for the job. /s

A more favorable take was offered by Barry Knapp at Ironsides Macro in his piece, “Uncle Milty is Smiling”:

“We strongly support Chairman Warsh’s five task forces objectives, like Chairman Warsh our criticism of what Treasury Secretary Bessent calls ‘gain of function’ monetary policy began with the launch of QE2 in November 2010. Non-crisis long duration asset purchases (QE) and the abundant reserves regime were an overreaction to the deleveraging impaired growth following the financial crisis. The second order effects on the capital allocation process of the Fed’s expanded footprint are vastly underappreciated, particularly by the FOMC participants focused on volatility of repo rates. The wealth of the nation depends on returning the setting of the cost of capital to market participants, reducing the influence of FOMC participants.”

Now Barry is a friend; and friends don’t let friends drive drunk. So I’ll simply note that while I agree with the objective of “reducing the influence of FOMC participants,” it’s worth emphasizing that market participants have NEVER set the cost of capital.

Barry wants to cut the Fed's footprint so capital allocation returns to the market. Unfortunately, there's no market underneath to return to. Markets are the sum of policy choices: the QDIA default that pushes savings into equities at any price (and leads to many believing policy is still loose), the post-GFC capital rules that decide which borrowers banks fund, sanctions on Russia, and, of course, QE. Remove QE and you don't reveal a market price; you just let the other choices, including the failure to prosecute antitrust violations, dominate. “Reduce the FOMC's influence and return the cost of capital to market participants” means, in plain terms, “let the bank-capital regime and the retirement-default rules set it instead.” That is not a market. It is a reassignment of which administrators are in charge, and Barry and Warsh do not appear to understand that the world does not work as Austrians would like to believe it does.

We do not have the choice to, as Grover Norquist once put it, “reduce the size of the government to the point that I can drown it in the bathtub.” Government is a perpetual state of any social species. It exists in households (“Mom wears the pants in the family”), it exists in firms (“Read the product objectives and get back to work,” as Lee Iaccoca allegedly told Pinto engineers), and it exists in every community of every size. You cannot be a nation of laws without the men (or machines [ominous background sounds]) to interpret and to enforce them. A decision to pare back one branch of government simply elevates the remaining branches. The choice is good governance or bad governance.

We now have the latter, but I cannot claim to understand it particularly well either. As my great friend, Harley Bassman, texted me this week:

“You need to stick with entertaining speeches about Passive… your Rate and War predictions are killing me!”

So…

Iran, I Saw, I Wrong

Or perhaps, “US ran”

The skeptics were right — “TACO” indeed. With higher inflation prints and gasoline prices now far above his “$2.30 a gallon in most states, and in some places, $1.99 a gallon" from the State of the Union, the decision was apparently made to “end the war with a victory.” The world jeered and Israel joined in. Admonishment followed:

Is Trump giving up too much? Absolutely. This is insane and cruel. The ultimate “negotiating with terrorists.” But make no mistake, they are doing it for ewe. Trump knew that resolving the US-Iran War was a requirement for surviving the midterms. So… “Victory!” After all, the people have short attention spans. You want to know why Neville Chamberlain “appeased” Hitler? Because 21% of the registered voters in the 1935 election that elevated Chamberlain were war veterans. Would have been 24% except 6% of adult male population, roughly 1/8th of those serving, never came home. Those who did come home didn’t want their children facing a similar fate.

We surrendered to Iran over 4% inflation. Millions of Iranians will likely die in the regime retribution. But they don’t vote in U.S. elections.

I want to be perfectly clear on this point. I supported the US attack on Iran. I did that with full knowledge that young men and women I know personally would be placed into harm’s way. I was well aware that gasoline prices would be higher and that the middle of our socioeconomic distribution would suffer disproportionately, both economically and emotionally, as they are the ones struggling to pay bills AND they are the ones whose children serve as enlisted in the US military. The middle 60% contributes over 70% of the fighting force.

The response of the Iranian regime — attacking neighbors, civilian infrastructure, and closing an international waterway should have been anticipated. Apparently, it was not. Radigan Carter’s conviction that the Iranians would “never surrender” was never even tested. Ground troops, which I expected to be deployed in limited numbers, were never deployed. Munitions were depleted, but reserves remain (somewhat adequate). What failed was not the capability of the military or the American people, but our leadership’s belief in our ability to be treated like adults.

And yes, this was a bit of black pill moment for me. Because we didn’t save American lives with this negotiation; we simply exposed the weakness of a nation that has record exposure to financial markets — both literally and through our potentate’s fixation on them.

“To allow the market mechanism to be the sole director of the fate of human beings and their natural environment... would result in the demolition of society.” — Karl Polanyi

I would suggest the most likely outcome is an escalation of the threat that China will move on Taiwan, and that the US will have fewer allies when it does. We’ve given a green light to Eco-terrorists (economic terrorists). And the world will again head into the flames. There is no peace from surrender.

And On Those Rates

My call for a reversal towards rate cuts, so far, has also been wrong, but less costly. The levered 2-year is down roughly 2.5% from March with the S&P500 up 15%. Long bonds are up roughly 2.5%. So wounded, but not a fatality. But interestingly, the equal weight S&P is up only 3.3%; the equal weight Russell 2000 only 2.8%.

The “passive factor” of 401K flows appears to have added about 2.5% as well, maintaining its annual pace of roughly 18% a year.

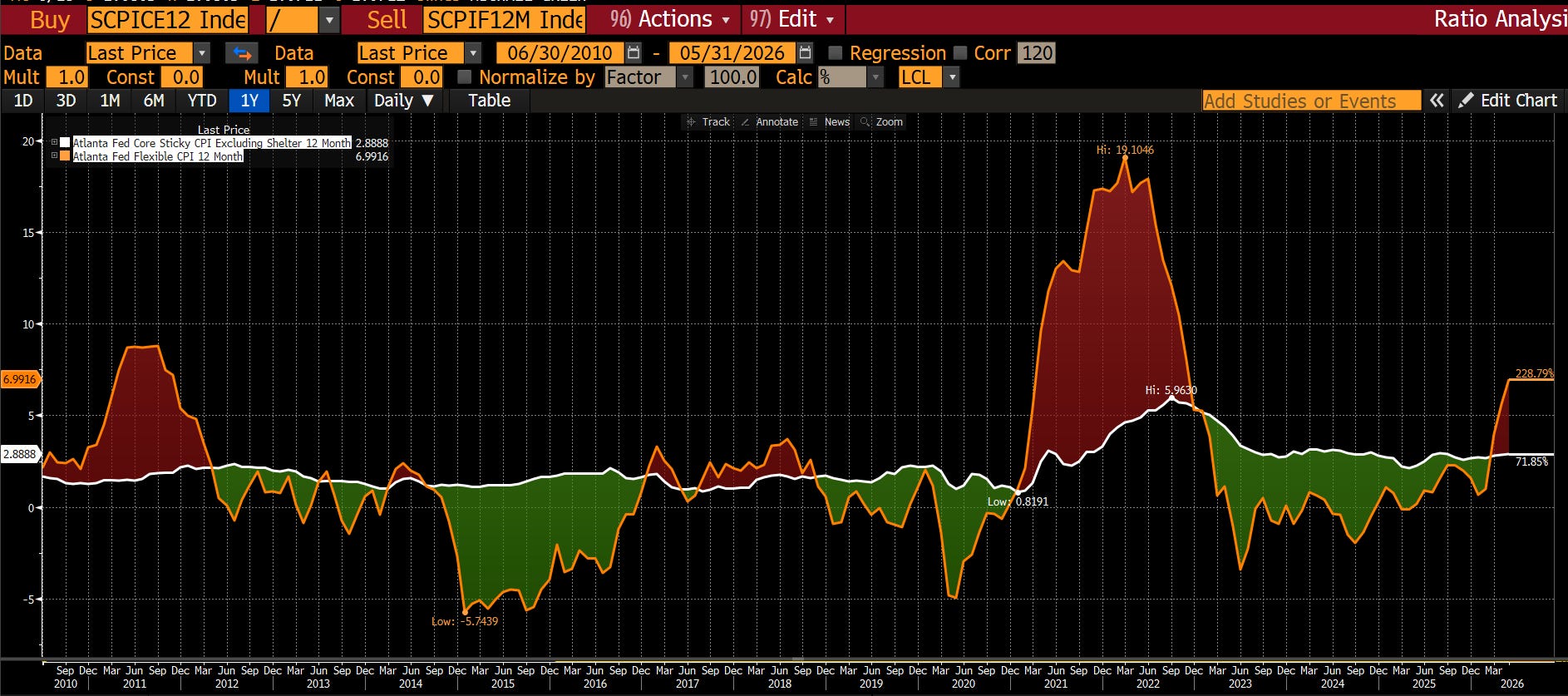

Meanwhile, headline inflation has soared with oil prices, but sticky inflation ex-shelter has remained largely quiescent:

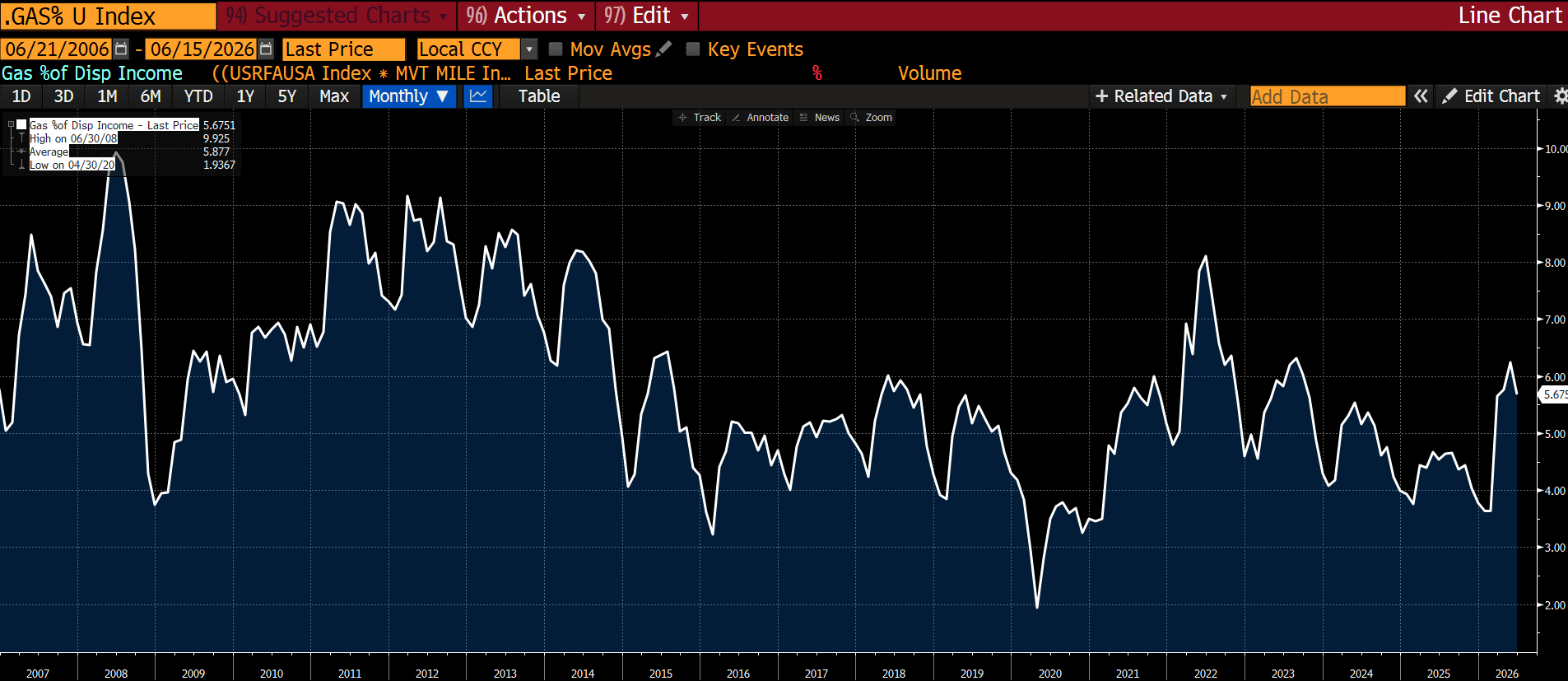

Yes, it remains above post-GFC levels at 2.9% per year, but unlike the immediate aftermath of Covid, it is not rising. And the surge in gasoline prices, now partially driven by seasonal changeover, appears to have peaked well below 2022 levels:

So I’m not buying this inflationary turn. And yes, I excluded housing for a reason.

Housing: frozen supply, not healthy demand

The housing market has been delivering pretty good news. Prices are stable, mortgage purchase applications are higher, as are existing home sales. Sure, it might be off a low base, but it’s positive, right?

The issue is that the housing narrative is on borrowed time. Let me explain.