No, David, No!

David Einhorn said the quiet part out loud.

I had planned another post, but then David Einhorn (hi, David!) broke the internet with a published interview by Barry Ritholz on Masters in Business, followed by an explosion of published articles and Twitter commentary from many who apparently failed to listen to the interview. To add insult to injury, my laptop is acting up so this writing has been a royal PIA (technical term) so no summary, top comment, etc. I’ve saved the other post and will release it next week. In the meantime, let’s talk about broken markets.

First, stop reading my drivel and listen to the podcast. It’s fantastic:

Second, understand what David is saying. He is not whining or complaining. In fact, knowing David, he’s the happiest I’ve seen him in years. He articulates a strategy that has allowed him to not only survive, but thrive in the current public markets. While many are bemoaning the valuation differential between small & large/growth & value, David has simply accepted that it is likely to persist and has therefore chosen only to buy companies that are perfectly happy to deliver the value he is seeking endogenously. If you want a 15% annualized return, you can:

Obtain it by buying a company at 10x P/E and a 5% dividend yield and hoping investors bid you to 11x P/E.

Obtain it by buying a company at 5x P/E with a 20% combined dividend and buyback yield and expecting other investors to sell it down to 4.75x P/E.

David notes that he has changed his methodology to the latter. Now, obviously, there aren’t that many companies out there with 5x P/E. But he’s certainly found some. For example Consol Energy, a producer of coal:

At Greenlight’s average cost of $33.54, although he mostly purchased in 2020 at well under $10/share, he paid less than 2.5x 2023 EPS. Over 2023, the company bought back roughly 15% of its outstanding shares. Is coal dead? Probably. But it’s going to be a slow and profitable death if we deplete the resource while not replacing it. And when the market bids up shares due to other active managers growing excited, he’ll sell some shares. If not? 15% buyback and 5% dividend works.

But that’s not what the market focused on. Instead we heard a chorus of whataboutisms:

The crazy part of this response is that it literally has nothing to do with David’s observation. He didn’t say, “NVDA is trading at 30x forward sales because passive.” He said, “Value is just not a consideration for most investment money that is out there.” That is an empirically true statement. There is no consideration of value in passive investing which now makes up more than 50% of managed equity assets.

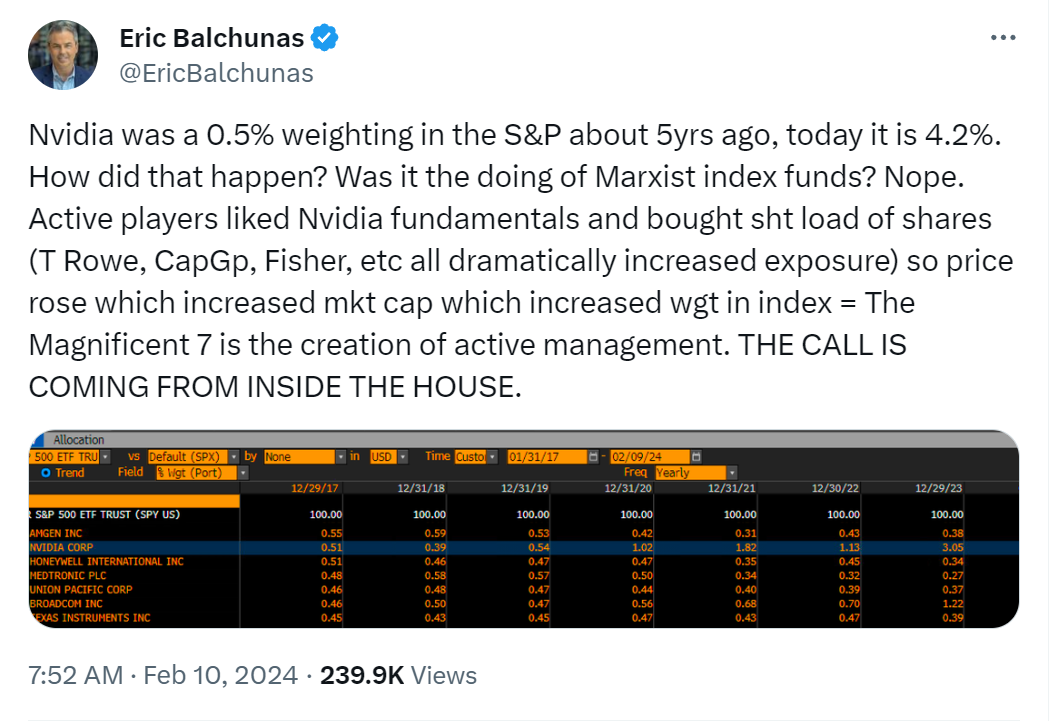

And yet interestingly, Eric has made an important point without realizing it. Active managers did indeed “bid up” NVDA as they “bought a sht load of shares.” How many shares were bought by the names Eric highlights over the past 5 years?

Hmmm… active managers “bid up” NVDA by buying 27MM shares, but passive managers had no impact buying 44MM shares. The math checks out.

Keep reading with a 7-day free trial

Subscribe to Yes, I give a fig... thoughts on markets from Michael Green to keep reading this post and get 7 days of free access to the full post archives.