A Look Forward

A recent tweet provides room for exploration

Summary

Section 1: Challenges for Active Managers

Despite recognized skill in active management, active managers struggle even as calls for “next year” continue

Passive investing's mechanical growth inflates valuations, particularly through momentum effects, and this systematically disadvantages active managers, whose value-oriented strategies underperform in such environments.

Section 2: Relative Valuation and TIPS

Treasury Inflation-Protected Securities (TIPS) provide a real return guaranteed by inflation adjustments, offering a compelling alternative to equities. Real TIPS yields have risen to multi-decade highs, while equity valuations remain stretched, suggesting equities may deliver low or negative real returns over the next decade.

Even under optimistic assumptions of record corporate profitability and stable valuation multiples, projected equity returns are modest. Conversely, TIPS provide a stable, predictable return, emphasizing their relative attractiveness in an environment of high valuations and uncertain inflation trends.

Section 3: Broader Market Dynamics

U.S. equity markets remain overvalued relative to historical benchmarks, even when adjusted for current profitability trends. The decline in cash allocations and bullish sentiment in active management reflect a continuation of passive-dominated flows, reinforcing the structural underperformance of active strategies until flows reverse.

Top Comment

TC is back with another great question:

Is Powell "finally" asking the right question or is he just doing it because its convenient to do so? It was expectable that they'd get back to the trend of understating their inflation metric below reality to allow financial repression. 2022-23 was an anomaly, conveniently timed in the middle of a presidential term, when they got the chance to build a rate cushion / dry powder to resume rate cuts.

On the opposite side of that dynamic, are higher rates even restrictive? For net lenders, top decile/quintile consumers, I can't imagine they are. And they are the ones doing most of the spending. But are they restrictive on the whole?

MWG Response: While no one is watching, the evidence that rates are restrictive is multiplying. Danielle DiMartino Booth highlighted the growing distressed exchanges and defaults in the variable rate loan market and shrinking household surplus:

And “The Fed Whisperer”, Nick Timiraos, offered support for my conclusion. It’s notable that post-Powell he chose to highlight growth in continuing claims:

I believe Powell’s concerns are genuine.

The Main Event

As the last days of 2024 slip by in a haze of Beef Wellington, glazed ham, and roasted turkey (and an uncheduled swim team brunch at our house this morning — blueberry pancakes, bacon, scrambled eggs, bagels & cream cheese, and hashbrowns for ~20 coming up in a few hours), it’s worth remembering we end 2024 as we started it — with forecasts for next year being the one for active managers:

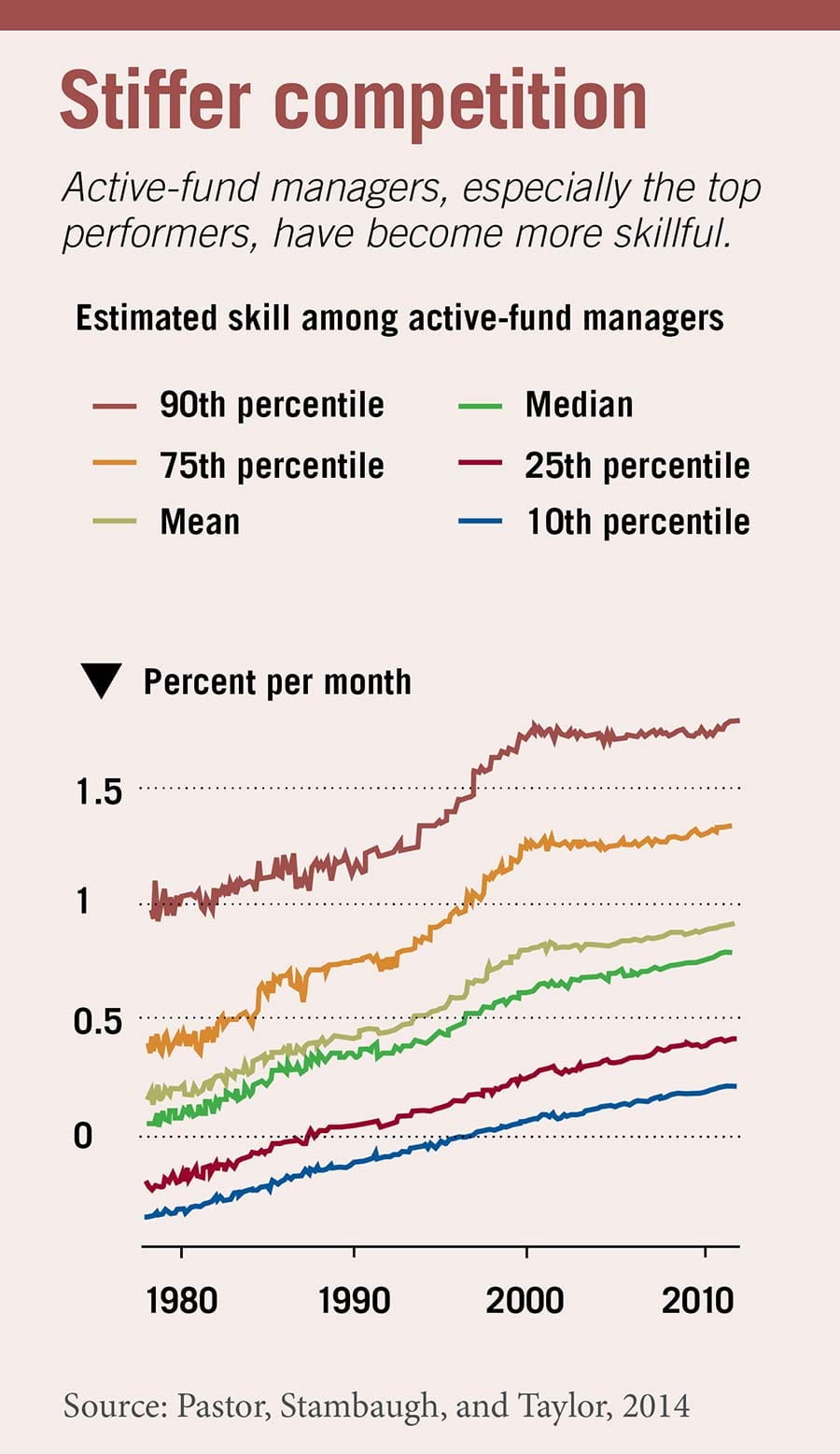

The problem with these forecasts is that they presume the question is one of skill… we already KNOW that active managers have skill. In 2004, Berk & Green published a paper identifying skill in active management. In 2014, their work was supported and extended by Pastor et al in a nicely summarized piece at UChicago research (a second rate, school, but prolific publishers nonetheless):

The text of the article lays out a thesis that is seductive:

Stockpickers have skill

Among those challenging the conventional wisdom that beating the market is more about luck than skill are Jonathan Berk and Richard C. Green.

In 2004, Berk (then at Berkeley, and now at Stanford) and Carnegie Mellon’s Green published a pioneering paper suggesting that an individual manager can have skill—and can beat the market by an average of 6.5 percentage points.

This same research also suggests that it’s hard to maintain market-beating performance. Although a manager can be skilled, the job is made harder as investors recognize and reward that skill. Half a dozen empirical papers have since tested and supported this hypothesis. The challenge is that as investors recognize a manager’s skill, they place more assets under his management. Those additional assets make it harder for the manager to achieve the same level of performance—among other reasons, because the bigger a fund is, the more likely it is to move prices. If a manager invests $100,000 in a company, it may go largely unnoticed. If he invests $1 million, he may raise the stock price in the process. The upshot is that while some money managers can beat the market, they can ultimately become victims of their own success.

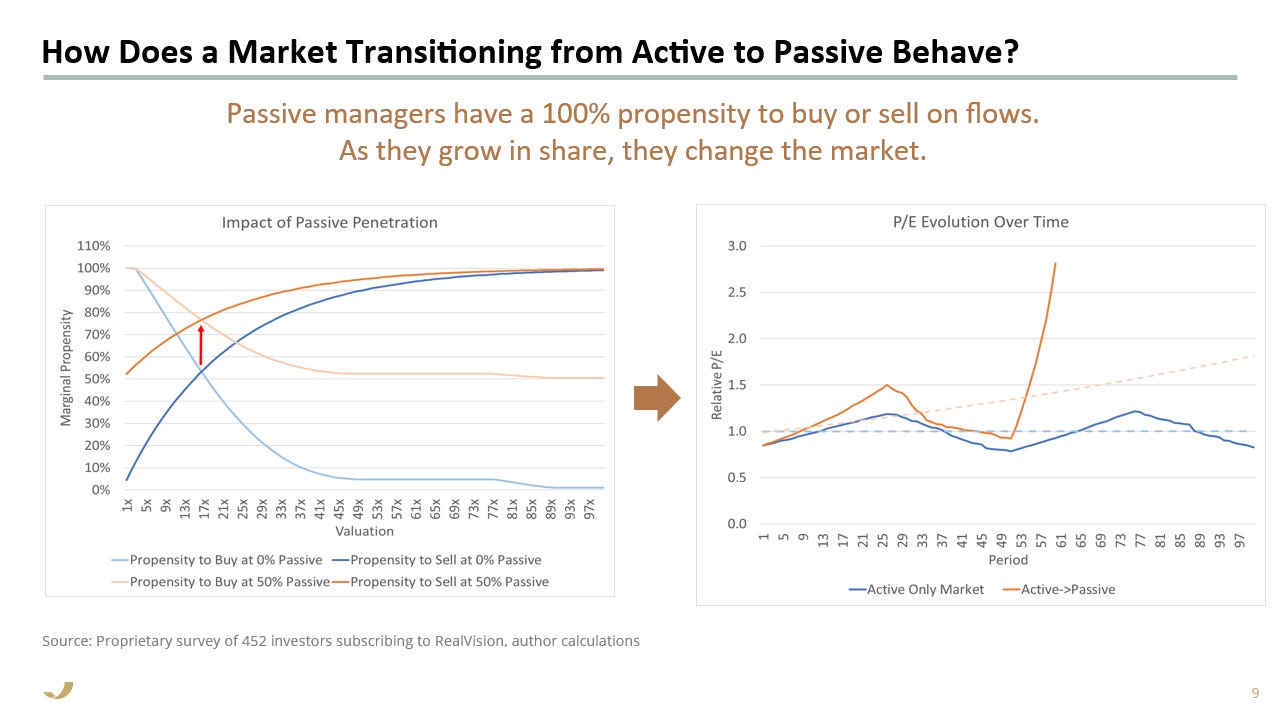

Now YIGAF readers will note the irony… more assets, more price impact. Except of course for passive index funds… they supposedly have no effect…

Not only did the paper hypothesize that size was the problem, it offered evidence that active managers were becoming more skilled:

So the outflows from Active management should make this a nirvana era… nimble, increasingly skilled active managers with fewer assets should be having a field day. I used to believe this as well. But they are not having a field day, and at some point, when empirical data so noticeably diverges from theoretical predictions, you have to ask, “Why?”

The answer, as you already know, is that “passive is not passive” and just like active managers influence price as they grow, so do “systematic algorithmic investors with the world’s simplest algorithm.” (If you give me cash, then buy; if you ask for cash, then sell). This MECHANICALLY leads to rising valuations — and the impact grows as passive gains share: