Here Comes the Rent Again, Falling On Our Heads...

The excitement around a good inflation print has morphed into the long awaited bond rally

Summary:

Inflation Analysis and Federal Reserve Policy: The "transitory" nature of inflation was correct, backed by market-based metrics showing an average inflation rate of 2% for 2023. When measured using market-based prices (like those from Zillow or the Cleveland Fed), inflation rates have been much lower than reported and the Fed has overreacted with hikes.

Market Expectations and Rate Cuts: The market is starting to price in rate cuts, possibly influenced by Treasury Secretary Janet Yellen's fiscal strategies and the broader economic context. These rate cuts in 2024 are likely, both as a response to political pressures and as a corrective measure to the overestimated economic growth.

Labor Market Dynamics and Housing Market Implications: A shift from a white-collar hiring recession to rising unemployment in blue-collar jobs appears to have begun, despite high job opening levels.

Housing Market Analysis and Interest Rate Impact: Factors like population density, housing quality, and location relative to city centers have a more significant impact on housing prices than interest rates. The Federal Reserve's rate hikes were an ineffective strategy against inflation, with potential negative repercussions still to unfold.

Top Comment

In response to my nuclear rants, John Taylor offers:

I’m really glad to see people fighting for our futures once again.

I got excited about nuclear power as an undergrad in Mechanical Engineering, then went on to the Nuclear Navy. It seemed optimistic with 3 nuclear plants being built in the early Bush years.

Then the powers that be decided to sabotage all of those projects and destroy a significant part of our nuclear power infrastructure. It was very disheartening.

The fraud within the “Green” movements from wasteful spending to infrastructure sabotage to blatant environmental damage is simply frightening. It’s as if all of these agencies were infiltrated with enemy spies, like the Soviets used to attempt within our biggest labor unions.

Sentiment has markedly turned in most countries since the energy crisis in 2022, but our leaders are absolutely dragging their feet.

MWG: John, thanks for the feedback. I obviously agree (and thank you for your service in the Navy). This piece resonated with many and I am HOPEFUL that the narrative is beginning to change.

What I’m Reading Now:

This piece was inspired by a discussion I had with Dave Nadig and Tom Morgan on Twitter. It’s worth the read, IMHO. Tom highlighted a recent podcast discussion with Geoffrey West that I look forward to reviewing.

I’m also finally making my way through “The Myth of the Rational Market” by Justin Fox. A useful book that helps inform my own writing on passive dynamics.

The Main Event

The narrative machine is busy again. A “surprise” inflation print on November 14th, when the core CPI index came in at 311.365 vs expectations of 311.653, has supposedly cleared the path for the Fed to cut not once, not twice, but now four times in 2024. What was a “surprisingly low” level of long-term rates has now totally reversed. A reminder that long-term views on “structural” issues are a luxury in today’s market:

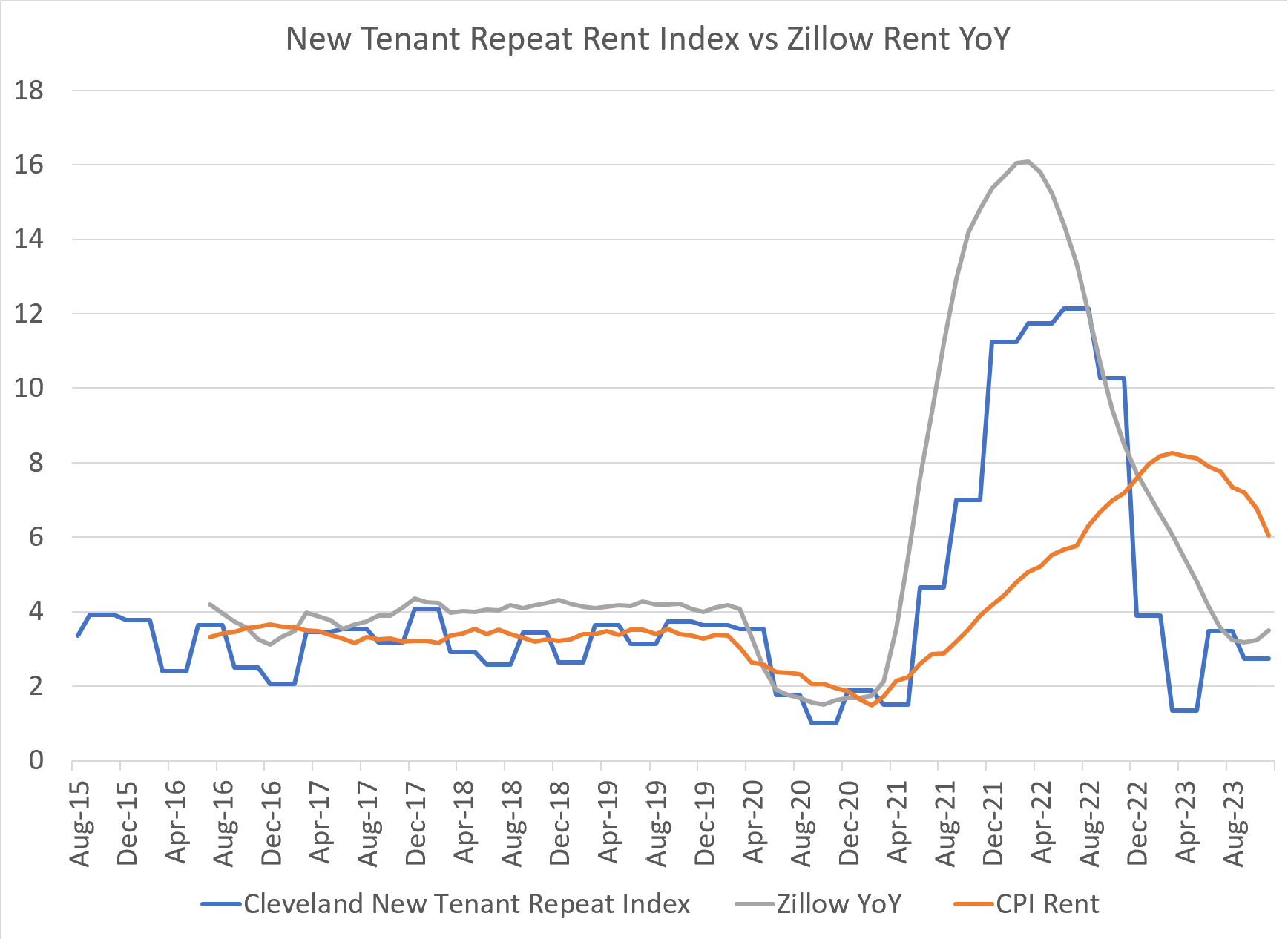

This is frustrating as it’s increasingly clear that the “transitory” inflation story WAS correct. On market-based metrics (you know, ACTUAL PRICES), we’ve averaged 2% for all of 2023. Note that even the Fed’s “market-based” metrics are corrupted as they include Owner’s Equivalent Rent for shelter:

“The PCE market-based price index excludes most imputed expenditures, such as “financial services furnished without payment,” for which deflators are implicit, based on independent current dollar and chained-dollar estimates. However, it includes “imputed rental of owner-occupied nonfarm housing,” which is deflated by the CPI for owner’s equivalent rent, so that the index will be comparable with the overall CPI. (Owner's equivalent rent within the CPI is measured by reweighting the renter sample of market transactions.)”

Fortunately, we can substitute market-based measures there as well to arrive at a “near right” answer. Zillow and the Cleveland Fed provide us with current market rent metrics by using “new tenant” indices. As you already know, this leads official rent metrics from the BLS by almost exactly one year:

And if we substitute the HIGHER of the two (Zillow), we get a picture that tells us clearly we continue to fight the last war. Since June 2022, inflation using market prices (again, actual transactions rather than imputed metrics) has averaged 1.74% annualized. Mission accomplished, Jerome. And all it took was 175bps of rate hikes and the unwinding of snarled global supply chains. Now, we get to look forward to the fallout from the lagged effects of the next 350bps of hikes.