BIGfoot is real

I hate it when a plan comes together...

For about a decade, I have been making the same argument.

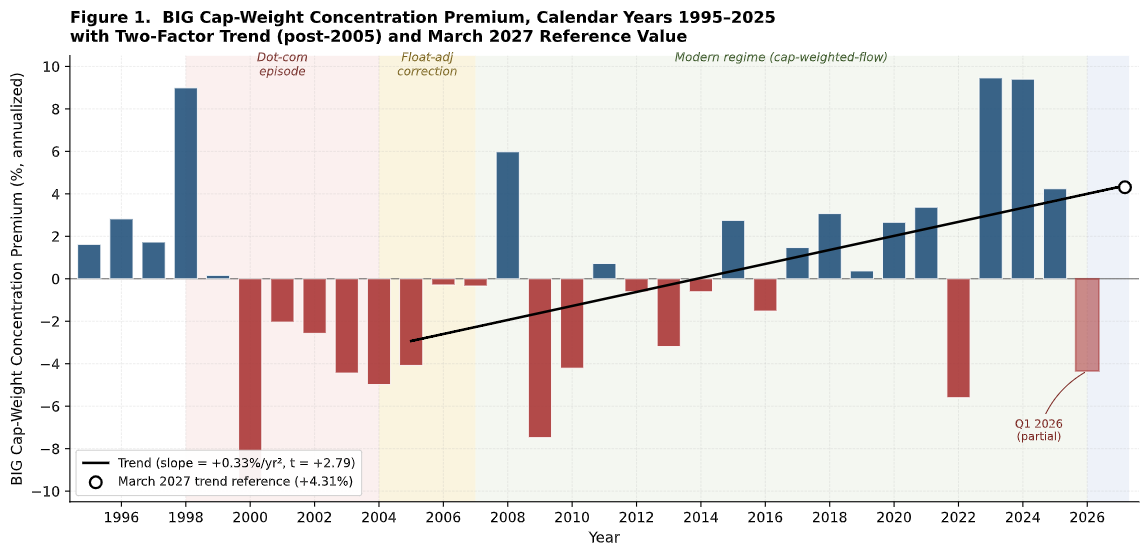

Cap-weighted passive investing, when it gets large enough relative to the active capital on the other side, should leave a measurable trace in returns. Not because index funds are bad, or because low fees are wrong (although I think we’ve lost perspective when discussing a fee cut from 3 to 2 bps as “largest ever”), or even because people buying them are making a mistake. The argument is the societal risk created by a growing mechanical bid. Every dollar that enters a cap-weighted index fund is distributed by existing market capitalization. Bigger companies get more of every dollar. If the dollar volume gets large enough and the active investors who would normally arbitrage that flow become small enough, the rule itself starts to move prices.

The fair objection has always been, “Show me.”

I’m about to release a white paper that I believe does this.

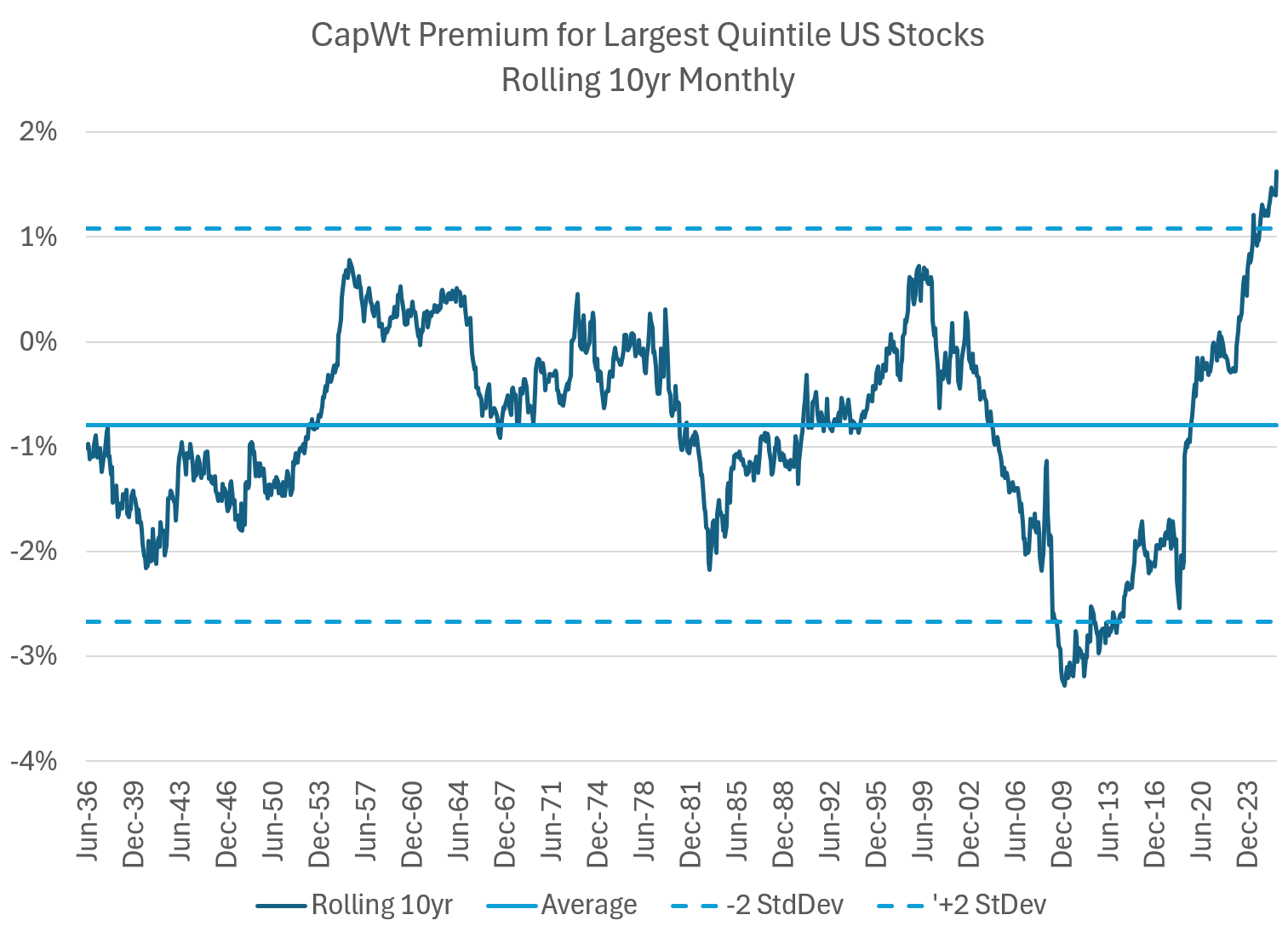

The trend above is the heart of it. Let me walk you through what you are looking at, because the argument is more measurement than opinion.

The simple question

We are all well aware that large stocks have outperformed small stocks for the last few decades. But inside groups of similarly sized companies, are the largest companies increasingly outperforming the smaller ones?