ProcrastiNation -- What's Gone Wrong With Productivity?

Some intriguing new work on total factor productivity may help to explain why it feels like we're making less progress

In the aftermath of the Global Financial Crisis, it was tough to ignore the apparent slowdown in global growth rates. Academics offered many takes, all of which converged on the idea of permanently slower growth.

In 2012, Robert Gordon hypothesized that the problem was not demand but rather supply — driven by deteriorating demographics, education, inequality, and government debt. As a result, he forecasted that real growth would slow to a rate of 0.9% annually from 2007 to 2032. Eight years later, it’s been a remarkably accurate forecast, with per capita growth at 0.91% annualized, less than half the growth rate from the prior 50 years. It can be found here if you’d like to watch a video version.

That he correctly forecasted from the pre-2007 peak to a post-Covid possible peak suggests that the rising inflationary pressures that began well before the post-Covid brouhaha were evidence of an economy that was already growing above potential. In other words, the low-interest rate/Trump tax cut-fueled economy was already running too hot, and a reckoning was inevitable. The outrageous decision to shut the global economy and then pump stimulus to consumers stuck at home had predictable (although not desirable) impacts:

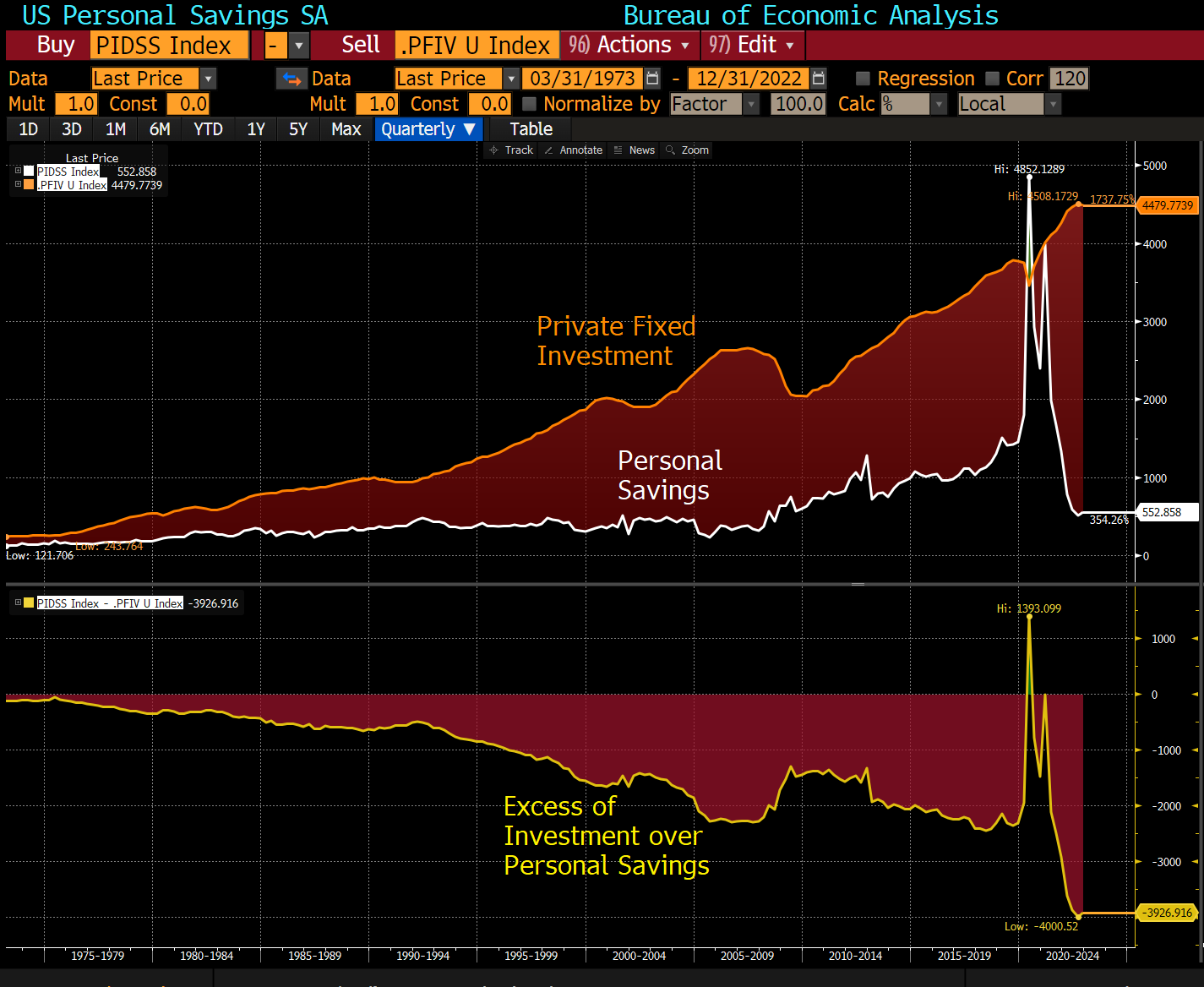

In 2014, Larry Summers joined the crowd, reintroducing Alvin Hansen’s “Secular Stagnation” concept from 1937 and stating that there was “a strong possibility that the Wicksellian natural rate of interest is negative and that, at any non-negative interest rate, saving will exceed investment leading to stagnation.” Unfortunately, this forecast has worked out less well:

Now obviously, investment must be funded by savings under accounting rules, so the reality that these are increasingly mismatched necessitates an alternate source of “savings”; in this cycle, those investment funds were provided by a combination of domestic credit growth, government deficits, and trade financing from creditor nations (looking at you, China and Germany). That all of this was facilitated by central banks has been well documented.

The failure of Summers’ Wicksellian forecast has not dimmed his propensity for predictions and prognostication. Remarkably, he has seamlessly moved from believing that negative real interest rates were the base case to an idea that we must pursue high real interest rates and that the Fed is too lax in its attempts to reign in inflation.

“Former Treasury Secretary Larry Summers said the Federal Reserve will likely need to raise interest rates more than the market anticipates as prices remain high but grew at slower rates in October.

Summers told Bloomberg Television’s “Wall Street Week” with David Westin that the economy has a “long way to go” before inflation is under control.

“My sense is that inflation is going to be a little more sustained than what people are looking for,” he said.

Summers can draw obvious comfort from Lord Keynes's apocryphal quote, “When the facts change, I change my mind,” but I’d prefer to place his approach into the Hickson proverb:

“If at first you don’t succeed, try, try, try again”

These debates essentially boil down to “total factor productivity.” Total Factor Productivity (TFP) measures the efficiency with which an economy combines inputs such as labor, capital, and technology to produce output. It is a crucial component of economic growth and a key indicator of an economy’s competitiveness. Importantly, TFP is the residual component of output growth that cannot be explained by increases in inputs and is often used to capture the impact of technological progress, organizational changes, and other factors that improve production efficiency. Gordon’s model suggests that a combination of the slowing pace of input growth, especially labor, and a deterioration in TFP is behind the slower growth.

Unfortunately, Robert Gordon passed away in 2018, so we can’t ask him if he too would have changed his mind, but a relatively new paper by Thomas Phillipon has provided further evidence that it’s the supply side, rather than the demand side, that has restricted growth. Phillipon’s paper builds on, oddly without referencing, the work of Ole Peters, whom I’ve previously extolled. However, unlike Gordon (and precisely like Peters), Phillipon takes issue with the analysis of the historical data series noting that there is no evidence that the compounding nature of growth exists. Instead, the evidence is that growth is additive:

In English, this means that income growth per capita is not growing at a constant rate but rather by a nearly constant amount. Graphically, this can be seen by those mathematically inclined in the following chart from Phillipon’s paper. On the left is the additive model; on the right the exponential (log-linear) model. Under this framing, the “Great Moderation” is simply a function of absolute levels of income having reached high enough levels that growth variability declines rather than the brilliance of politicians and political appointees in smoothing the path:

This has enormous societal implications, because, under an additive model, changes in income share suggest how we choose to share the pie matters more than the absolute growth rate. It also indicates that there is little evidence of a growth slowdown but rather a series of accelerations in the additive rate of growth occurring at definable periods in time. Interestingly, Hansen’s/Summers’ invocation of secular stagnation appear to occur when the distribution of wealth and income becomes a more critical talking point than historically, even as no evidence of their actual hypothesis appears to exist. Another paper, this one in 2021 by Katarzyna Schmidt-Jessa, compares Google trends on terms of economic and social mood and finds that while there is no evidence that we are building our models around secular stagnation, the evidence of slowing growth shows up clearly in mood. Interestingly, the authors hypothesize that these “animal spirits” may be inhibiting growth. In contrast, Peters/Phillipon suggest that the growth rate has not changed, and instead, the issue can largely be framed in the distribution of growth, which would be expected to manifest in population-wide data surveys:

Now we’re starting to unify several threads. The work of Peters and Phillipon would suggest that the societal problems we’re experiencing are increasingly a function of the scarce growth being allocated disproportionately to a subset of society, while the inflationary conditions we experienced in 2021-2022 were a function of a brief experiment at reallocating income to the income constrained subsegments of society. The price increases we experienced during that experiment match well with another feature embedded in the Hansen (but not Summers) hypothesis — the role of monopoly/oligopoly:

“Hansen approached macroeconomics as an institutionalist, rooted in the idea that markets were not necessarily competitive, and that many prices were likely to be set oligopolistically by large corporations.” — CEPR, 2015

The Summers’ hypothesis that secular stagnation might require a negative real rate was not Hansen; instead it was an extension of Hansen by Lawrence Klein nearly a decade later as models of perfect competition began to take hold. It was simply unacceptable by 1947 to believe that oligopolistic corporations would be able to force price increases while failing to make adequate investments to meet the marginal demand. In the aftermath of WW2 and nearly five years of government-imposed price controls and rationing, this might have seemed reasonable; and yet here we are again:

We’re left with a conundrum. Do we embrace the model of Volcker (and apparently Summers 2022) and attempt to defeat inflation with the tools of monetary policy, or do we pivot in a manner that the work of Peters/Phillipon suggests and focus on investment that raises the increments of additive growth (e.g., generative AI like ChatGPT) while working to redistribute the benefits of additional growth in a manner that is more conducive to societal harmony?

I’d guess my readers know which way I’m leaning.

Comments are appreciated, as always!

TFP growth rate is falling towards zero or rising at an additive rate is not at all the same statement. Phillipon and Peters' point is a very different statement than Gordon's.

It would be better to promote productive investment that increases the supply of goods and services in a noninflationary manner, but the current political environment is an impediment. There is a strong push to switch to less efficient means of energy production to decrease carbon emissions. There is also a cultural and political segment that believes we must lower our consumption of goods and services to protect the environment. I believe these policies will increasingly lead to radical politics on the left and right of the political spectrum. On the bright side, labor shortages might help to redirect the benefits of growth more equitably, and technological and scientific advances might help us out of this quagmire.