Everybody Step to the Right

Back on the East Coast and ready to rumble...

Summary:

Market Dynamics and Retirement Fund Trends: The beginning of 2024 has shown significant shifts in market trends, with a notable rotation between value and growth stocks.

Economic Indicators and Equity Flows: The weak December jobs report and low ISM hiring intentions, which are below the onset levels of the past four recessions, raise concerns about the future of equity flows. Coupled with a trend of steady liquidation in 401Ks since COVID, primarily due to increased retirements and the aging of the Baby Boomers, this should lead to downward pressure on equities.

Outlook for the R2000 Index: The R2000 index is facing unique challenges as it is over-owned by active managers who are struggling, leading to underperformance. The lack of significant share buybacks in the R2000 compared to larger indexes like the S&P 500, coupled with concerns about profitability, paints a less hopeful outlook for this index in 2024.

What I’ve Been Reading Writing

Alongside Simplify’s CIO, David Berns, I’ve been working on my first book. It’s a straightforward primer on harvesting option premium for Wiley in their “Little Book” series. We sent the preliminary manuscript off to the publisher this past week and I am looking forward to seeing it published sometime in March. My mother is very excited. I am very exhausted.

Top Comment

Levi brings a hard-wearing, utilitarian observation:

I wonder how many white-collar laid-off workers (especially from big tech) from the past year or so decided they'd rather ride severance + HELOC + credit cards (which you can use to pay mortgage/HELOC) until taking a distribution from a 401(k) or selling their stock in January (to maximize the time before having to pay taxes/penalties)?

Last week felt like everyone was itching to delay taking profits until 2024.

MWG: Levi, you nailed it. Certainly looks like the delayed profit-taking played out as hypothesized.

The Main Event

A week into 2024, we’ve seen signs that the end-of-year tax deadline was indeed important. The absurd rotation between value and growth in the last three months is illustrative, with the past four trading days unwinding over half of the Value underperformance in Q4 2023:

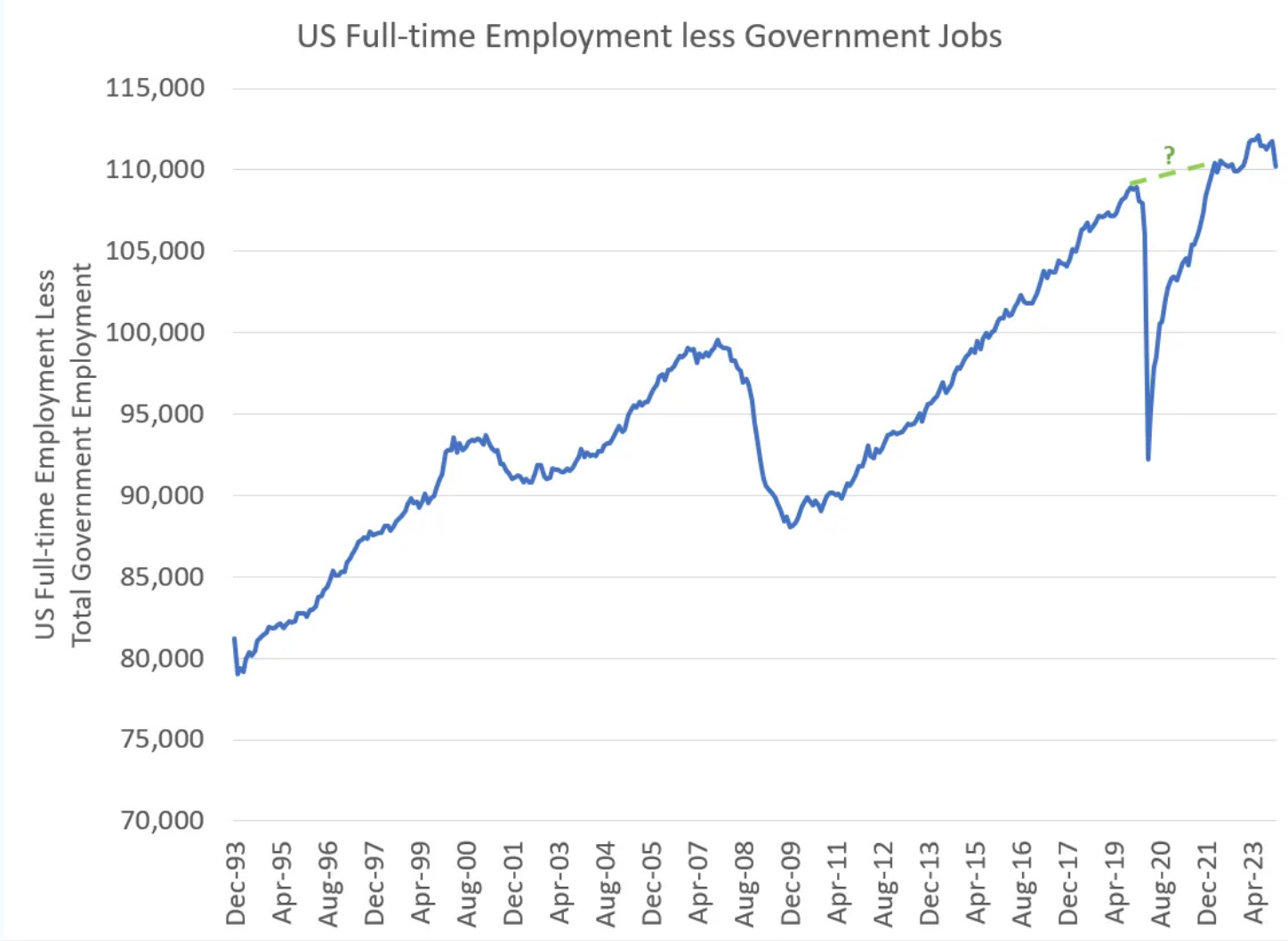

We got the December jobs report, and let’s just say it was ugly. While many have presented variations on the theme of “all the hiring is government and social services,” I remain convinced that we are finally due for the Covid-interrupted expansion to end:

The start of the year has been particularly interesting for the R2000 as the rally from last October’s lows has reversed sharply back into the 2022-23 consolidation. While hope springs eternal, I am less hopeful than most (explanation below).

The key question in 2024, particularly in light of the weak jobs report and even weaker ISM hiring intentions, a level below the onset of the past four recessions, is what happens to equity flows.

As Steve Blitz at T.S. Lombard points out, 401Ks have been in steady liquidation since COVID, a combination of increased retirements and the natural aging of the Baby Boomers. All else equal, we would expect this to place downward pressure on equities, although obviously, there are other sources of flows. IRAs, for example, remain net buyers at this point. The different multipliers of active vs passive are another driver of equity performance that has kept this from mattering as much as we might think.

Surprisingly, we’re even beginning to see this hit Vanguard, which is now net selling shares of stocks from their mutual funds: