Drowning in the Rubicon

Receding liquidity will likely dominate political events in Europe

Summary

The debt ceiling resolution should lead to a surge in Treasury issuance and a reduction in risk appetite. However, the markets seemed to rally after the resolution, possibly due to a brief news-driven relief rally and large retail inflows into equities that have begun to reverse.

Following the start of debt issuance, a downtrend was observed in the market, especially in small-cap indices and credit markets. This supports the hypothesis that liquidity outflows may cause instability in the market, potentially making things "very messy."

Increased interest rates will lead more companies to hit tax deductibility limit thresholds as they refinance, leading to a faster rise in effective interest expenses than interest rates themselves. This will likely cause a collapse in profitability and free cash flow in levered companies, posing a substantial market risk.

Top Comment

John Taylor had an excellent comment that, unfortunately, is too long to repost in its entirety. I encourage you to read it on last week’s note. However, the crux of his bias towards “deflation” is the following:

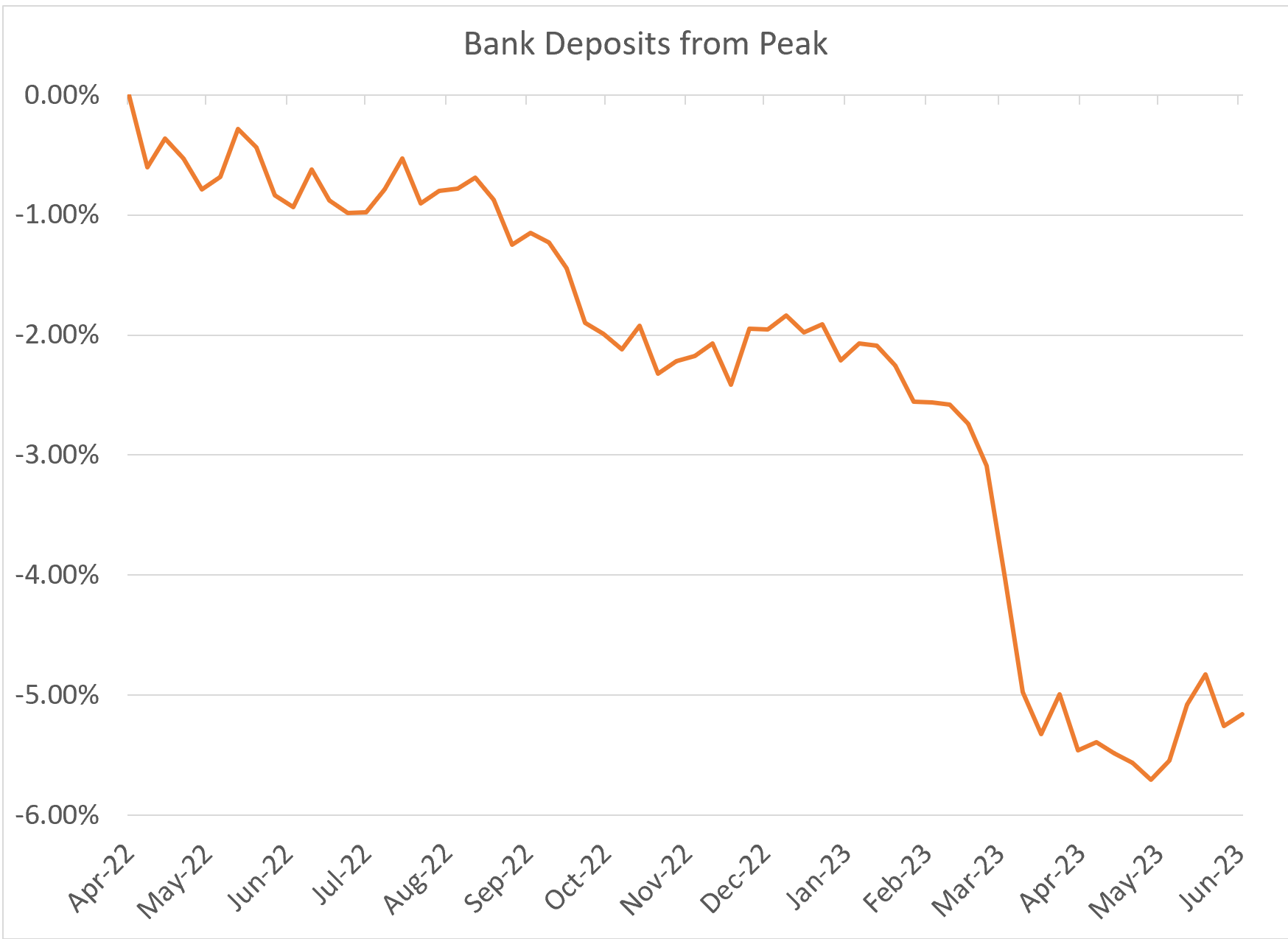

My main reason for being on the deflationist side, though, is the US banking system. They’re still sitting on a lot of bonds and loans that yield less than their current cost of capital while commercial loans and CRE bonds mature and are unable or unwilling to refinance at current rates, especially if their collateral has fallen in value. I still believe we see another series of bank failures around September, and this will continue until something fails with enough counterparty risk to spook the Fed and roil markets, then either Powell or his replacement will cut rates back towards zero (which is more about the political appearance of help than actual help).

MWG: I agree with this observation and would highlight that after a brief consolidation, it appears that bank deposits are again turning lower based on the Fed’s reported reserve levels. We won’t know until the actual deposit data is released next week, but it appears likely we’ll make a new low:

The bank equities have again begun to falter and are now materially closer to a retest of the lows than the “new bull market” narrative.

So let’s hear it for John (and Zachary) Taylor. Thank you for your thoughts! (and war service in the Mexican-American War… without you, we might not have had California to leave.)

The Main Event

With news of a revolt by the Wagner Group in Russia dominating the headlines this weekend… or perhaps it’s a failed purge by Putin now turned into a revolt… or… as Pippa Malmgren posits, a failed purge turned into a revolt turned into a coup (this seems highly plausible to me although it is likely to take most of the year to play out), it was easy to forget the drama of the debt ceiling just a few weeks ago. Ultimately, I think history will blend the two stories into a significant risk-off event.