A MonSTeR of a Rally

You have to admire the chutzpah

Summary:

Labor Market Dynamics: Government jobs have experienced a post-pandemic surge in hiring, with relatively low quit rates due to high wages and benefits, especially at lower education levels. This slow-moving phenomenon now appears to be turning lower which, alongside a renewal of the private sector downturn suggests the economy is at a precipice.

Interest Rate Trends: Recent rises in global interest rates appear to reflect broader Western economic policy and trade imbalances with China rather than purely U.S. fiscal deficits. China’s substantial trade surplus may be influencing Western rates indirectly as it seeks ways to manage surplus dollars amid its limited ability to hold treasuries.

Market Structure Shifts: Stock comovement has been increasing due to passive investing, with the advent of short-dated options interrupting a trend in implied correlation.

Cryptocurrency Price Influences: Bitcoin’s price has shown a strong correlation with ETF inflows, suggesting that its price is now highly sensitive to passive investment flows.

Top Comment

John Taylor, presumably of Stanford and the Taylor Rule fame, comments:

Great article.

I’ve long argued that the Smoot-Hawley tariff was not a primary cause of the Great Depression so much as a reaction to falling global demand, more in line with Kindleberger’s writings. It’s tough though because we are in a time where tariffs and unions have been overly blamed for our economic ills over the last 40 years.

As for the size and impact of passive side at the end, I understand how incredibly complex it is to calculate. There are many gray areas from “closet indexers” to momentum investors to active managers who allocate between various market sector ETF’s rather than individual stocks.

Your chart at the end showing median price to sales vs market cap weighted price to sales does an excellent job or illustrating the problem though.

If I was ever able to suggest a fix for the problems caused by passive investing, I would probably just focus on reinstating limits to the exposure to individual securities that are allowed in 401k’s and pensions. Each product offered to these investment products would have to calculate the percentage of money allocated to each individual company enough to show that it was capped at 1% or less of the portfolio.

Obviously, this would have huge ramifications today and would have to be eased in, and it would foster a secondary goal of reversing the trends towards monopolization.

MWG response:

Thanks, John. I think the detailed proposal is useful, but remember that “risk finds a way…” to paraphrase Jeff Goldblum. Very detailed prescriptions are easily gamed and this is, unfortunately, part of the spirit of regulation.

On the Great Depression, I am finding myself quoting Keynes more and more (even as I disagree with many of his thoughts).

"Practical men, who believe themselves to be quite exempt from any intellectual influences, are usually the slaves of some defunct economist"

Friedman and Schwartz’ definitive work on the Great Depression was a notable piece of scholarship, but the core assumption of fixed velocity has proven totally false in a floating exchange rate regime. While I share many of Friedman’s views, I unfortunately think nearly irreparable harm has been done in his name.

The Main Event

This coming week, I’ll be debating Randy Cohen of HBS on the impact of passive investing. It will be challenging not only because my view is distinctly heterodox but because Randy is sight-impaired; “sharing charts,” which is my primary mechanism of communication, will be impossible. This has been quite helpful in forcing me to develop more transparent communication around mechanisms, and I look forward to the debate. I also had an interesting discussion with a reporter who asked me a very important question, “Why do you care so much?” More on that to close.

I had to take a break from analyzing the impact of Trump vs. Harris because I’m bored with it candidly, and far too much exciting stuff is happening in my analysis of the impacts of passive investing. So, those of you here for my (flawed) political/economic analysis will have to wait a week or so for those final thoughts. With that said, there were a number of key economic reports this week that provide a valuable context for what the world may look like in a few months. In particular, Friday’s employment report was a rich vein that, after adjusting for hurricanes and strikes (and of course Birth/Death model distortions), provided further evidence that the slowdown is again upon us after a brief interlude in Q3-2024:

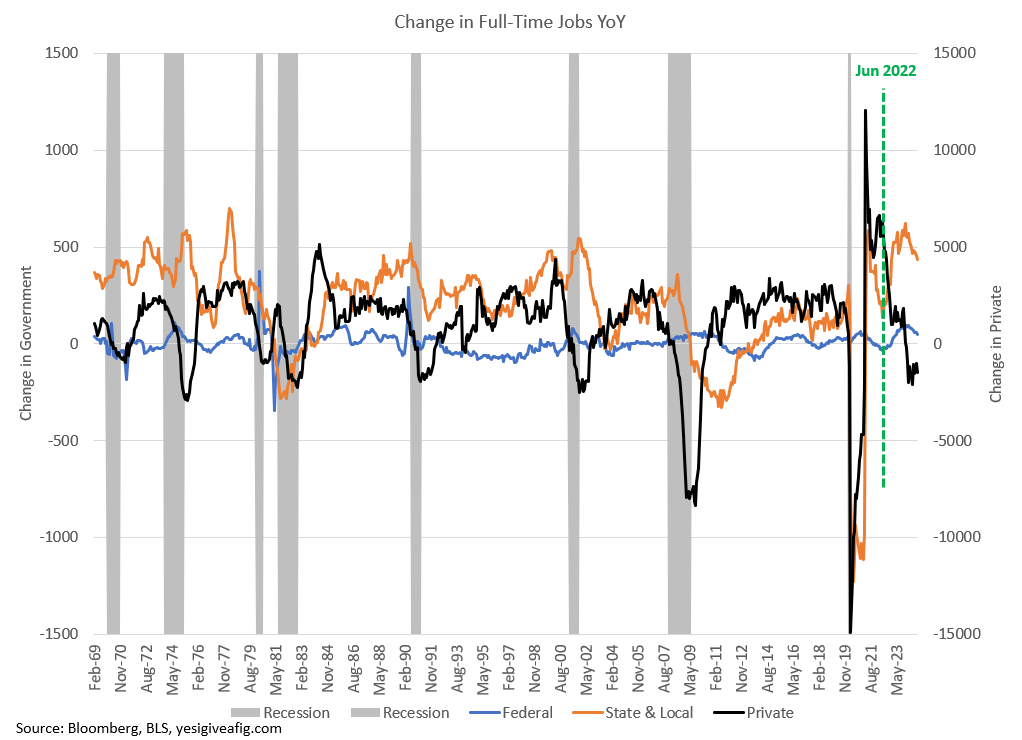

I’ve made a point of highlighting June 2022. This month coincides with the peak oil impact of the Russian invasion of Ukraine, but from a macroeconomic standpoint a more important component was the sudden acceleration in government employment. It appears this was tied to the “great reopening” of schools and healthcare in the post-pandemic period. While it may seem a distant memory, this was the “Great Resignation” period aftermath when back to school/work prompted a magnificent reshuffling of employment conditions. The public sector behaved no differently than the private sector, seeing an almost identical relative shift.

Note that government employees quit at roughly 1/3rd the rate of their private counterparts (separate axes are scaled identically). The reason for this is straightforward — relative wages and benefits at the low end are far more attractive for government employees than the private sector. If you only have a high school diploma, you make nearly 50% more than your private sector counterparts. Quitting would be absurd. Conversely, for those with professional degrees (think lawyers), the door is quite a bit more attractive to switch to lobbying when the opportunity presents itself. As I discussed a few weeks ago — POSIWID — the proof of a system is what it does.

It’s worth highlighting the assumption in the analysis… so I did. For readers unaware of the reference, benefits in the private sector are far higher at large firms than small firms, so these results are likely much more skewed than shown when we consider the true economy where less educated workers are often employed at small employers (e.g. retail, local construction, etc) with few benefits.

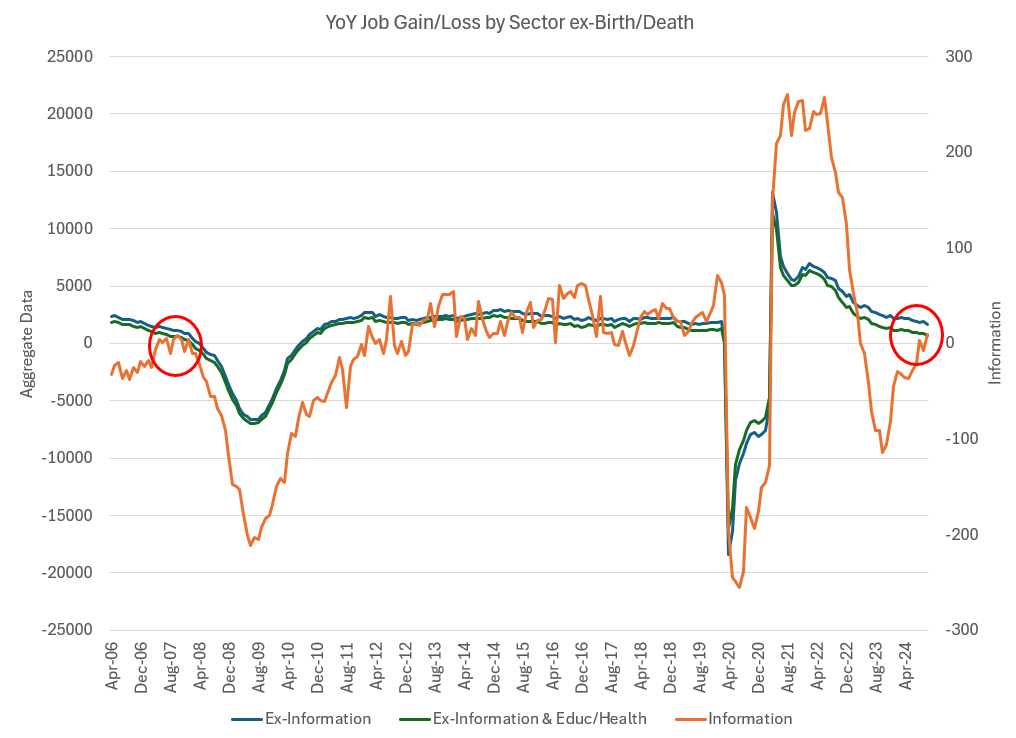

This much lower quit rate means fewer resources are devoted to recruiting and managing a dynamic labor force. As a result, the wheels were much slower to start turning in the public sector than in the private sector, and hiring showed up later. The critical question is, can the private sector, largely IN recession for the past two years, begin to recover as the public sector falters? As I noted on Twitter, when a pebble (information sector) meets a boulder (everything else), the boulder is not crushed. If we’re going to turn, we better turn quickly:

On the recent surge in interest rates, I offer a contrarian take. High hopes for a Red sweep on increased government spending are claimed to be behind the recent rise in interest rates. This appears to be a DECLINING probability as the prospect for an electoral college sweep are FALLING since Oct 25th, not rising. Odds of a marginal Democrat victory are rising slightly over the past few days (red line):

I will add three observations:

Rates are rising globally in Western countries in a highly correlated manner (note I have multiplied Japan’s rates by 5x to put on same scale), while gold (inverted) and Chinese rates are moving in lockstep in the opposite direction. Unfortunately, this suggests that the real story is Western unwillingness to cut-off China’s unprecedented trade surplus (helpful for mollifying constituents and reducing inflation) while having proven their willingness to “freeze” the assets of major sovereign entities who invade small neighboring countries. If China can’t hold treasuries, it can use the dollars earned in trade surplus to sell dollars and “buy” Chinese rates/gold/etc. Since China is simultaneously trying to maintain a rough peg to the dollar, this must manifest in rates rather than currency as they must find the marginal buyer willing to hold Western debt (not just US debt). If the trade surplus is greater than reported (as Brad Setser seems to have documented), then this becomes an even more compelling explanation for the behavior we’re seeing in rates.

Extension of the Trump tax cuts is not new spending, even as it raises the deficit and issuance versus baseline projections. As a result, I genuinely don’t understand how people view this as “stimulus.” A reprieve, maybe.

New tariffs on trade, almost inevitable and necessary under either administration, are new taxes that do not require Congress. In contrast, subsidies for domestic production WILL require a unified Congress and presidency. Prepare for disappointment in the real economy even as investors gear up to buy “Stonks!” And if I’m right that the story is actually about China's trade surplus rather than US fiscal deficits, a Trump victory could indeed set off a monster rally in rates while US equities play second fiddle.

With that, let’s switch to passive. Don’t just sit there; let’s actively dig in…