Revisiting the Condundrum

One more try to explain "Inflation!"

Summary:

PCE Price Index and Inflation Commentary: The PCE price index for the year showed a deceleration in inflation, from a peak of 6.8% two years ago to 2.5% headline and 2.8% core year-over-year. High inflation was transitory and the aggressive monetary tightening was an overreaction with potential negative consequences for the economy. The declining inflation numbers become self-reinforcing as they allow the government to slow the pace of wage hikes.

Term Premium and Interest Rates: Term premium—the extra yield investors demand for holding longer-term bonds over a series of shorter-term bonds—highlights a disconnect between short-term rate hikes and long-term bond yields. Historical observations suggest that long-term rates often do not move in tandem with the Fed's short-term rate adjustments, implying that recent hikes might not have the intended effect on long-term investment decisions. This perspective raises questions about the effectiveness of rate hikes as a tool for controlling inflation.

Economic Impact of Rate Hikes: The aggressive rate hikes have coincided with various economic challenges, including bank failures, a downturn in real estate, and slower auto and home sales, suggesting a tight monetary policy may be contributing to economic stress. Despite these challenges, the stock market and certain asset prices have risen, which some interpret as a sign of enduring inflationary pressures. However, broader economic indicators suggest a complex interplay between monetary policy, inflation, and economic growth that suggests bonds are near fair value while short-term rates are simply too high.

What I’m reading now:

If you want to bend your mind, I’d encourage reading “Radical Hamilton: Economic Lessons from a Misunderstood Founder” by Christopher Parenti. The financial genius founder understood that “hard” money was not the solution and the obsession with “small government” reflects not a Hamiltonian sensibility, but rather the agrarian fantasies of Jefferson. Parenti lays out the case that Jefferson’s emasculation of Hamilton’s financial system set the stage for the decline of US sovereignty that culminated in the War of 1812. With the US having pursued similar policies, it is unsurprising that we have again industrialized and increasingly represent the Jeffersonian ideal — a divided nation of agricultural and raw material exports — even as our manufacturing “partner” increasingly threatens the global stage.

The Main Event

“I’ll say it again, raising rates was a TERRIBLE way to fight inflation. But we did it. And now we’ll get to pay the consequences for Jerome’s folly.” — Michael Green, aka “The Dumbest Man Alive”

Friday closed out a holiday-shortened week with the dropping of the PCE price index and a speech from Jerome Powell. What more could we ask for?

The PCE came in roughly inline with expectations at 2.5% YoY headline and a 2.8% YoY core. As a reminder, this number was 6.8% two years ago:

Now I personally find it hard to look at that chart and use anything other than the phrase “transitory” to describe the inflation experience. From the trough in April 2020 until the peak measured in June 2022 (remember Russia’s invasion of Ukraine?), inflation accelerated higher for 26 months. It has decelerated lower for the past 20 months. For an index that references 12 months prior, the up and down has been about as fast as physically possible without a 2008-style event. Just to help keep this in perspective:

But the PCE was not “clean” enough for many, and the complaints are surging from the “the Fed is trapped” crowd:

And off in the distance, we hear the thundering hooves of Paul Revere’s horse: “Term Premium! The Term Premium is coming!”

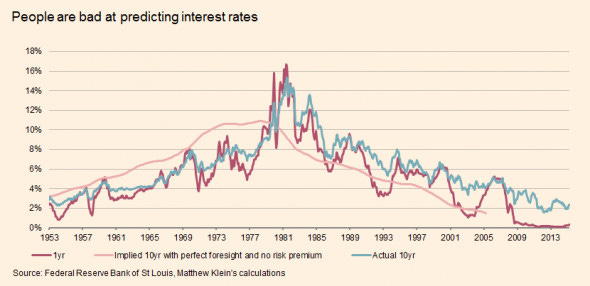

Term Premium is simply the compensation for the uncertainty in the path of interest rates. If I buy a 10yr bond, I have foregone the optionality to buy a series of short-dated bonds in sequence: ten one-year bonds, five 2-year bonds, two 5-year bonds, 40 3-month bonds… and so on. The disconnect between an aggressive short-term hiking cycle and changes in 10 year bonds was “first” identified by Alan Greenspan in 2005 as his hiking Fed Funds rates had no material impact on 10 year bonds. As we know, he hiked into inversion in June 2006:

Matthew Klein revisited this topic in 2015 as we approached the “watching paint dry” removal of accommodation by the Federal Reserve from Dec 2015 until Q4-2018. Klein noted that far from being a conundrum, 10 year bonds had spent the last 25 years overcompensating investors for the risk of being locked into a long-term bond and experiencing a hiking cycle:

Once again, long-term interest rates were largely unaffected by the hiking cycle, initially falling on China weakness and then recovering. While the Fed hiked from zero to 150bps, the 10-year bond was sanguine. As the Fed pressed higher, the 10-year sold off initially and then began to rally hard as financial markets began to collapse under the combined weight of 401K outflows and safe asset shortfalls. Q4-2018, the Fed “paused” and by Q3-2019, with the yield curve deeply inverted from a bull flattening, the Fed began to cut. Newly sensitive to market data, they paused the cuts in Q4-2019 as the yield curve uninverted… and then Covid.

By the time the Fed began hiking in Q1-2022, the 10yr yield had already sold off from 53bps to 180bps and approximately 40% of the ultimate losses in bonds had already been realized. By July 2022, my models suggested the Fed was already in restrictive territory and that inflation had both peaked AND the Fed was overtightening. This was the source of the “It’s time to stop” quote in my “Bringing Out the Inner Volcker” piece from July 2022. Real interest rates had turned positive already and were in line with post-GFC averages, consistent with the available research that “real interest rates tended to FALL post pandemics. Obviously, Mr. Powell did not listen.

Now the logical conclusion is that those concerns were simply misplaced. Since the Fed hiked interest rates an additional 300bps, clearly the need was for higher rates. After all nothing has broken, except:

Five major bank failures

Commercial Real Estate collapse

Auto sales “stabilizing”25% below levels from 2000 with inventory building rapidly

Home sales are down 40% on a population-adjusted basis (inventory building as well)

Marginally employed and unemployed up by 1MM people

Full-time employment flat for almost two years

Native-born US employment down 1MM

And for what it’s worth, the median stock is down 4%

On the flip side, the S&P500 is up $10T in market cap against a real GDP increase of $1T and US government debt outstanding is up $3T (half of which is tied to increased interest expense), so all must be well. “Inflation!” has rebounded (more later) so the Fed is clearly delusional in wanting to cut in 2024. At least there’s “no rush” to cut rates. According to the BLS establishment survey, hiring is robust.

There is no conundrum, unfortunately. What the markets are pricing is the eventual realization that the Fed has made yet another error and raised rates far too high (at the front end). 10 year bonds are “fine”, but likely represent something close to “fair value.” On my math, the “right” price is probably 3-4%, which represents 2-3% inflation premium and 0-1% real rates, and a normalization of 1% realized term premium over time. From these levels, even if I’m “wrong” and the realized term premium is going to be 1%, the immediate hit to 10yr bonds is roughly a 5% mark-to-market hit. Even on a return to the lowest realized Term Premium in history (1970s), mark-to-market losses are less than 20%. On the flipside, if the 10yr is “right” and Powell has hiked rates higher than appropriate, there is real risk that the damage to the economy is another “settling” at a new lower equilibrium where the high cost of servicing government debt further lowers our productive capacity. This is the Lacy Hunt/David Hume: “when a state has mortgaged all of its future revenues, the state by necessity lapses into tranquility, languor, and impotence.”

But clearly this cannot be the case, because, you know, bitcoin, gold and equities! According to the BLS, employment surged in 2024 (even as household surveys suggest it has fallen). Inflation must be resurgent! So let’s pivot and examine that case.

From high levels post-pandemic, goods consumption continues to fall as a percentage of total consumption, while services consumption has now “normalized” to its pre-Covid trend.

The low in services consumption relative to goods occurred back in March 2021 — when we were hitting the peak of the “we’re all going to be working from home forever so renovate it into a palace.” Flush with pandemic checks, there was money to spend but no workers to hire. As a result, prices were high, DIY was in vogue, and services consumption was low. Dining out at a restaurant or heading out for a hotel vacation was a rare treat.

With the return growth in services demand, we are hearing more narratives of “sticky” inflation and a hypothesis that the Fed has decided to start cutting rates “without the job done.” After all, 2.5% is NOT 2% (and definitely not 1.5% like pre-Covid), and long and variable lags only work on the topside… (sarcasm). Since services costs are largely driven by labor, it’s obvious that 5% wage growth is inconsistent with inflation returning to 2%. “Irresponsible dovishness” rules the day!

Except there is little to no evidence that any of this is true. The SF Federal Reserve examined exactly this theory in 2015 and found it wanting: