Please Don't Squeeze the High Yield

Mr. Whipple gets a soft landing, not us

Important!

This coming week on September 26th, Simplify will be hosting and streaming their third annual Entering The Fall (ETF) conference from 10 am - 4:30 pm at the NYSE. This year, I’ll be hosting fireside chats with credit investing legend Boaz Weinstein of Saba Capital, a macro discussion with Danielle DiMartino Booth, Chief Strategist at QI Research, and a geopolitical discussion with Jonathan Ward, author of “China’s Vision of Victory,” John O’Connor, creator of the Whitney U.S. Critical Technologies Index, and Perth Tolle, creator of the Freedom 100 Index. Free registration for the event can be found here.

This event benefits Coney Island Prep, a public charter school serving the heavily immigrant Brighton Beach area of New York City. Beginning with a single 6th grade class in 2009, CI Prep has expanded to become a K-12 shining star in the NYC education arena. With a rigorous expectations-based approach, CI Prep’s four schools have risen to the top of charter school rankings, despite being penalized in the rankings for a lack of organized sports! Jen and I have been active supporters of CI Prep for over a decade.

As in prior years, I will be matching donations to the event. You can access the donation page here. Please give if you can.

Summary

The historical trend of declining real interest rates is unbroken and does not suggest there was anything particularly unusual about the post-GFC period.

Recent increases in interest rates are likely a temporary phase rather than a return to a "normalization" of higher rates from the late 20th century. The rise has been driven by Central Banks' policy-driven actions rather than fundamental inflationary pressures.

Growing risk of refinancing, especially in the high-yield sector as higher risk-free rates can lead to unaffordable refinancing rates for private sector borrowers, is key. There has been a notable shortening in the maturity profile of the high yield index.

The market seems incapable of digesting the financial vulnerability of companies like Verizon with large debts due, suggesting a crisis if interest rates remain high. Like 2005, the risks of fallen angels is key.

Top Comment

Zach chimes in: When I saw the FT article on Friday highlighting the NAV loan for Vista my first thought was I hope Mike comments on this. You did not disappoint. When I shared it with my sales team the response was... crickets... and one of the products we sell is PE! Working at a reputable asset manager and selling and talking to advisors at the largest and most respected wealth management shops, it saddens me but no longer surprises me to see how little actual thought, care, and analysis/due diligence goes into investment selection. It is all 1-5 year historical returns. Reading about NAV loans, I was pretty startled and couldn't help but think of subprime mortgages being packaged in with the good to create an "investment grade" product. Post blow up I expect tighter private market regulation but I hope they at least start with "no buying into the same company that a previous vintage owns." With state pensions buying this crap hand over fist I'm sure Congress will see it as vital that they don't fail and the solution will be PE bailouts aka private gains, socialized losses. And the bifurcation of the US continues...

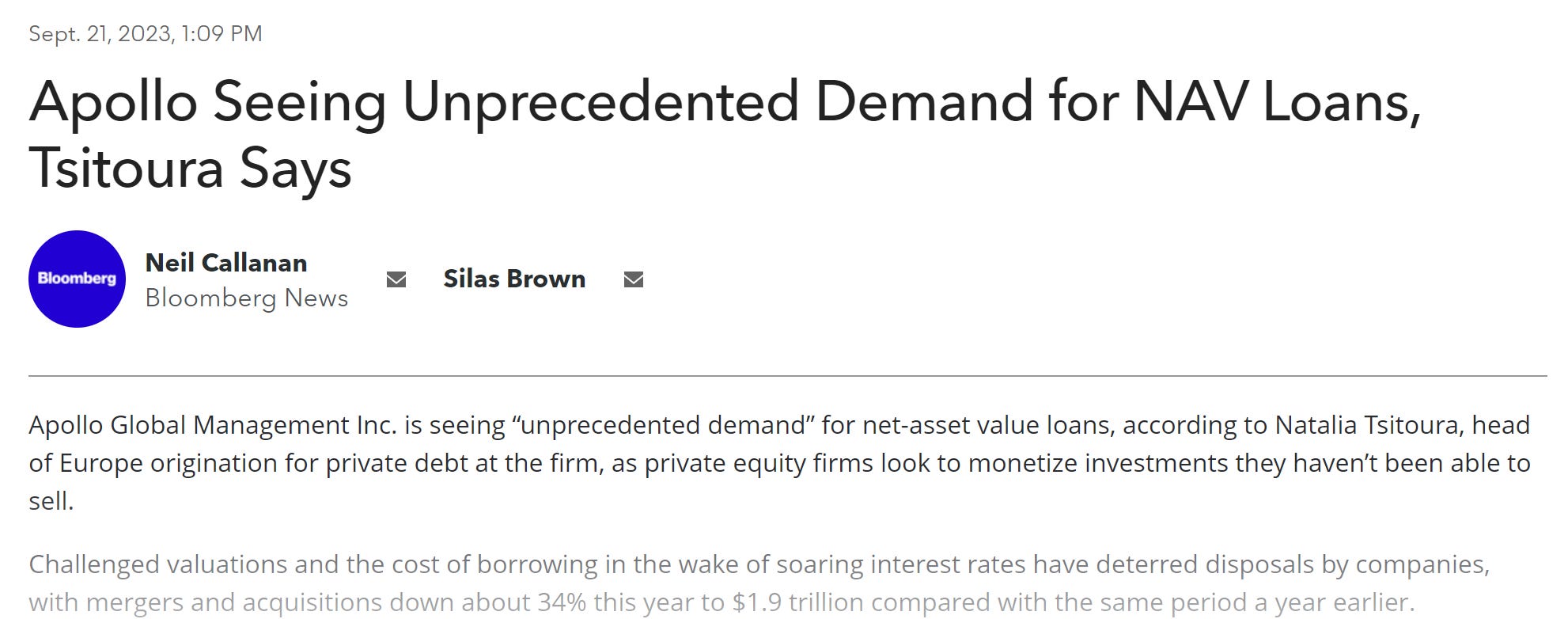

MWG: We aim to please, Zach! I’d note that since publishing last week, NAV loans are all over the news. Unsurprisingly, Apollo announced they see “unprecedented demand” for NAV loans this past week. I don’t know about you, but when I see “challenged valuations” and rising cost of borrowing, my immediate thought is “lever it up, baby!”

The Main Event

My friend Mike Kao (@urbankaoboy) posted a tweet on Friday that fit perfectly with the topics we’ve been covering on bonds:

To me, the remarkable part of this chart is not the current period of low interest rates, but the general willingness to accept that the interest rates of the late 1970s and 1980s were somehow a “natural” level while the interest rates post-GFC were the aberration. When looked at globally, over a long period of time, the trend in real interest rates has been perpetually lower since the break in the series associated with the Black Death. The Black Death, coming on the heels of the capital-intensive Crusades (similar periods of rising real rates can be found during the World Wars of Napoleon, WW1 and WW2), meaningfully alleviated Middle Period population pressures and created a significant per capita surplus, underpinning the trend in rising living standards that has broadly persisted since then.

Interest rates are the price for the use of money. All else equal, a society on the brink of starvation has a very high cost of capital — preserving seed corn for tomorrow takes a back seat to staying alive today. A society with a substantial surplus has a low cost of capital — the risks of capital loss are not catastrophic, and there are many with the resources to temporarily reduce consumption (save) and provide resources to those with clever ideas. Executed well, those clever ideas produce an additional societal surplus, and even more resources are available. Rinse and repeat and you can understand easily how a trend towards lower real rates has emerged over the last 800 years. Note there is nothing exceptional on this chart about global interest rates as of 2021.

Now, of course, no one wants to hear this. With interest rates rising rapidly over the last 18 months, it becomes very easy to convince ourselves that something MUST be different and that the inevitable trend in interest rates is towards “normalization.” And there ARE reasons to believe this may be true. Political idiocy over the last three years has substantially reduced the global surplus. The fraction of the world’s population living in poverty has risen for the first time in decades:

I’d bet that the pangolins at the Wuhan wet market feel terrible about this, but they were unavailable for comment.

However, it’s important not to forget that the REASON interest rates are rising is not due to rising inflationary pressures, it’s due to Central Banks raising interest rates. This entire cycle has been characterized by a deep inversion that only occurs during POLICY-driven cycles — the Specie Circular-driven Panic of 1837 and subsequent policy-driven panics of 1847 and 1857, Paul Volcker’s “heroics” (read incompetence) in 1979-1982, and today’s Jerome Powell-driven “soft landing” policies. Good luck with that last one.

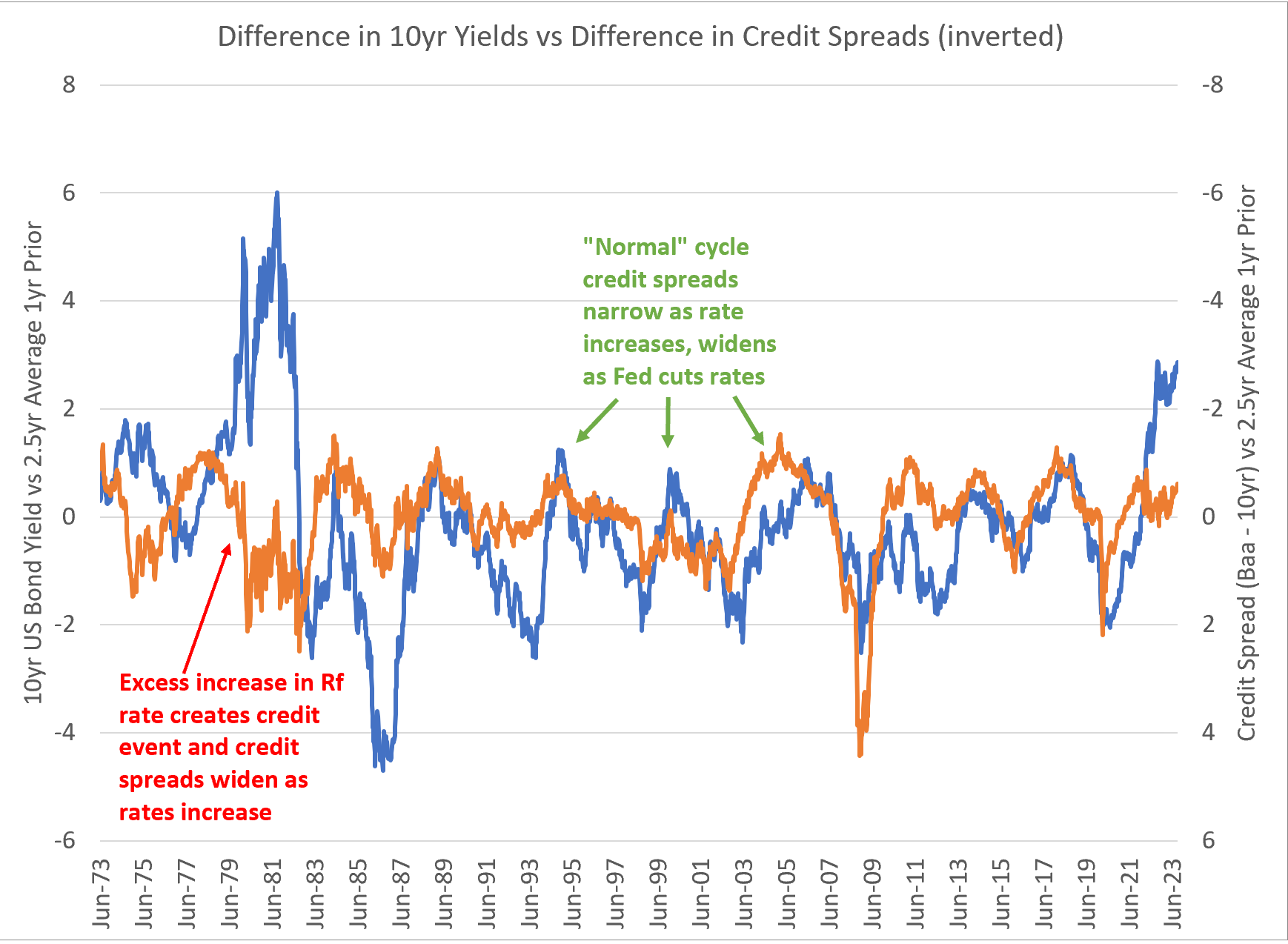

The speed and magnitude of this interest rate hiking cycle are nearly unprecedented. While I lack the detailed data to extend the data series prior to the early 1960s, the distinct nature of this cycle is only matched by the actions of the Fed in the late 1970s. The methodology here is worth a brief explanation. Because corporations refinance themselves at the risk-free rate + a credit spread, we care about both aspects when evaluating a credit refinancing cycle. In “normal” cycles, the Fed tightens monetary policy and demand for money for private sector usage falls as a cycle approaches maturity. In English, risk-free rates and credit spreads are almost perfectly inversely proportional unless central banks over-tighten: